The semiconductor business goes via the worst section in additional than a decade, harm by the unfavorable pricing surroundings, regardless of steady demand. For reminiscence chip maker Micron Expertise Inc. (NASDAQ: MU), the primary half of 2023 was a very difficult interval when revenues declined throughout the board and the underside line slipped into unfavorable territory. Worryingly, the downturn is anticipated to persist within the second half.

Micron’s inventory has been in free fall for greater than a 12 months now, leading to a major discount within the firm’s market worth. Prior to now twelve months, it went via a collection of ups and downs, reflecting the blended investor sentiment. On the constructive aspect, the inventory has turn out to be extra reasonably priced, and plenty of potential buyers would discover it enticing. Additionally, Micron’s dominance within the reminiscence chip market and profitable enterprise mannequin would allow it to create long-term shareholder worth.

Growth

The tech agency is at the moment constructing what it calls the Megafab in New York, spending about $100 billion. Touted as the most important semiconductor fabrication facility within the US, the manufacturing facility is anticipated to present the corporate a major edge over rivals. It’s anticipated that the whole addressable marketplace for reminiscence and storage chips would develop to a document excessive within the subsequent two years, outpacing the bigger semiconductor business.

“Our expectations for calendar 2023 business bit demand progress have moderated to roughly 5% in DRAM and low-teens presentation vary in NAND, that are properly under the anticipated long-term CAGAR of mid-teens proportion vary in DRAM and low 20s proportion vary in NAND. The discount in calendar 2023 demand from our prior forecast is pushed by an evaluation of buyer inventories in addition to some degradation in finish market demand. We count on that bettering buyer inventories will help sequential bit demand progress for DRAM and NAND via the calendar 12 months,” stated Micron’s CEO Sanjay Mehrotra in a latest assertion.

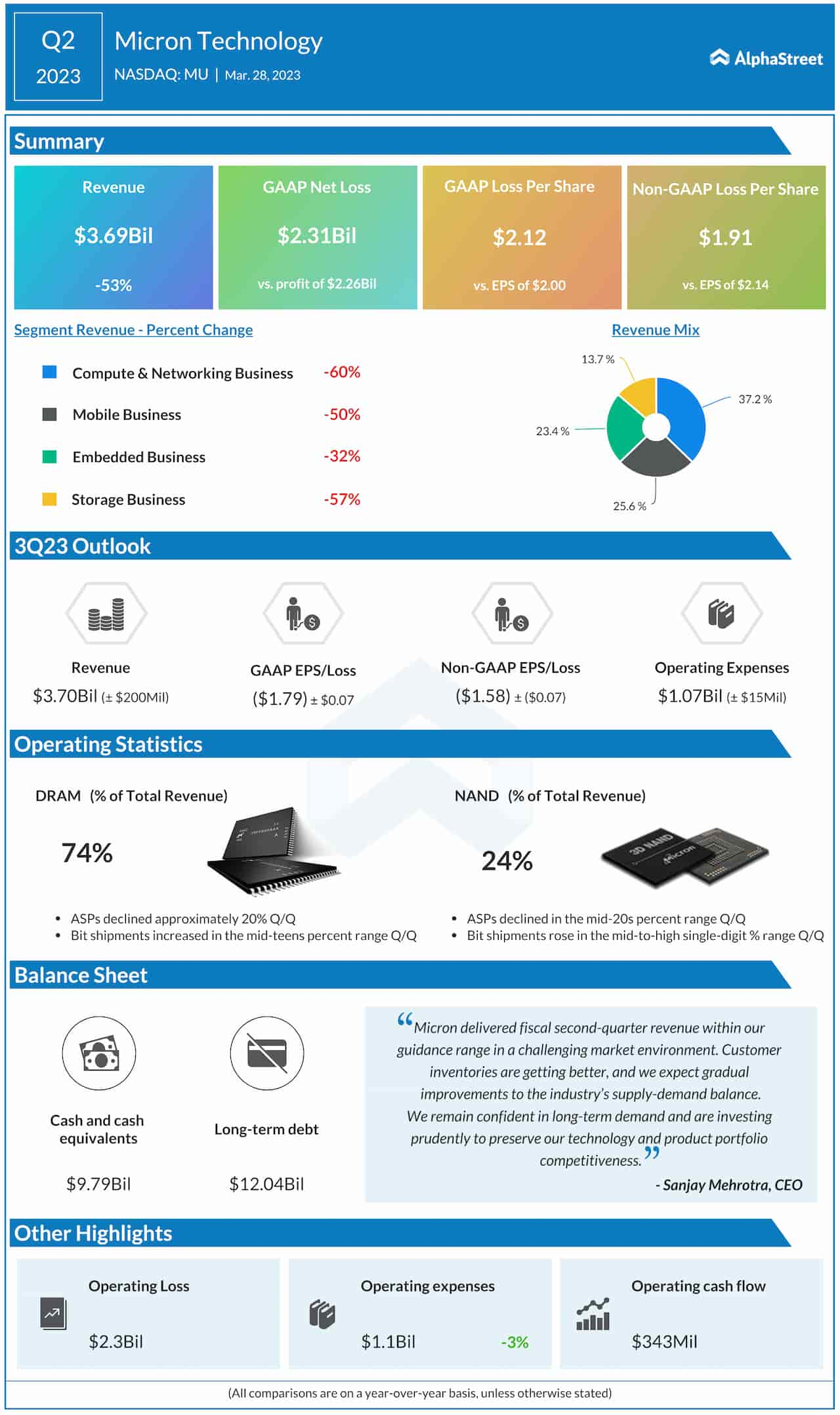

Weak Q2

In a dismal present, all 4 working segments contracted in double digits within the second quarter of 2023 when whole revenues dropped 53% year-over-year to $3.69 billion. That was consistent with the administration’s steering. Consequently, the corporate slipped right into a loss, marking the second consecutive unfavorable earnings. The underside line additionally missed estimates, because it did within the prior quarter, reversing the long-term pattern of normal beats. On an adjusted foundation, the web loss was $1.91 per share, in comparison with earnings of $2.14 per share within the prior-year quarter.

In the meantime, Micron executives are of the view that buyer inventories and the business’s supply-demand steadiness would enhance within the coming months. On Tuesday, Micron’s shares declined in early buying and selling and hovered barely under the long-term common. They’re up 16% for the reason that starting of the 12 months.

{kind=link}