alvarez

JFrog (NASDAQ: FROG) is a US-Israeli supplier of a software program provide chain improvement platform that permits organizations to handle end-to-end lifecycle of software program improvement, from improvement, to launch, and to safety.

I’ve lined FROG before last year in June, once I wrote about its enticing potential, regardless of score the inventory impartial at the moment. I felt that the upside was totally priced in and that buyers ought to watch for a greater entry level then. For the months following my maintain score, FROG remained comparatively flat, reinforcing a few of my preliminary considerations. Nonetheless, these considerations dissipated faster than I had anticipated, as FROG noticed a surge beginning in November and is now up by about 41% since my final score. The excellent news is that given the present atmosphere, I imagine buyers can nonetheless seize some extra upside in FROG.

I’ve upgraded FROG to purchase. My modeled 1-year goal value of $43 initiatives a 16% upside. FROG stays a beneficiary of the secular digital enterprise transformation development. The current non permanent headwinds within the type of delayed enterprise cloud migration initiatives could probably subside within the second half. The current pullback to $37 offers a stable purchase alternative, in my view.

Monetary Evaluation

YCharts

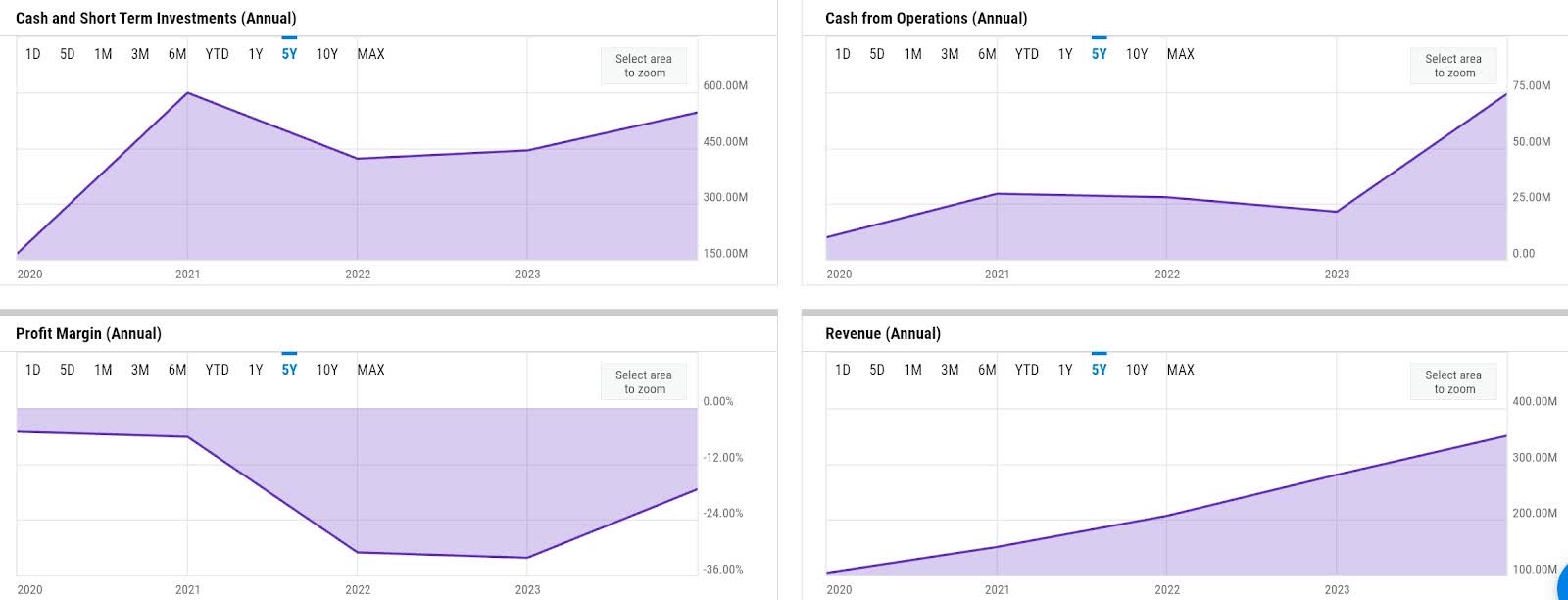

Apart from the weak GAAP profitability, FROG has respectable fundamentals, which I additionally famous in my earlier protection. Income development has normalized from over 60% to 25% over the previous 5 years. In FY 2023, FROG delivered a income of $350 million, a 25% YoY development. Internet loss margin has narrowed somewhat bit to -17%, although it’s nonetheless distant from break even. One constructive factor in FY 2023, in my view, is the numerous working money move (OCF) enlargement to $74 million, greater than triple that of final yr. This has resulted in a good liquidity enhance for the yr. FROG ended FY 2023 with over $545 million of money and short-term investments.

Catalyst

As per my earlier protection, I imagine FROG will general proceed to profit from the secular enterprise digital transformation traits. On this protection, it’s most likely worthwhile to know how FROG truly has been benefiting from the development and the way it’s progressing to this point.

In This fall, it seems that FROG’s major go-to market entry level within the enterprise digital transformation phase could have been cloud migration. Cloud migration is the method of transferring on-premise enterprise information and purposes to the cloud, making it a crucial half to modernizing an enterprise IT atmosphere.

The motivation is kind of clear – cloud-hosted purposes supply higher economics long run by way of simpler upkeep and higher scalabilities. Nonetheless, this additionally means migrating an usually sizable software codebase to the cloud and securing it. Since FROG’s choices assist enterprises obtain this by streamlining the software program improvement provide chain from code-development to launch, investing in FROG looks like a smart choice to attain such a marginal profit in a capital-intensive digital transformation undertaking.

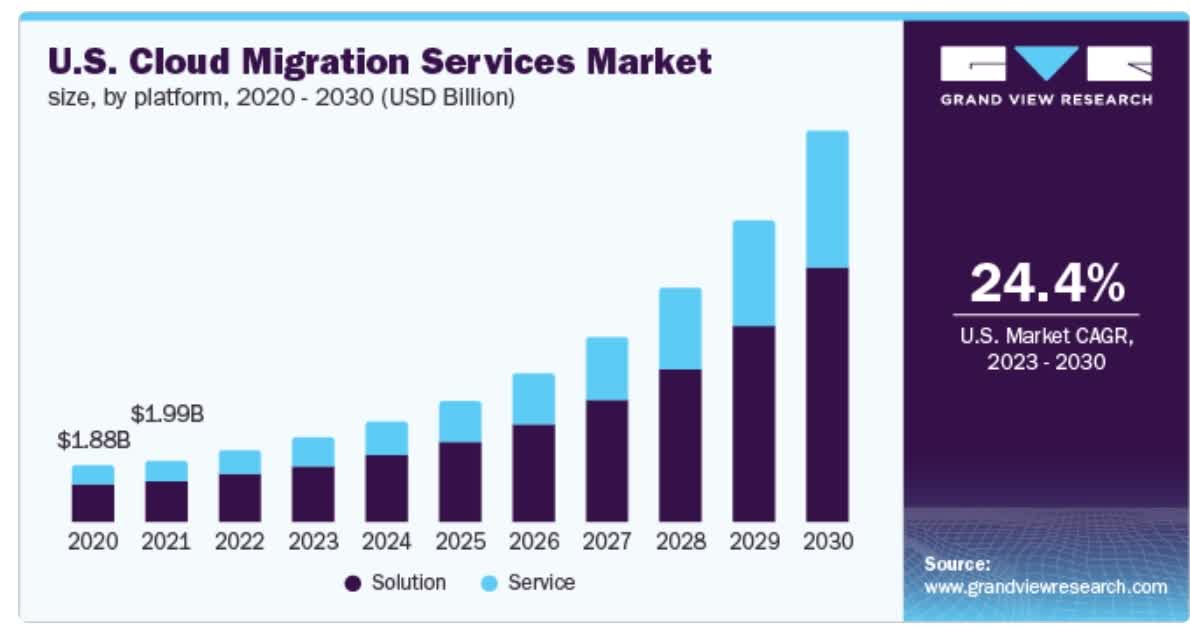

Grand View Analysis

Rising at 24.4% CAGR, cloud migration is projected to be an $18 billion market by itself in 2024 within the US alone. Although this isn’t a direct market alternative for FROG, its choices have been in demand as a result of enhance in enterprise cloud migration actions, as commented by the administration in This fall earnings name:

Third, I wish to deal with development within the enterprise adoption of the JFrog platform. The transfer towards a unified common platform for the enterprise is just not solely a expertise or device initiative but in addition a change we see in how corporations are being structured to streamline digital deliveries. We see roles like CIOs and CISOs changing into one and cloud migration initiatives focusing on a number of features like tooling consolidations to attain velocity and belief all through the software program move.

Supply: Q4 earnings call.

At this level, I imagine that there are two key takeaways that might spotlight near-term catalysts for FROG. To start with, the macro problem that has delayed a number of enterprise cloud migration initiatives FROG has been concerned in could probably subside, offering bookings acceleration within the second half of FY, as commented by the administration in This fall:

Slowly into the yr, we noticed an enchancment within the frequency of on-prem to cloud migration initiatives being restarted alongside extending consumption within the second half of the yr as we shared in earlier calls.

Supply: This fall earnings name.

Second of all, I imagine the restart of those delayed cloud migration initiatives will proceed to emphasise the significance of IT price optimization, which is achieved primarily by way of vendor consolidation. FROG is well-positioned to reap the profit right here, due to the character of its options that deal with the entire software program improvement provide chain.

Threat

For my part, FROG’s market share seize within the enterprise phase, which has been fairly vital as of late, could probably elevate income focus threat. Virtually half of FROG’s income in FY 2023 got here from enterprise subscriptions, in comparison with simply 38% final yr. As per its 10K, this has resulted within the high 10 prospects making up as a lot as 7% of FROG’s income as of FY 2023. Given the potential acceleration of main enterprise cloud transformation initiatives within the second half, I imagine this determine might probably enhance additional by the top of FY 2024.

Valuation / Pricing

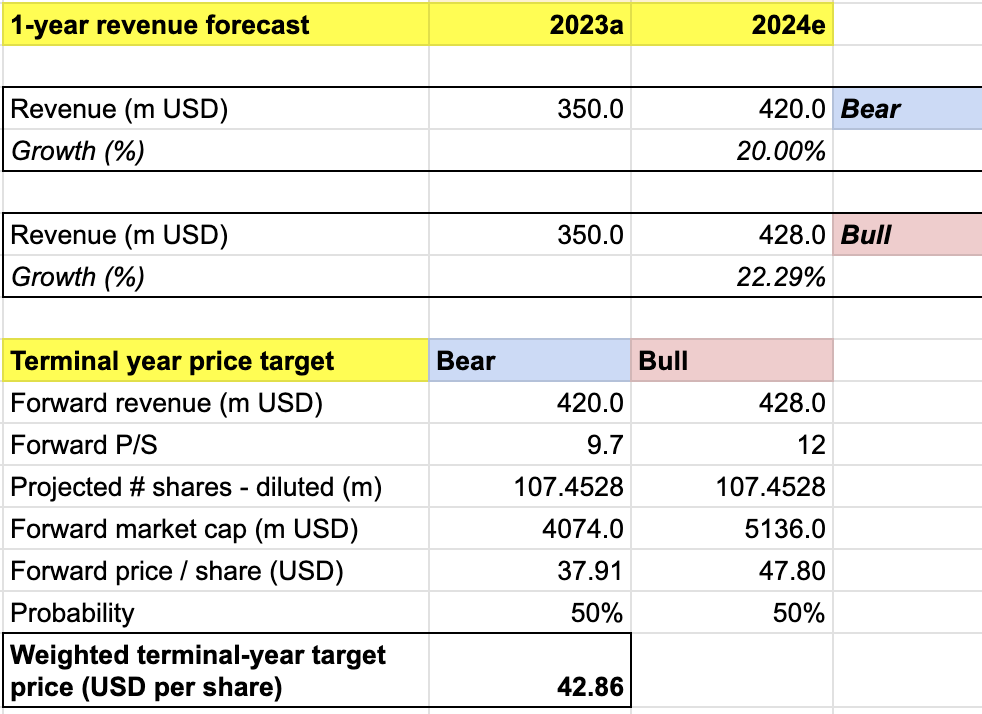

To estimate the goal value for FROG in FY 2024, I assume the next bull vs bear state of affairs in a 5-year income projection:

Bull state of affairs (50%) – FROG to complete FY 2024 with a income of $428 million, a 22% YoY development, in keeping with the corporate’s steerage. On this state of affairs, I count on most cloud migration initiatives to restart within the second half, giving FROG additional income visibility into the FY. P/S to broaden to 12x, the extent the place it just lately noticed a YTD excessive.

Bear state of affairs (50%) – FROG to complete FY 2024 with a income of $420 million, a 20% YoY development, which is $8 million decrease than the corporate’s low-end income steerage. I count on FROG to see continued headwinds and sudden churn. On this state of affairs, the market will attain negatively, leading to sideways value motion for the inventory.

personal evaluation

Consolidating all the knowledge above into my mannequin, I arrived at an FY 2024 weighted goal value of ~$43 per share. This represents virtually 16% upside from the present value of $37. I improve FROG to purchase.

Regardless of my conservative projection, FROG nonetheless delivers a stable upside, in my opinion. Nonetheless, the upside right here additionally assumes FROG rebounding again to the place it was earlier than the pullback, which was proper round $43, my goal value. As such, I imagine FROG could also be oversold at this time.

Conclusion

As I highlighted in my earlier protection, FROG is a compelling alternative. It is going to proceed to profit from the secular enterprise digital transformation development, additional fueled by the shift in direction of vendor consolidation technique to optimize prices. Although FROG has seen a little bit of non permanent headwinds within the type of delayed cloud migration initiatives at its potential purchasers, the administration has seen indicators of potential restart within the second half. The current pullback offers an excellent shopping for alternative. My 1-year value goal of $43 signifies that FROG is eyeing virtually 16% upside at yr’s finish.

{kind=link}