Funtay

In 2022, Tourmaline (OTCPK:TRMLF) generated a file free money circulation of CAD$3.2 billion and paid dividends of CAD$7.90 per share on base and particular dividends. Tourmaline’s whole dividends paid elevated from CAD$469 million in 2021 to CAD$2653 million in 2022. Because of the hiked pure gasoline and oil costs in 2022, Tourmaline’s monetary outcomes have been very sturdy and with the present vitality costs, we can not count on the corporate’s 2023 outcomes to be as sturdy as in 2022. Nonetheless, even with present vitality costs, Tourmaline can stay extremely worthwhile, reward its shareholders, cowl its obligations, and enhance its manufacturing. The corporate expects its working money circulation, free money circulation, and capital expenditures in 2023 to be CAD$3.8 billion, CAD$2.0 billion, and CAD$1.7 billion, respectively. You will need to know that as a consequence of coming into right into a 15-year pure gasoline provide agreement (to ship roughly 140 million cubic toes per day) in July 2021, Tourmaline started delivering gasoline to the US Gulf Coast with full publicity to Japan Korea Marker (JKM) pricing in January 2023. Primarily based on its present manufacturing volumes, current developments and acquisitions, and pure gasoline & oil spot and futures costs, Tourmaline’s expectations are dependable. The inventory is a purchase.

Monetary outcomes

In its fourth quarter and full-year 2022 monetary outcomes, Tourmaline reported 2022 commodity gross sales from manufacturing of CAD$8.1 billion, in contrast with CAD$5.1 billion in 2021, because the pure gasoline and crude oil costs hiked. The corporate’s revenue from operations elevated from CAD$2.6 billion in 2021 to CAD$6.0 billion in 2022, up 131% YoY. Tourmaline’s whole produced quantity elevated from 484 thousand boe/d in 2021 (78% pure gasoline) to 508 thousand boe/d in 2022 (77% pure gasoline). The corporate was in a position to enhance its manufacturing degree by 5% in 2022 because of its company and property acquisitions accomplished within the final two years, which accounts for 25% of the rise in 2022. Within the final two years, Tourmaline had a major acquisition exercise by paying CAD$1.6 billion in money and customary shares, which was anticipated to extend its manufacturing by about 70 thousand boe/d.

“The remaining enhance is attributable to the corporate’s profitable exploration and manufacturing program, together with the expansion in condensate and NGL manufacturing which displays the continued improvement of the Gundy space and the commissioning of Gundy Part 2 in January 2022,” the corporate defined.

Tourmaline paid a particular dividend of $CAD2.00 per share on 1 February 2023 and paid a quarterly money dividend of CAD$0.25 per widespread share in 1Q 2023. In 4Q 2022, Tourmaline paid a quarterly dividend and a particular dividend of CAD$0.25 per share and CAD$2.25 per share, respectively. Additionally, in 1Q 2022, the corporate paid a quarterly dividend and a particular dividend of CAD$0.20 per share and CAD$0.125 per share, respectively. The corporate plans to return 50-90% of its free money circulation to shareholders in 2023.

The market outlook

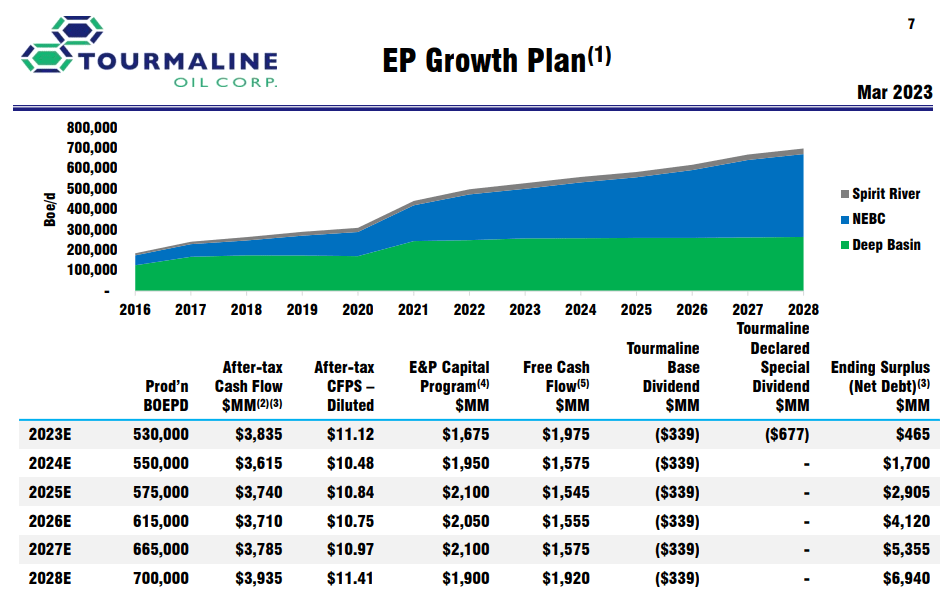

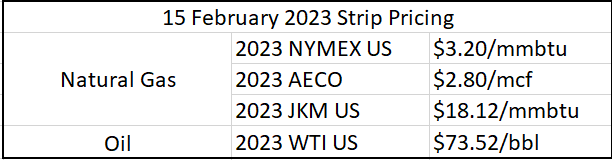

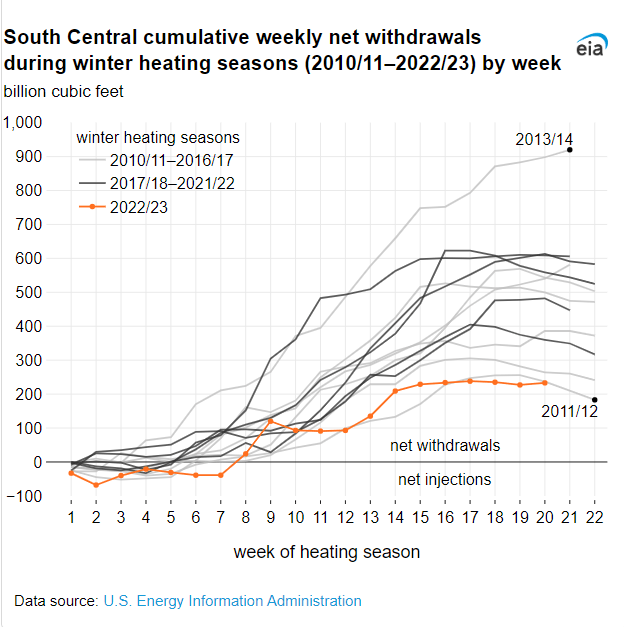

Tourmaline estimates its 1Q 2023 whole manufacturing to be between 520 to 530 thousand boe/d, and expects its full-year 2023 manufacturing to be 520 to 540 thousand boe/d, which is increased than in 2022 and 2021. It’s value noting that Tourmaline expects to drill and full a complete of roughly 300 wells (gross) in 2023. Figure 1 reveals Tourmaline’s exploration and manufacturing (EP) progress plan, which signifies the corporate expects its manufacturing to extend to 700 thousand boe/d in 2028. Primarily based on strip costs on 15 February 2023 and the corporate’s EP progress plan, Tourmaline’s after-tax money circulation and free money circulation in 2023 are anticipated to be CAD$3835 million and CAD$1975 million, respectively. Determine 2 reveals strip costs as of 15 February 2023. Resulting from very gentle temperatures over the last winter, pure gasoline costs in 2023 have been considerably decrease than in 2022, as consumption decreased and pure gasoline manufacturing and storage elevated. In keeping with EIA, cumulative web withdrawals of pure gasoline from the week ending 4 November 2022 to the week ending 17 March 2023 have set a file low (by way of the twentieth Weekly Pure Fuel Storage Report) within the final winter (see Determine 3).

Determine 1 – Tourmaline’s exploration and manufacturing progress plan

March 2023 presentation

Determine 2 – Strip pricing as of 15 February 2023

Writer (primarily based on March 2023 presentation knowledge)

Determine 3 – Cumulative web withdrawals of pure gasoline

eia

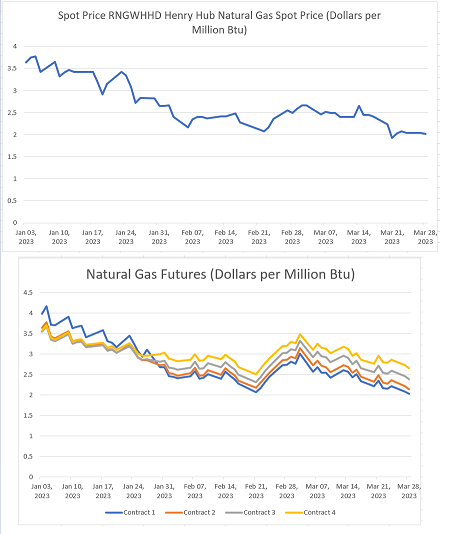

In Determine 4, we are able to see that Henry Hub’s pure gasoline spot worth elevated within the second half of February, then decreased within the second half of March. Henry Hub pure gasoline spot worth is now decrease than on 15 February. Moreover, Determine 3 signifies that pure gasoline futures (NYMEX) elevated within the second half of February, then decreased. As of 28 March 2023, pure gasoline futures (NYMEX) have been decrease than on 15 February 2023. In keeping with EIA’s pure gasoline weekly replace, within the week ending 29 March 2023, the value of the 12-month strip averaging Could 2023 by way of April 2024 futures contracts declined 5 cents to $3.083/MMBtu.

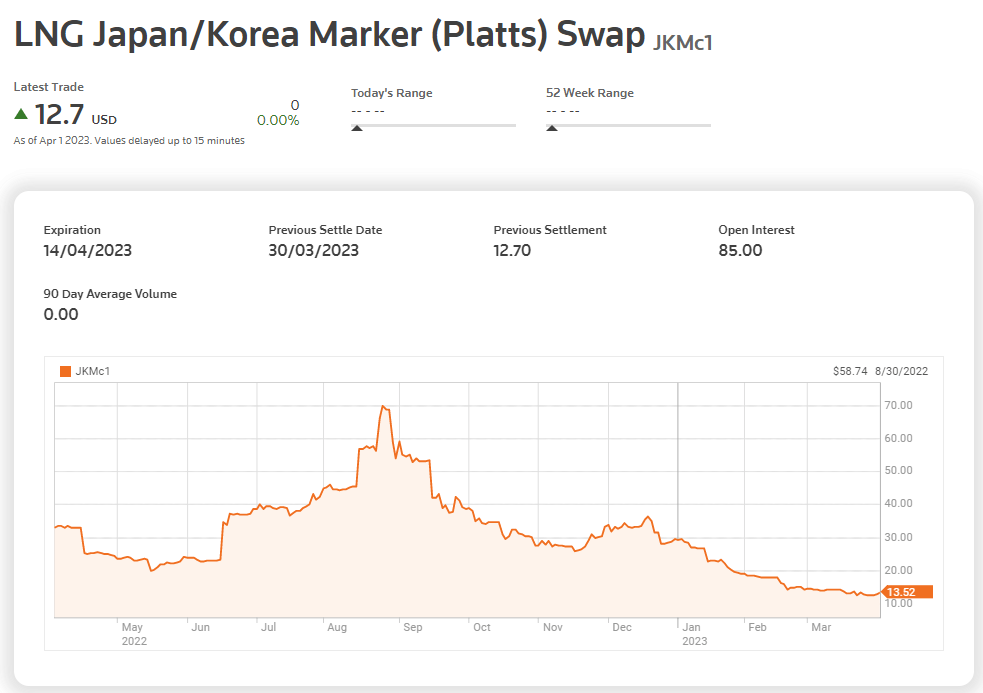

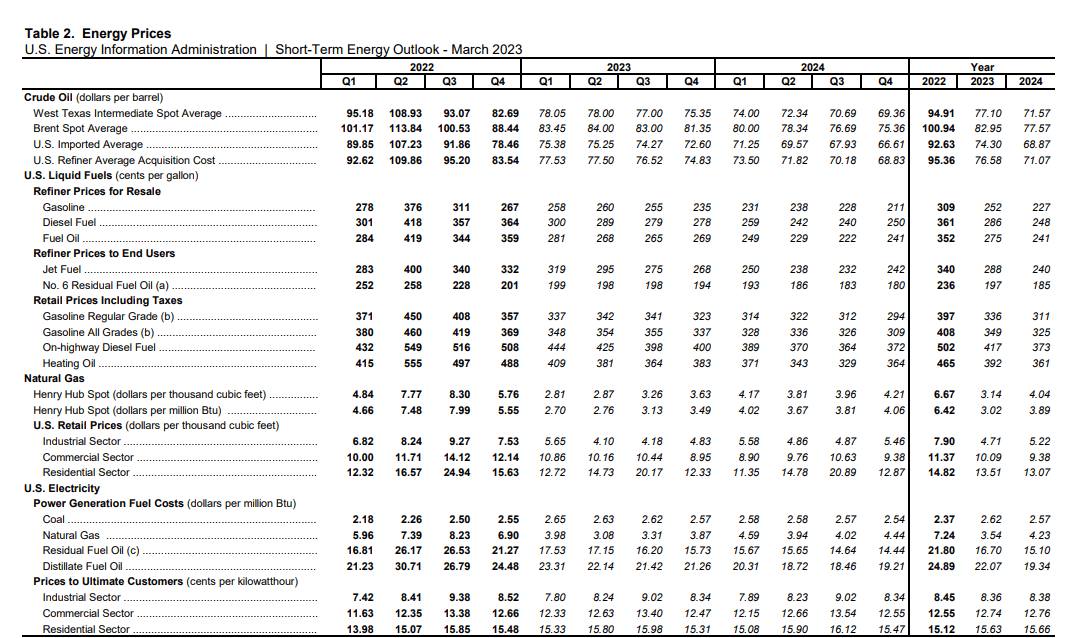

Moreover, Figure 5 reveals that JKM costs decreased up to now month. In keeping with EIA’s short-term vitality outlook, Henry Hub’s pure gasoline worth in 2Q 2022 is predicted to be $2.87 per thousand cubic toes, then enhance within the second half of the 12 months, as international locations begin preparing for the winter season (see Determine 6). You will need to know that Tourmaline has a complete storage capability of 4.0 billion cubic toes which permits for the chance to inject in intervals of decrease commodity costs and withdraw in intervals of upper costs. Because of increased costs and better manufacturing, I count on Tourmaline’s pure gasoline gross sales to extend within the second half of 2023, reaching its estimated money circulation and free money circulation by the top of the 12 months. Additionally, WTI crude oil worth decreased to $67 per barrel on 17 March; nonetheless, elevated up to now two weeks. On one hand, the excessive world oil inventories and financial headwinds in america and Europe, stop oil costs from rising. However, excessive demand for refineries, ongoing geopolitical tensions in Europe, and the reopening of China help crude oil costs. The WTI crude oil common quarterly worth is predicted to stay between $75 to $78 per barrel within the second, third, and fourth quarters of 2023.

Determine 4 – Pure gasoline spot and futures costs (NYMEX)

Writer (primarily based on EIA’s knowledge)

Determine 5 – LNG Japan/Korea Marker (platts) swap

www.reuters.com

Determine 6 – Vitality costs

eia

TRMLF efficiency outlook

*** On this part, knowledge are gathered from Searching for Alpha and are introduced in USD

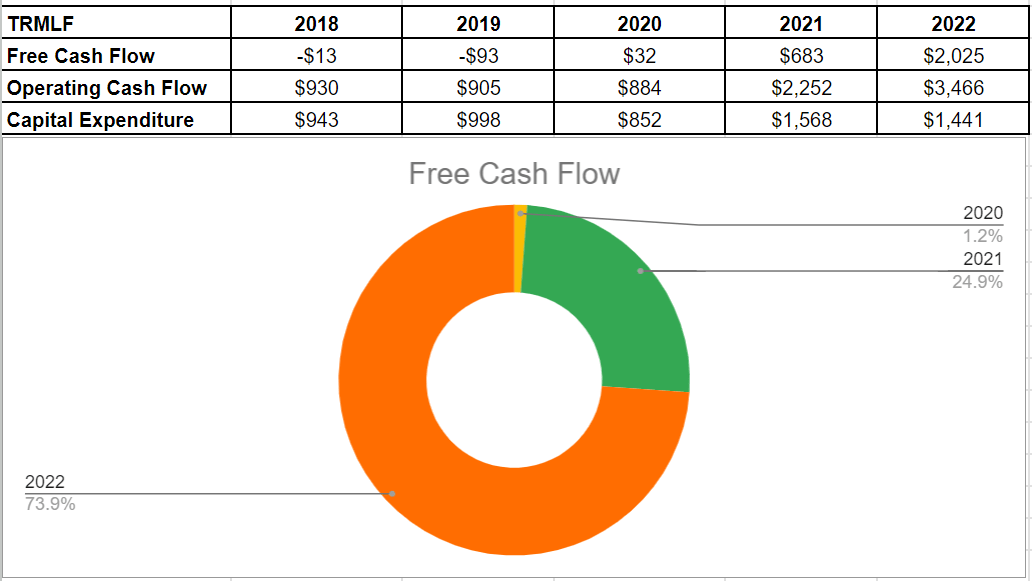

I performed an evaluation of the corporate’s free money circulation development over current years. It was not shocking to search out that the corporate had a promising degree of FCF, provided that they generated a considerable quantity of working money in 2022. A surge of their money operation from $2.25 billion in 2021 to $3.4 billion in 2022, coupled with an 8% lower in capital expenditure from $1.56 billion in 2021 to $1.44 billion, resulted in a lift in free money circulation to over $2 billion by the top of 2022. Tourmaline had the biggest share of FCF at 74% in 2022 in comparison with earlier years. The numerous quantity of free money circulation is indicative of the corporate’s capability to repay debt, repurchase inventory, and foster enterprise progress. Additionally, in 2023 steerage, the corporate anticipated producing $3.8 billion and $2.0 billion money circulation and free money circulation, respectively, which the vast majority of the free money circulation can be returned to shareholders by dividends (see Determine 7).

Determine 7 – TRMLF’s free money circulation (in hundreds of thousands)

Writer

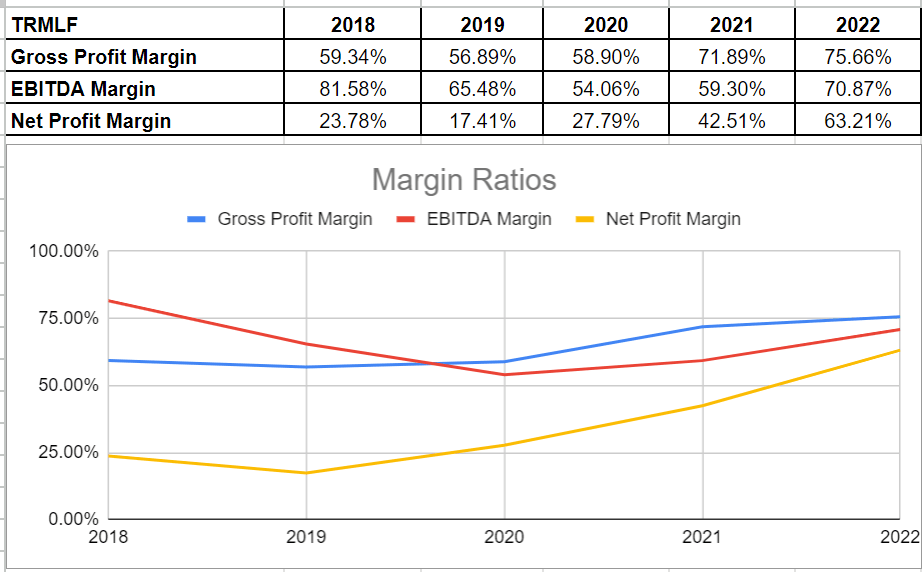

Moreover, I checked out Tourmaline’s profitability ratios to evaluate how properly the corporate can flip a revenue and use its property to become profitable for its traders. I’ve examined the profitability ratios for margin and return ratios to supply helpful insights into the monetary well being of the corporate. I calculated the ratios compared to current years to be extra useful.

Generally, margin ratios consider the flexibility of the corporate to show revenues into income in a variety of methods. It’s indicatable that the corporate had stronger gross revenue, EBITDA, and web revenue margins in contrast with the earlier years. In trivialities, the entire income of Tourmaline elevated significantly by 39%, from $3.7 billion in 2021 to $5.2 billion in 2022. A soar in income mixed with the upper degree of income and EBITDA led to increased margin ratios on the finish of 2022.

TRMLF’s gross revenue margin was 72% in 2021, which is barely decrease than its quantity of 75% on the finish of 2022. Additionally, the corporate’s EBITDA margin was 59% in 2021, which is way decrease in contrast with its quantity of 71% in 2022. Furthermore, Tourmaline’s web revenue margin, which is a last image of how worthwhile the corporate is in spite of everything bills, improved significantly to 63% in 2022 versus its earlier quantity of 42.5% on the finish of 2021. Consequently, the stronger margin ratios are proof of the corporate’s functionality to generate revenue for its traders (see Determine 8).

Determine 8 – TRMLF’s margin ratios

Writer

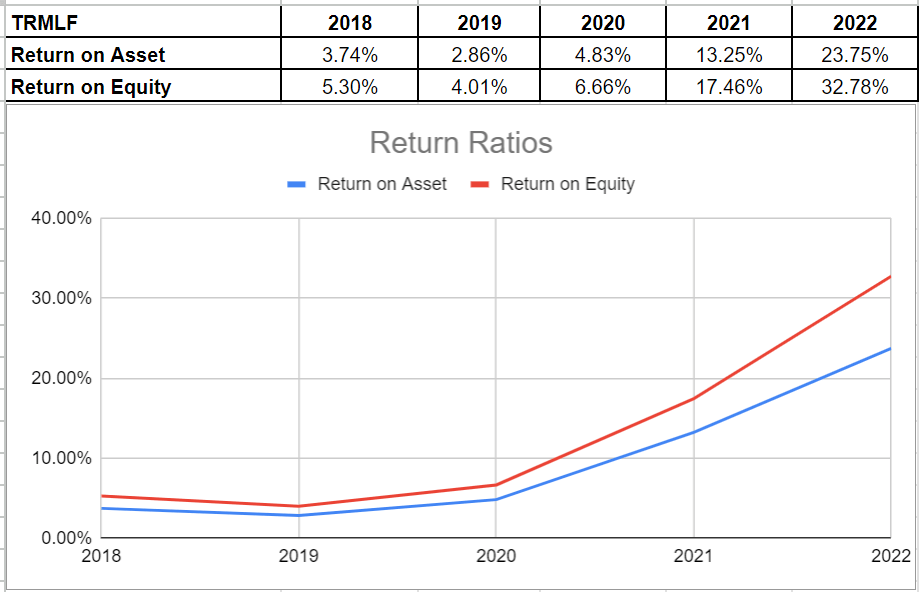

Moreover, I appeared into TRMLF’s return on fairness and return on property ratios to indicate how properly the corporate can tailor returns to its shareholders. The ROA ratio illustrates the quantity of revenue an organization could produce for every greenback of its property. The ROA ratio of 13.25% for Tourmaline in 2021 surged by 1050 bps in contrast with its degree of 23.75% on the finish of 2022. Moreover, its return on fairness of 32.78% in 2022 is way increased than 17.46% in 2021. ROE ratio reveals the corporate’s web revenue regarding shareholders’ fairness and is necessary because it calculates the speed of return on the capital invested within the enterprise. The corporate’s web revenue of $1.6 billion in 2021 was boosted to $3.3 billion in 2022 and thus affected its return ratios (see Determine 9).

Determine 9 – TRMLF’s return ratios

Writer

Abstract

Tourmaline benefited from hiked vitality costs in 2022 and was in a position to enhance its monetary ratios. TRMLF’s return on property and return on fairness improved to over 23% and 32% in 2022, respectively. The corporate’s pure gasoline manufacturing is rising and regardless of decrease vitality costs in 2023, Tourmaline is on the proper path. TRMLF inventory is a purchase.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please concentrate on the dangers related to these shares.

{kind=link}