David Livingston/Getty Photos Leisure

Introduction

The 2022 annual report for Warner Bros. Discovery (NASDAQ:WBD) notes that April eighth will mark the one-year anniversary of the mixed firm. Their three strategic pillars are content material creation, distribution & monetization, and a one firm mindset. My thesis is that the streaming economics are bettering as logical selections are made throughout the framework of those pillars.

Content material Spend And Allocation Pushed By Economics

The streaming economics for a lot of firms have been horrible in recent times as we had low rates of interest such that subscribers had been pursued at any price. This has been altering over the previous couple of quarters and WBD has rightsized the content material investments after recognizing that not all content material ought to be handled equally. Administration is bettering the economics of the streaming enterprise by being extra selective with the content material spend. It’s essential to establish which content material drives viewership and which content material doesn’t. On the March 2023 Morgan Stanley (MS) Tech conference, CFO Gunnar Wiedenfels mentioned 20% of WBD’s content material drives 80% of the viewership. As such, it does not make sense for all of the content material to be unique. Within the 4Q22 call, CEO David Zaslav famous that 40% of the content material on HBO drives the vast majority of viewership. Wanting on the remaining 60%, a few of it may be lower, some can go on the AVOD service, some can go on the AdLite service and a few of it may be bought non-exclusively to others:

And having a few of that content material seem on our platform and promote it non-exclusively to others could be very economically helpful. And the excellent news is we have had an actual likelihood to have a look at content material on every of the platforms over the past 2 years. And we might see, as an example, at HBO, the vast majority of viewership of content material on HBO was solely 40% of the content material. So there was 60% that was hardly being considered. And why ought to we have to monetize that as a way to drive shareholder worth. And as soon as we set up this funnel, then we will take issues like the primary season of succession or the second season. We will put that down on our AVOD service. After which if you happen to beloved it, you’ll be able to come up and you would then pay for on AdLite or in subscription. And principally, we create a flywheel of our personal, the place we personal the complete ecosystem, the subscription, the AdLite and the advert free. And we reap the benefits of all of the content material that we now have.

It’s also key to not worth all kinds of viewership equally. There’s a distinction between turning off the lights and actively watching Sport of Thrones in a movie-like expertise versus deciding between the radio and reruns of outdated content material as a passive background whereas doing chores round the home. CEO David Zaslav talked about this within the 4Q22 name, saying Discovery Plus content material is closely considered for hours throughout the day in a passive method whereas HBO is considered with household in a extra intense method. A March twenty eighth WSJ article talks about the truth that Emmy Award-winning Succession is the enduring kind of content material that’s actively considered and worthy of a big funds:

Viewership of Sunday’s premiere of “Succession” exceeded the season two premiere of one other hit HBO present, “The White Lotus,” by 51%, HBO mentioned. HBO’s steady of high-profile collection, which embody “The Sopranos,” “The Wire” and “Sport of Thrones,” earned it trade plaudits and important viewer numbers.

Giving Prospects Selections

The 2022 annual report says the brand new product providing for streaming will likely be showcased in a press occasion on April twelfth and it’ll have mixed content material from each HBO Max and Discovery Plus. The providing will likely be obtainable in each ad-free and ad-supported tiers. Additionally, CEO Zaslav made it clear within the 4Q22 name that present subscribers will likely be allowed to remain on Discovery Plus as a standalone service:

Simply merely that for people who have Discovery proper now, the churn could be very low and it is worthwhile, Discovery Plus. A lot of these individuals are going to wish to transfer as much as an even bigger product, extra strong with an even bigger providing. For these which can be joyful paying $5 or $7 and having HomeFood Discovery … our technique isn’t any sub left behind. We’ve got worthwhile subscribers which can be very pleased with the product providing of Discovery Plus, why would we shut that off?

Worldwide

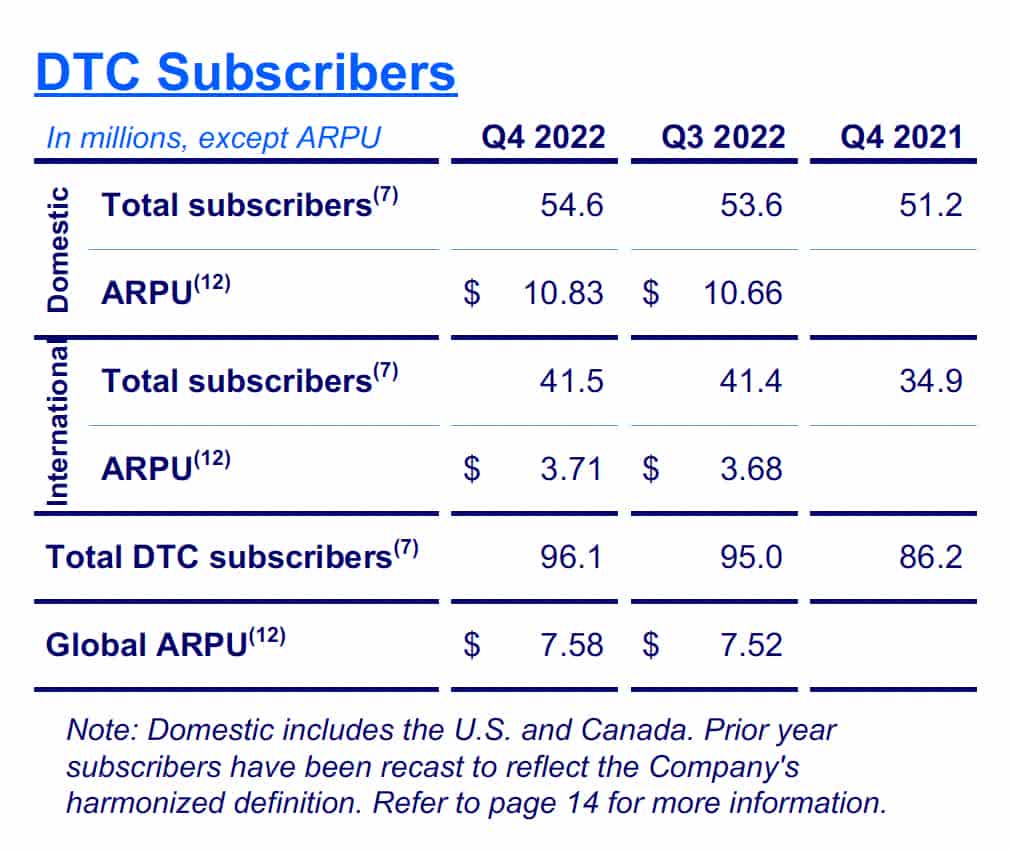

WBD can enhance streaming profitability if they’ll determine easy methods to increase costs internationally with out rising churn excessively. By 4Q22, the month-to-month ARPU for home subs was $10.83 nevertheless it was a mere $3.71 for worldwide subs per the 4Q22 release. WBD raised the month-to-month value for the ad-free tier of its HBO Max streaming service in January by virtually 7%, from $14.99 to $15.99 a month after these 4Q22 figures got here out:

DTC subscribers (4Q22 launch)

Netflix (NFLX) does not have this kind of disparity between US/Canada ARPU and international ARPU. Discovery Worldwide President & CEO Jean-Briac Perrette talked about this within the 4Q22 name saying the worldwide pricing is considerably under market:

It isn’t only a query of subscriber scaling. Sure, that is 1 necessary ingredient. So we do see subscriber scale as 1 a part of the income progress story. We see value as a vital second half. Internationally, as I’ve mentioned earlier than, we take a look at – our pricing is considerably underneath the place we expect the market is. We see churn as a 3rd necessary variable that traditionally has been comparatively greater on the HBO Max product that with the two merchandise coming collectively, that finally coming down is necessary.

Numeric Enhancements

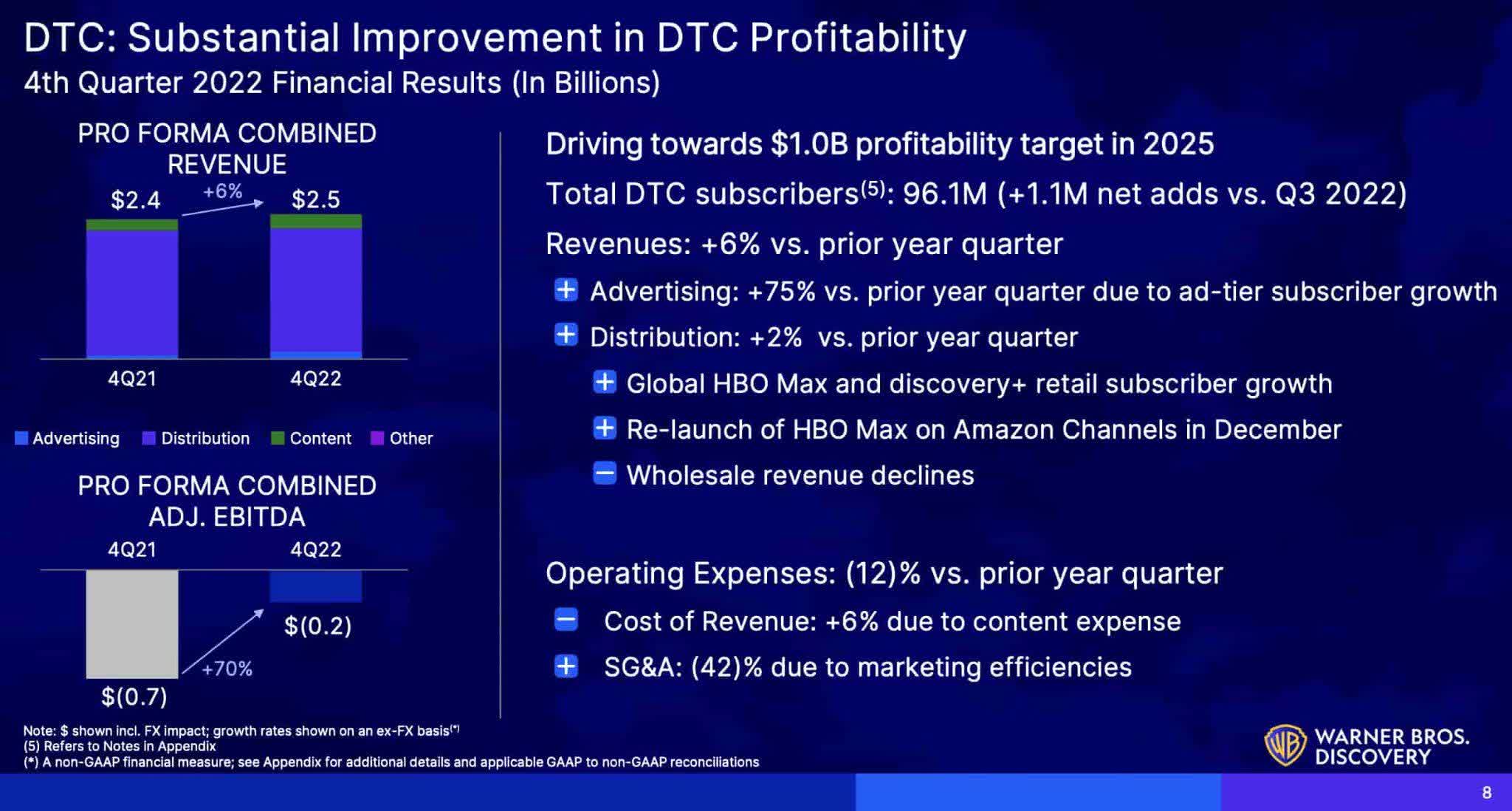

The 4Q22 presentation reveals that professional forma mixed adjusted EBITDA for streaming has improved from $(0.7) billion for 4Q21 to $(0.2) billion for 4Q22. This momentum is anticipated to enhance as WBD drives in direction of their $1 billion profitability goal for 2025:

DTC enchancment (4Q22 presentation)

Within the 4Q22 name, CFO Wiedenfels mentioned DTC ought to enhance to breakeven within the US in 2024 and it ought to rise to have a worldwide 2025 revenue of $1 billion. LatAm is an space the place he thinks income may be elevated:

We’re analyzing our pricing technique in quite a few key worldwide markets, notably in LatAm, the place we imagine our service has important pricing upside. Primarily based on the traction we’re seeing throughout the broad spectrum of operational and monetary KPIs, we count on section EBITDA to be roughly breakeven in Q1, which suggests one other $500 million enchancment year-over-year, roughly in step with the advance seen in This fall.

Valuation

Within the 4Q22 name, CFO Wiedenfels mentioned general adjusted EBITDA ought to go as much as the $11 billion vary in 2023.

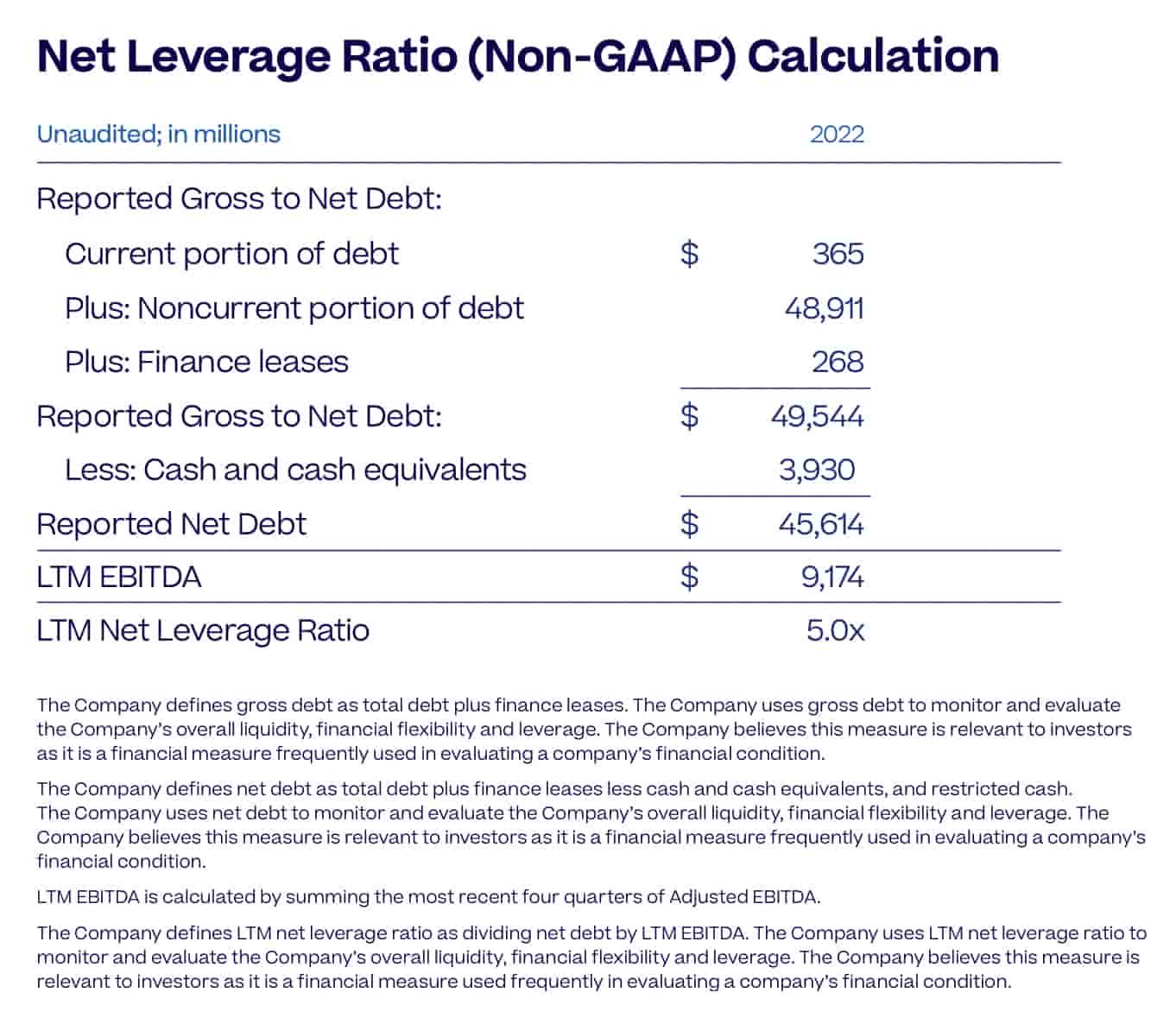

As a result of an infinite debt load, the enterprise worth for WBD is far greater than the market cap. Within the 2022 annual report, CEO Zaslav talked about the truth that $7.3 billion of debt was paid in 2022:

We’ve got demonstrated our capacity to generate significant free money stream with greater than $3.3 billion reported in 2022, and we paid down $7.3 billion of debt in 2022. We additionally count on to cut back our web leverage from 5x on the shut of 2022 to comfortably under 4x by the top of 2023.

Once more, general free money stream (“FCF”) for 2022 was $3.3 billion or $4,304 million – $987 million. The 2023 steerage states they proceed to count on 1/third to half of adjusted EBITDA to transform to FCF. They are saying this could enhance to 60% in the long term. Adjusted EBITDA for 2022 was $9,174 million however $434 million of that was share-based compensation so my adjusted EBITDa determine is $8,740 million. I believe an inexpensive valuation vary is 9 to 11x my adjusted EBITDA determine or $79 to $96 billion.

The 2022 10-Ok reveals 2,430,029,982 shares as of February 9, 2023. The market cap is $35.6 billion based mostly on the March twenty ninth share value of $14.66.

Per the 2022 annual report, the web debt is $45.6 billion:

Internet leverage (2022 annual report)

The enterprise worth is $82.8 billion which is $47.2 billion greater than the market cap attributable to $45,614 million in web debt, $318 million in redeemable non-controlling pursuits and $1,254 million in common non-controlling pursuits.

Sitting inside my valuation vary, the enterprise worth seems like it’s in a great place and I believe the inventory within reason valued.

Ahead-looking buyers ought to tune in for the April twelfth press occasion that can showcase the brand new product providing for streaming.

Disclaimer: Any materials on this article shouldn’t be relied on as a proper funding suggestion. By no means purchase a inventory with out doing your personal thorough analysis.

{kind=link}