JillLang

I have been shopping for Healthcare Realty Belief (NYSE:HR) in latest weeks as REITs pulled again in response to sticky inflation numbers and feedback from the Fed that they are keen to maintain base rates of interest increased for longer. HR is an internally managed medical workplace constructing (“MOB”) REIT with a 688-property portfolio on the finish of its fiscal 2023 fourth quarter. That is unfold throughout 40.3 million sq. toes and 35 states. HR focuses on Class A MOBs concentrated in medical clusters of fast-growing Solar Belt markets. Dallas and Houston type its two prime places at 8.9% and 4.6% of its portfolio respectively.

Healthcare Realty February 2024 Supplemental Data

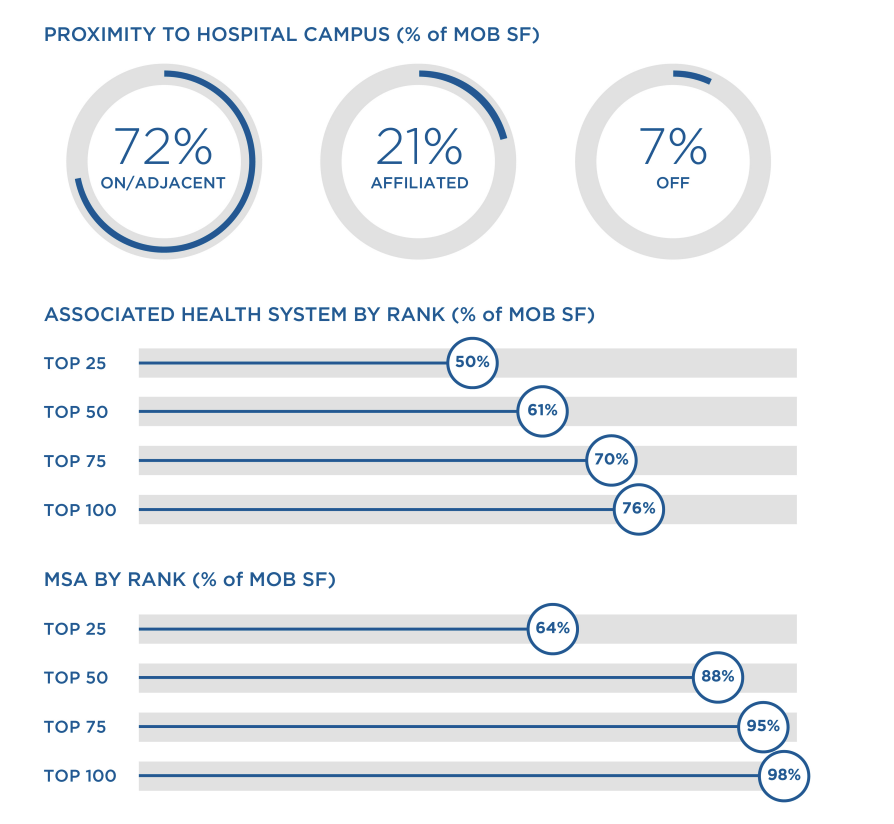

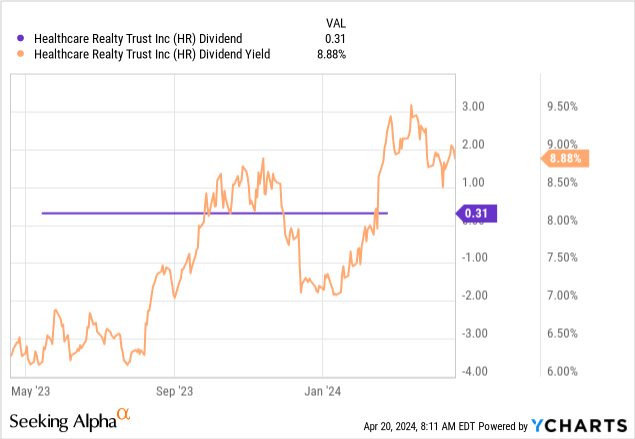

The REIT has located 72% of its MOB portfolio in clusters on or round hospital campuses to drive efficiencies in leasing and tenant providers. This technique additionally helps type a moat towards any new MOB provide, because the REIT is ready to profit from a broad development in outpatient care and because the US inhabitants ages. HR final declared a quarterly money dividend of $0.31 per share, left unchanged sequentially, and $1.24 per share annualized for an 8.8% dividend yield. This could be amongst the best yield in HR’s historical past if we adjusted out the irregular selloff on the onset of the pandemic.

Right here lies the chance for the bulls, as a dividend yield that has moved to sit down near its highest-ever stage since HR grew to become a public entity in 1993 has offered a chance to construct and develop a median value base on the commons that captures this abnormality. HR sits on the intersection of a tripartite of bearish components which have left shares buying and selling at a low a number of to annualized fourth-quarter NFFO. Client inflation has remained sticky, base rates of interest stay at 22-year highs, and investor sentiment towards office-focused REITs has cratered towards the work-from-home zeitgeist.

| HR | |

Market capitalization | $5.4 billion |

Annualized dividend | $1.24 per share |

Dividend yield | 8.9% |

Dividend protection (Annualized 2023 fourth quarter NFFO) | 125% ($1.56 per share) |

Worth to annualized 2023 fourth quarter NFFO | 9x |

Credit standing | “BBB“ |

Geographic unfold | US solely |

1-year return | -30% |

NFFO And 2024 Steering

HR is presently topic to the discounting of workplace REITs regardless of MOBs being a wholly completely different property sort from normal company workplace buildings. The REIT recorded a fourth-quarter normalized funds from operations (“NFFO”) of $0.39 per share, and $1.56 per share annualized. Fourth quarter NFFO was according to analyst consensus however dipped by 3 cents from NFFO of $0.42 per share a yr in the past. HR is basically now swapping fingers for 9x its annualized 2023 fourth-quarter NFFO, roughly 30% below its peer group median.

Healthcare Realty February 2024 Investor Presentation

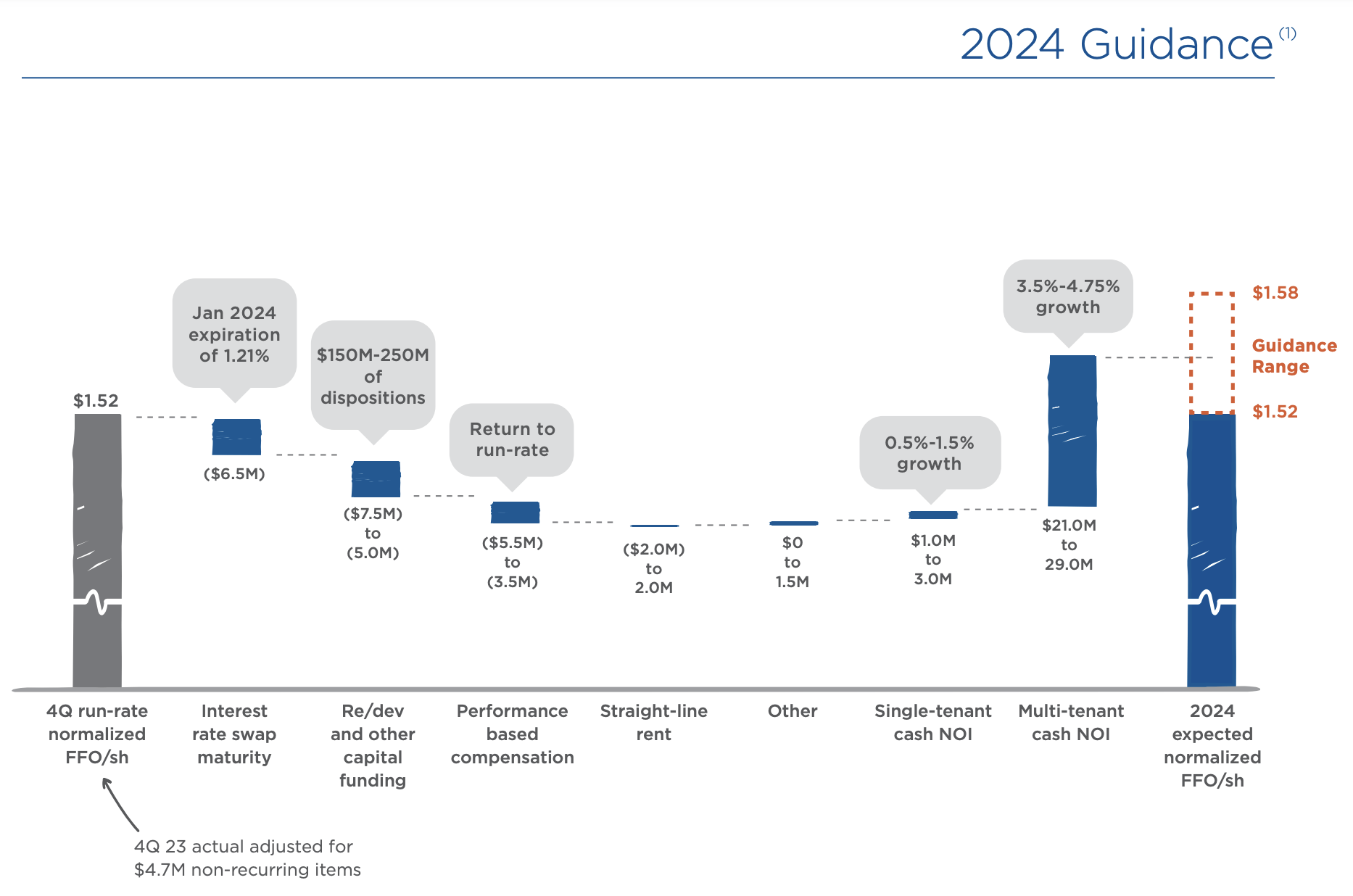

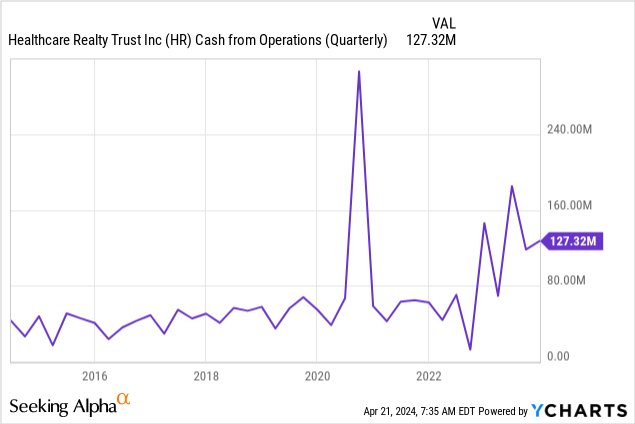

The REIT is guiding for 2024 NFFO of $1.52 per share to $1.58 per share. This could symbolize a development of 6 cents, roughly 3.9% year-over-year development on the prime finish of the vary. That is set to be pushed by multi-tenant money internet working revenue (“NOI”) development of between 3.5% to 4.75%. HR’s money from operations got here in at $127.32 million on the finish of the fourth quarter, with the REIT’s money and money equivalents place ending the quarter at $25.7 million.

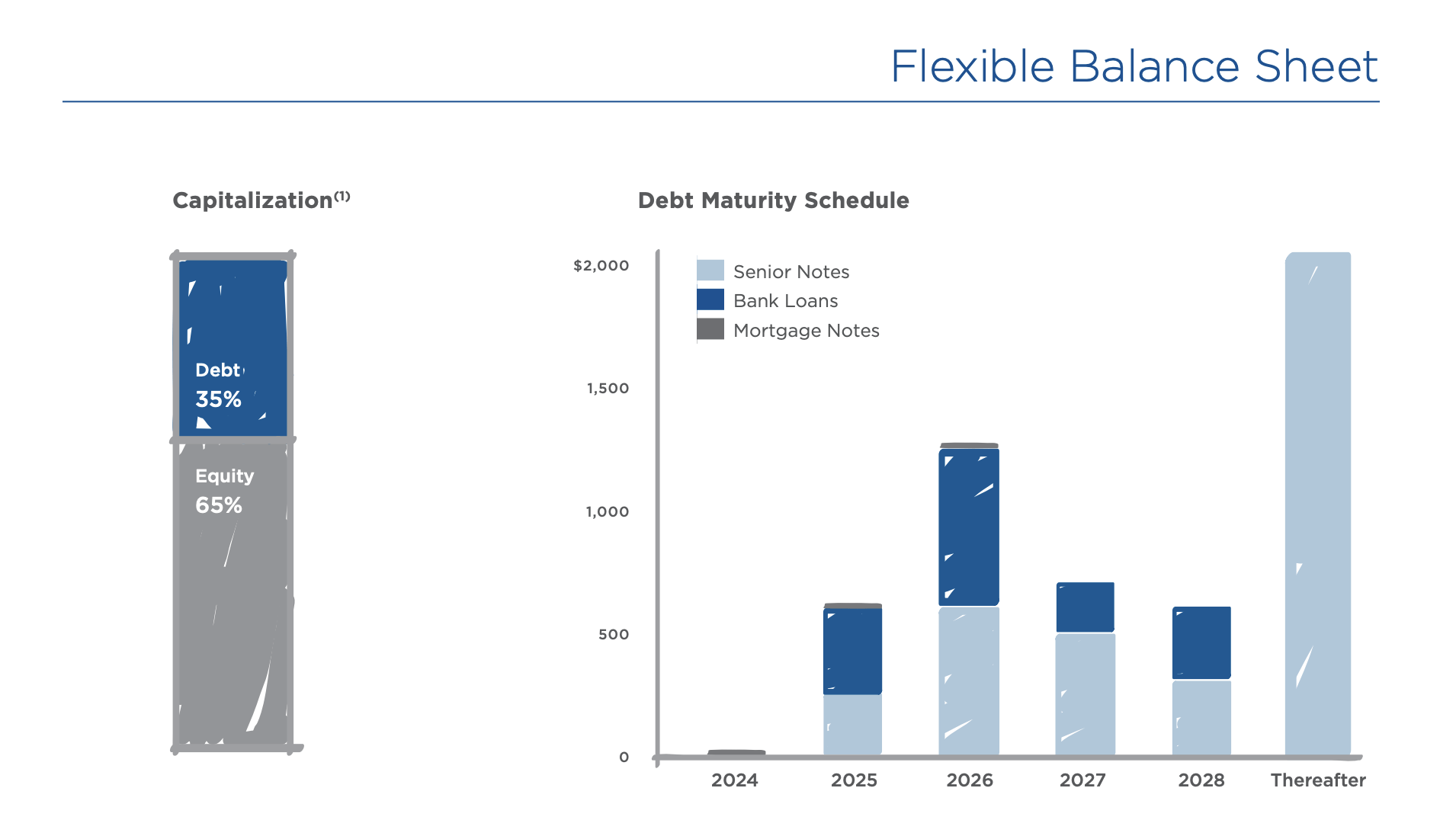

Debt Maturities And Progress

HR spent a outstanding $472 million in dividend funds by means of its fiscal 2023, a big development from $283.7 million within the prior yr following the REIT’s merger with Healthcare Belief of America. This merger was accomplished simply because the Fed’s combat with inflation started to ramp up, with the inventory down materially since then. HR faces no actual debt maturities in 2024 with its portfolio common years to maturity at roughly 4 years as of the tip of the fourth quarter.

Healthcare Realty February 2024 Investor Presentation

Critically, HR continues to file development because it guides for continued development by means of 2024. The REIT’s mixed complete same-store money NOI elevated by 2.7% throughout its fourth quarter, towards a median in-place lease improve of two.8%. Outpatient amenities, the place physicians can supply routine consultations, check-ups, and minor remedies, are set to see continued demand development. The REIT’s leverage can be manageable, with its internet debt to adjusted EBITDA of 6.4x inside its anticipated vary of 6.0x to six.5x.

Fitch Rankings

The REIT was additionally rated, albeit now withdrawn, funding grade at ‘BBB’ by Fitch Rankings in the summertime of 2023. That is an funding grade-rated REIT with a high-quality Class A MOB portfolio and a near-9% dividend yield that’s buying and selling markedly under its historic vary. The REIT ought to be capable of meet its dividend funds on the midpoint of its 2024 NFFO steering vary. Therefore, I am snug taking a place right here with the commons being rated as a purchase.

{kind=link}