Now, Let’s Get into the Particulars of the Maths

This equation estimates the return an investor can count on from an funding. It takes into consideration the change within the asset’s worth in native forex (r) and the change within the alternate price (f𝑥).

To elucidate it in our instance:

Let’s assume a US investor is concerned about a European property valued at €100 million. On this situation, the investor is worried with the modifications within the property’s worth and the Euro’s worth towards the US greenback. The European property is appreciated from €100 million to €103 million.

In educational jargon, this phrase can be included in analysis papers on finance.

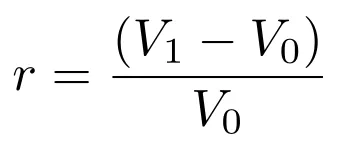

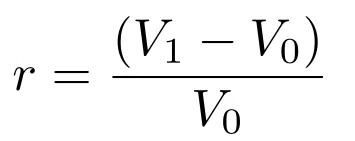

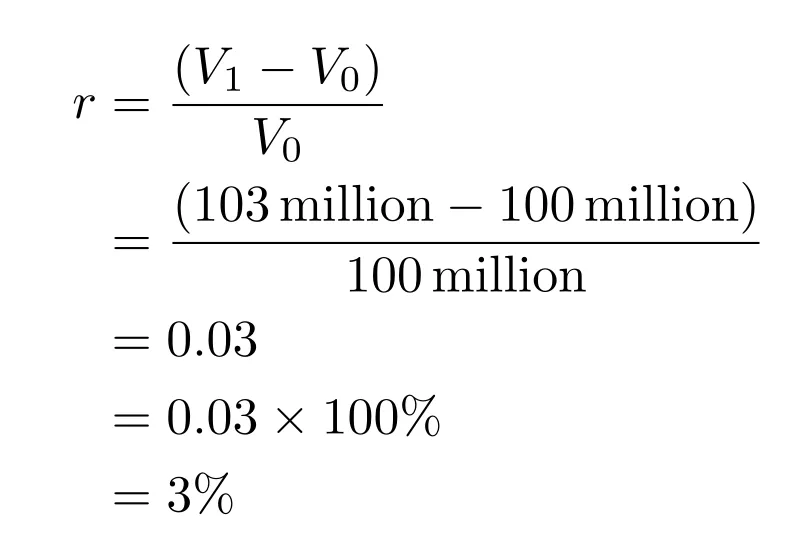

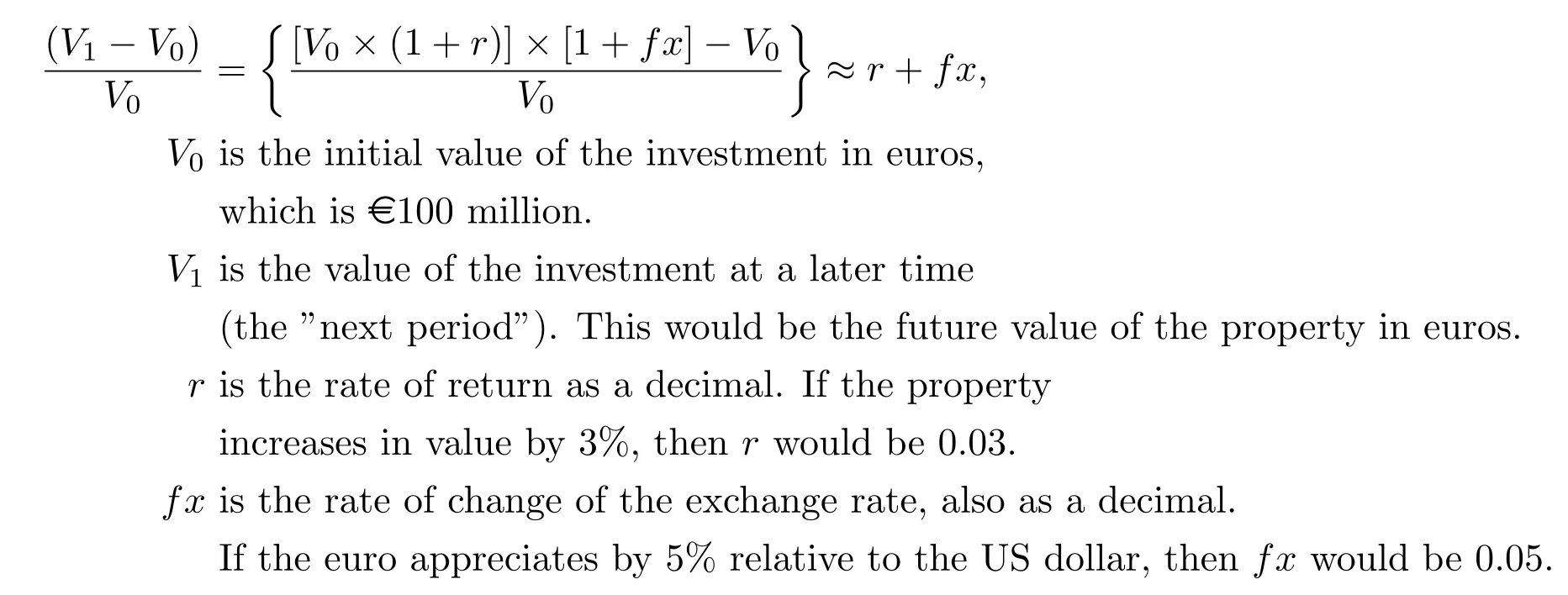

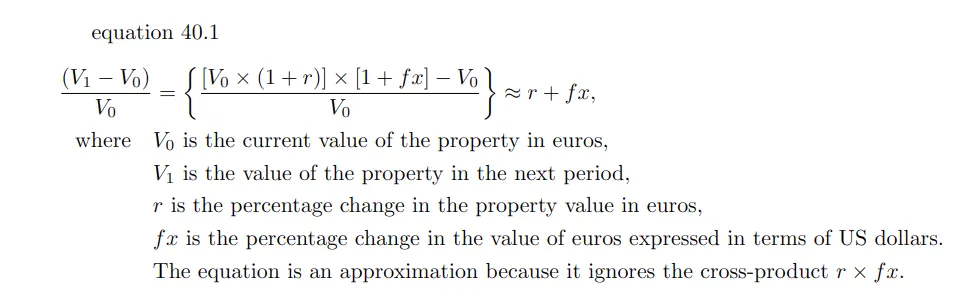

For instance, to the US investor, a property with a present value, V_0, of €100 million may be considered as having a return R, based mostly on the subsequent interval worth V_1, as proven on this equation:

(V_1- V_0)/V_0 = {[V_0 * [1 + r] * [1 + fx]] – V_0 ≈ r + fx

I’ll make the equation extra readable with LaTeX.

Equation 40.1

Observe phrase:

“V_0, of €100 million may be considered as having a return R, based mostly on the subsequent interval worth V_1”

V_0 is €100 million, and V_1 is €103 million, but we don’t know “r” but. So, let’s determine that out.

The full proportion acquire or loss within the worth of the full funding is denoted by “r,” which tells us how a lot our funding is value in comparison with after we first invested.

We have to learn the way a lot the property’s worth modified if we purchased it for €100 million and it’s now value €103 million. The change in worth (€103M — 100M) is €3 million.

€103 million — € 100 million = €3 million

Subsequent, we need to see how this alteration is relative to what we paid, so we divide the €3 million by the unique €100 million.

(103 million — 100 million) / 100 million

On this case, dividing €3 million by €100 million offers us 0.03, however to show this right into a proportion, we multiply by 100, which provides us 3%.

Did you waste my time studying to provide me a fundamental rationalization of learn how to calculate the share beneficial properties/losses? Sure, sure, I did.

We’ve got confirmed that our acquire on the property is 3%.

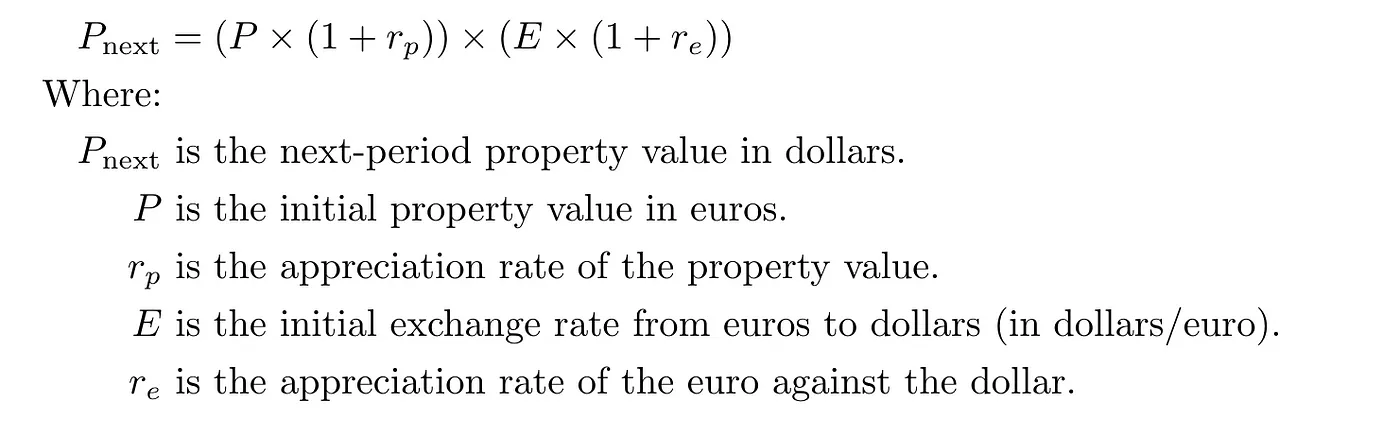

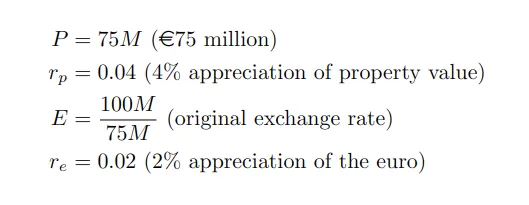

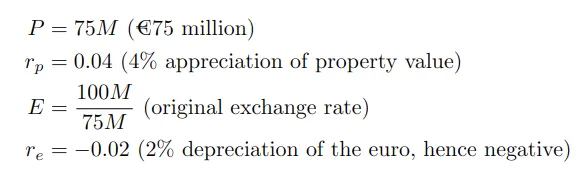

Suppose we’re a US investor shopping for European property at €75 million with our bucks. We hope for a 4% enhance within the property’s greenback worth over the 12 months.

Let’s simplify the mathematics and assume €75 million is value $100 million. We bought this European property value €75 million and paid $100 million.

What occurs to our bucks if the Euro appreciates or depreciates towards the greenback?

State of affairs 1 (Euro Appreciates):

- Property worth up 4%

- Property worth: 75 * (1 + 0.04) = €78M

- Euro appreciation: 2%

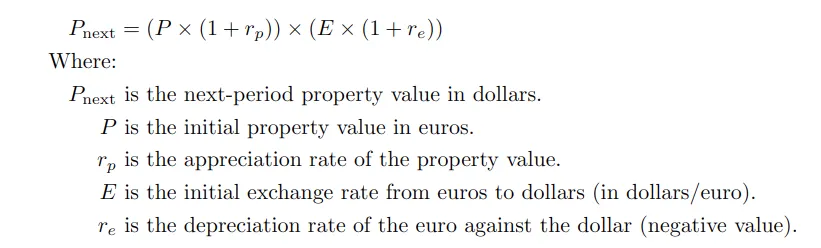

Now, to seek out the “Subsequent-period property worth in {dollars}” denoted as P_next:

In our case:

By plugging within the numbers, we get:

P_next = (75 × (1 + 0.04)) × ((100÷75))×(1+0.02) = $106.08M

State of affairs 2 (Euro Depreciates):

- Property worth enhance: 4%

- Subsequent-period property worth: (€75M * 1.04) * 0.98 = €76.44M

- Euro depreciation: -2%

- Subsequent-period property worth in {dollars}:

Now, to seek out the “Subsequent-period property worth in {dollars}” denoted as P_next:

In our case:

By plugging within the numbers:

P_next = (75×(1+0.04)×(100÷75)×(1−0.02)) = $101.92M

So, you managed to buy property abroad, and even when the native value of the property doesn’t transfer, the worth again house can swing simply because of the forex alternate charges.

You’ve purchased your property in Europe, and the Euro would possibly fall towards the greenback (EUR/USD down), and instantly, your property isn’t value as many {dollars} as earlier than.

Your funding value in your “house forex” (let’s say {dollars}) can soar round even when the value of your property within the “native forex” (let’s say Euro) has stayed the identical.

It’s not nearly property worth. It’s additionally in regards to the international alternate recreation you’re collaborating in. With out heading, you’re just about partly playing.

Key conventional forex threat assumptions of cross-border investing

When investing in actual property throughout borders, it’s necessary to concentrate on forex threat because you’re not directly taking part in the international alternate market.

A typical perception in forex threat administration is that fluctuations within the worth of the investor’s house forex can affect the worth of their international funding.

Which means if the forex within the nation the place you may have invested (for instance, the Euro) strengthens or weakens towards your own home forex (for instance, the US greenback), it should have an effect on your returns.

As an example, if an American investor’s European asset appreciates by 4% in USD phrases, conventional knowledge suggests that is impartial of the USD’s market efficiency. That viewpoint implies that proudly owning international belongings inherently entails forex threat.

Nonetheless, this won’t maintain in important forex devaluation or inflation situations.

In such conditions, the nominal worth of actual belongings, when calculated within the inflating forex, tends to reflect the excessive inflation price.

start{align*}

frac{(V_1 - V_0)}{V_0} &= left{ frac{[V_0 times (1 + r)] occasions [1 + fx] - V_0}{V_0} proper} approx r + fx,

textual content{the place} quad & V_0 textual content{ is the present worth of the property in euros,}

& V_1 textual content{ is the worth of the property in the subsequent interval,}

& r textual content{ is the share change in the property worth in euros,}

& fx textual content{ is the share change in the worth of euros expressed in phrases of US {dollars}.}

& textual content{The equation is an approximation as a result of it ignores the cross-product } r occasions fx.

finish{align*}Bear in mind the equation above, which helps us perceive the mixed impact of the property’s worth change and the forex alternate price in your funding’s general worth.

So image this: you’ve bought a property the place the native forex, say the Euro, is taking a nosedive in comparison with the US greenback. In finance, we’d count on the return of the property (that’s our pal “r” in Equation 40.1) to reflect this.

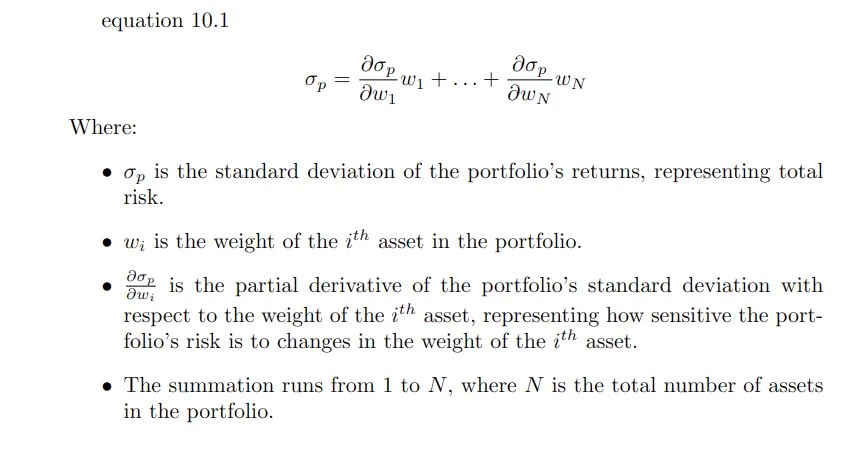

When investing in properties throughout completely different international locations, you’re taking part in a twin recreation of actual property and international alternate markets. Right here’s the place Equation 10.1 turns into related.

Equation 10.1

start{equation}

sigma_p = frac{partial sigma_p}{partial w_1} w_1 + ldots + frac{partial sigma_p}{partial w_N} w_N

finish{equation}

The place:

start{itemize}

merchandise $sigma_p$ is the usual deviation of the portfolio's returns, representing whole threat.

merchandise $w_i$ is the burden of the (i^{th}) asset within the portfolio.

merchandise $frac{partial sigma_p}{partial w_i}$ is the partial by-product of the portfolio's normal deviation with respect to the burden of the (i^{th}) asset, representing how delicate the portfolio's threat is to modifications within the weight of the (i^{th}) asset.

merchandise The summation runs from 1 to (N), the place (N) is the full variety of belongings within the portfolio.

finish{itemize}This equation helps us decide how our entire funding is predicated on the danger of every funding (like properties and forex holdings) and the way a lot of our cash is in every half.

In actual case situations, if the forex through which an funding is made devalues considerably, say by 25%, the property’s worth in that forex could enhance considerably.

This helps to take care of the property’s actual worth. Conventional fashions usually overlook this risk.

It’s not simply in regards to the property’s price ticket; it’s additionally about how forex values and financial circumstances within the funding nation can have an effect on your returns.

Accessing international belongings with futures and Quanto futures

In finance, fairness futures contracts are monetary devices the place buyers agree to purchase or promote a selected inventory index or particular person inventory at a predetermined value on a future date.

I assume the reader has a fundamental understanding, however let’s assessment it simply in case.

Fairness futures are contracts you make with somebody to purchase or promote shares at a set value on a future date. You don’t really get the shares; you compromise the wager with money. Merchants use these contracts to guard towards dangers or to attempt to generate profits from anticipated value modifications. They’re helpful as a result of you possibly can commerce lots with a little bit bit of money with leverage.

So, at expiration, the client and vendor settle the distinction between the contract and market costs in money. There’s no bodily alternate of the particular shares or indices. Then again, oil futures usually contain bodily supply.

(Bear in mind in the course of the COVID pandemic, when oil futures ended up buying and selling negatively as a result of nearly no person needed bodily oil supply at their door).

These contracts are usually linked to the efficiency of indexes such because the SPX500. They’re traded within the forex of the underlying belongings. As an example, if the futures contract is predicated on the SPX500 index within the U.S., it might be traded in U.S. {dollars}.

How does that work? It’s fairly simple.

Every contract has a selected greenback worth assigned to every level motion of the index. Contemplate a contract valued at $250 per level. If the SPX500 index rises by 2 factors, a market participant holding a “lengthy” place (wager on the index rising) would acquire $500.

That revenue is calculated as:

contract worth * factors = PNL

$250 * 2 = $500A Quanto by-product takes this idea a step additional.

What Are Quanto Futures?

Do you Quanto? Have you ever ever heard about quanto derivatives? Quanto merchandise are a kind of by-product that gained reputation over time on account of their skill to mitigate international forex threat.

Quanto merchandise, generally known as “currency-linked derivatives,” had been initially developed within the late Nineteen Eighties to fulfill the calls for of buyers who needed to take part within the explosive rally in Japanese shares and keep away from the danger related to fluctuations within the Japanese Yen.

In the course of the late Nineteen Eighties, the recognition and acceptance of quanto merchandise led to the speedy globalization of monetary markets. These monetary devices had been designed to successfully handle cross-border funding threat by offering buyers with publicity to international belongings with out exposing them to the dangers related to forex fluctuations. This innovation was a major growth that helped to enhance and streamline worldwide funding actions.

It’s a kind of monetary by-product the place the payoff is adjusted based mostly on a sure amount, often involving a international alternate price. In essence, quanto derivatives mix the hypothesis of the value motion of an asset with the potential fluctuations in alternate charges.

These merchandise are designed to have their payouts in a home forex, though the underlying belongings are priced in foreign currency echange. They make sure that it doesn’t matter what forex your funding is in, you get your returns in your house forex.

Let’s say you’re an American investor; Quanto merchandise help you spend money on international belongings together with your {dollars} with out worrying in regards to the forex alternate price of the international forex you’ve invested in.

Who coined the time period “Quanto derivatives”, and the place did this “Quanto” originate from?

Now, it’s value asking, “Who got here up with this genius concept?” Properly, so far as I do know, it’s a thriller. The time period “quanto” is believed to have first appeared amongst a workforce of merchants at Salomon Brothers. Salomon Brothers was well-known for creating new methods to handle forex threat. At Salamon, they used “quanto” to explain derivatives linked to international forex indexes.

The story originated from a hopeful interviewee drenched from a 6-block stroll and walked into Cooper Neff’s workplace in Philadelphia. Cooper Neff was a famend proprietary buying and selling agency identified for its progressive methods in choices buying and selling and different monetary derivatives. They had been additionally identified for his or her grueling, rigorous interviews.

In the course of the interview, the candidate was introduced with a difficult query that included Siegel’s Paradox.

The query was one thing like this: The USD/DM (U.S. Greenback/German Deutsche Mark) alternate price is 1. It has an opportunity of rising to 1.50 or dropping to 0.50 with equal likelihood. What’s the truthful worth?

Basic math suggests the truthful worth is 1.00 USD.

Now, let’s flip or invert it to DM/USD. The speed might both hit 0.67 (1/1.5 = 0.67 ) or soar to 2.00 (1/0.5 = 2). If you common these out, you get an anticipated worth of 1.335 DM, suggesting a good worth of 0.75.

What offers?

The truthful worth is the common of the 2 attainable future charges. Because the common (anticipated worth) is 1 DM per USD, the truthful worth underneath the given assumptions and market circumstances can also be 1 DM per USD.

Let’s go over the mathematics a bit.

USD/DM

Present price: 1 USD = 1 DM

Doable future price: 1.50 DM

Doable future price: 0.50 DM

USD/DM Anticipated worth: (1.5 DM + 0.5 DM) / 2 = 1 (straight ahead)

Truthful worth: (1.50 + 0.50) / 2 = 1 Observe: Truthful worth is common of the 2 attainable futures price

DM/USD (inverted)

1 USD = 1.5 DM

Doable future price: 1 / 1.50 ≈ 0.67 DM/USD

Doable future price: 1 / 0.5 ≈ 2 DM/USD

DM/USD Anticipated worth: (0.67 USD + 2 USD) / 2 = 1.335 USD

Observe: To find out the truthful worth of USD/DM

Calculate the anticipated worth of DM/USD by inverting the 1.335 USD

Truthful worth DM/USD: 1/1.335 ≈ 0.75

Now, somebody new to buying and selling could marvel, “What? How can the identical forex pair have two completely different values?”

I perceive the place the perception got here from. This isn’t a paradox however only a matter of perspective. USD/DM and DM/USD symbolize the identical relationship in another way. They aren’t separate however simply completely different models of measurement. Which means the charges are priced in numerous models. Due to this fact, there isn’t a precise inconsistency or buying and selling alternative.

There isn’t any monetary alternative for buying energy arbitrage, so there isn’t a actual paradox; the distinction comes from how we mathematically work together with these charges, and there’s no “free lunch.”

When forex charges, we discovered that advanced math is typically misused in finance. This consists of misusing ideas like Jensen’s inequality, which may result in misunderstandings in monetary theories and practices. In our case, after we averaged charges like USD/DM and DM/USD and transformed them, we utilized a non-linear perform.

We calculated the anticipated worth by taking the common of future charges after which discovering its inverse via division, which entails non-linear transformation.

Quick-forward a number of years. The Chicago Mercantile Change (CME) launched progressive forex cross-rate contracts priced in USD, like DM/JPY. This was an fascinating growth however didn’t fairly take off as hoped.

Nonetheless, we’re accustomed to the Base and Quote forex.

What are the Two Important Forms of Quanto?

There are two primary sorts of quantos: two-currency quantos and single-currency quantos.

The Two Foreign money Quanto: Think about you’re investing in one thing priced in euros, however you need your return in {dollars}. This sort is initially valued in euros. When it’s time to money in, it’s transformed into {dollars}. For this kind, the place conversion into the home forex occurs, the pricing tends to be extra simple. That’s as a result of the conversion price is thought upfront, making it simpler to calculate the payoff.

The Single-Foreign money Quanto: This one is a bit completely different. Let’s say you’re within the Japanese inventory market and eyeing the Nikkei Index. With a single-currency quanto, though your funding tracks the Nikkei, you’ll get your payout in your good outdated {dollars}. No conversion is required. Such a pricing is extra advanced, the place the payout stays within the home forex with none conversion. On this case, the pricing mannequin takes into consideration any potential fluctuations in alternate charges in the course of the contract’s life.

Quanto choices fundamental

Take quanto choices, for instance. It is a particular kind of choice contract the place the payoff is transformed into a unique forex at a predetermined alternate price. Not like common choices, which repay within the forex of the underlying asset, quanto choices permit buyers to obtain payoffs in a forex of their alternative, utilizing a hard and fast alternate price agreed upon on the contract’s inception.

- Foreign money conversion: Quanto choices are an efficient manner for market individuals to achieve publicity to international markets with out being uncovered to the related forex threat. These choices present payoffs in a forex completely different from the underlying asset’s forex.

- Fastened alternate price: When getting into right into a contract, the alternate price used to transform the payoff from the underlying asset’s forex to the chosen forex is decided and glued. This mounted price stays the identical no matter any modifications out there alternate charges on the time of payout.

- Floating-rate quanto choices haven’t any predetermined alternate price. They provide buyers flexibility but additionally expose them to forex threat. As an alternative, the alternate price used to transform the payoff is decided on the time of settlement.

- Hedging towards forex threat: Quanto choices permit buyers to hedge towards fluctuations in forex alternate charges by locking within the alternate price.

- Payoffs in most popular forex: Buyers have the pliability to obtain payoffs of their most popular forex, which may be extra handy because it aligns with their threat administration.

A quanto choice is completely different from an everyday choice in that it converts the payoff into a unique forex utilizing a hard and fast alternate price set on the contract’s begin. In distinction, an everyday choice has an easy payoff within the underlying asset’s forex.

Think about an everyday choice that pays out $4 on the finish of its time period. Think about a quanto choice with the identical underlying asset and circumstances however a unique manner of dealing with the payoff.

In a quanto choice, the $4 payout is transformed to euros, however not on the present market alternate price. As an alternative, it’s adjusted to a predetermined alternate price, for instance, $1.25 per Euro.

In a quanto choice, the payout of $4 is transformed to euros, however not on the present market alternate price.

As an alternative, it’s adjusted to a predetermined alternate price, for instance, $1.25 per Euro. You will need to word that the $4 payout just isn’t immediately transformed to euros on the $1.25 per euro price acknowledged within the phrases.

Fairly, the payout is transformed to an equal worth in euros, which means the investor receives 4 euros. In the event you convert 4 euros to greenbacks utilizing the predetermined alternate price of $1.25 per Euro, it might equal $5.

4 * 1.25 = 5

As an alternative of a $4 return, it now equals a $5 return.

- The maths for quanto choices is extra advanced than for normal choices as a result of it entails two currencies and an FX threat premium.

This mechanism provides a singular benefit. It shields the investor from the unpredictability of alternate price fluctuations.

In one other case, think about the greenback depreciates 10% towards the Euro, which means that if the present alternate price had been $1.10 per Euro, it might shift to $1.21 per Euro.

1.10 * 1.1 = 1.21If an investor holds a non-quanto fixed-rate funding at $1.25 per Euro, any greenback depreciation will have an effect on the returns when changing to euros.

Regardless of the alternate price fluctuating to $1.21 per Euro, the Quanto by-product with a hard and fast price stays anchored on the predetermined $1.25 per Euro, making it distinctive. This implies the Quanto contract’s investor is protected towards unfavorable market fluctuations brought on by international alternate actions.

Let’s take a look at a sensible instance to grasp this higher. If the quanto by-product ends in a payoff of 10 euros with a floating price underneath regular circumstances, this could be transformed into {dollars} on the prevailing market price.

Given the greenback’s 10% depreciation, the investor would usually obtain $12.10 (10 euros * 1.21 per Euro) as a substitute of $11 (10 euros * $1.10 per Euro) earlier than the depreciation.

Nonetheless, with the quanto contract’s mounted price of $1.25 per Euro, the investor nonetheless receives $12.50 (10 euros * $1.15) regardless of the shift in international alternate.

By locking within the alternate price from the outset, the investor’s return is influenced by the underlying asset’s efficiency and the predetermined alternate price.

Quanto derivatives supply a classy option to hedge forex threat whereas permitting buyers to faucet into international asset markets.

How Do Quanto Futures Contracts Work?

We’re all accustomed to futures contracts. Futures contracts are generally identified agreements that permit events to purchase or promote a inventory index at a predetermined value on particular dates. These contracts may be utilized to hedge or speculate on the value of a specific asset.

Futures contracts permit buyers to handle threat and maximize returns. They will hedge investments to guard towards value fluctuations or speculate on an asset’s value to revenue from them.

In a Quanto futures contract, the underlying asset is often priced in another way than the investor’s house forex. For instance, a Quanto future contract within the U.S. could be based mostly on the Euro Stoxx 50 index, which is denominated in euros, however the contract’s payouts are in U.S. {dollars}.

In a Quanto futures contract, the alternate price is decided and locked in when the contract is created. This price stays the identical all through the contract’s life.

This mounted price calculates the worth of beneficial properties or losses within the underlying asset, equivalent to a inventory index, within the forex used for contract settlement.

Think about you’re within the U.S. and enter a Quanto futures contract based mostly on a European inventory index just like the DAX, measured in euros.

The mounted alternate price for this contract is ready at 1.2 USD for each euro.

If the DAX goes up by 100 euros, you’d usually count on to get the equal of that enhance in your individual forex (USD). Nonetheless, with a quanto futures contract, this 100 euro acquire is mechanically transformed into USD on the mounted price of 1.2, whatever the present market alternate price. So, you’d get $120 (100 euro * 1.2)

In the event you go for a quanto future commerce, you possibly can lock within the alternate price at 1.2 and obtain fee in {dollars}, even when the euro decreases in worth towards the greenback.

For instance, if the EUR/USD alternate price falls by 10%, you’ll nonetheless earn $120 in your commerce. Nonetheless, if you happen to had been buying and selling a non-quanto future, you’d nonetheless earn 100 euros, however the greenback worth can be 10% much less because of the decline within the EUR/USD alternate price. So, as a substitute of incomes $120, the 100 euros would solely be value $108.

By buying and selling quanto futures, you recognize precisely how international beneficial properties or losses will translate into your individual forex, eliminating the uncertainty of alternate price fluctuations.

So, in an everyday situation, you face two dangers if you happen to commerce the Euro Stoxx 50 index, DAX, or Nikkei 225. The index efficiency threat and the forex alternate threat. The mounted alternate price neutralizes the forex threat in Quanto futures. Your payoff remains to be linked to the international asset however transformed into your native forex utilizing this mounted price.

You’re not uncovered to the danger of forex fluctuations; your threat is now purely based mostly on the asset’s efficiency, adjusted by a hard and fast forex price.

How Does a Quanto Futures Multiplier Work?

Notably, most futures contracts are “quantity-adjusted” and use “multipliers” to regulate for the amount.

A contract’s settlement has a multiplier. For instance, a wheat future contract would possibly symbolize 5000 bushes of what, or an S&P500 future contract could be 250 occasions the index worth.

These multipliers merely scale the scale of a single contract to a handy degree. In easier phrases, multipliers make the scale of the contract extra sensible and sizable for buying and selling. They don’t change the basic nature of the danger.

Quanto futures contracts additionally use a type of amount adjustment, however it’s completely different. As an alternative of adjusting the bodily amount of measurement, they alter the payoff utilizing a forex alternate price.

As an example, in a Quanto futures contract based mostly on the Nikkei 225 index, the beneficial properties or losses within the index are transformed into one other forex, like USD, utilizing a predefined alternate price.

For instance, if a Quanto futures contract is predicated on the Nikkei 225 index however settles in USD, and the mounted alternate price is 0.009 (which means 1 Japanese Yen equals 0.009 USD), then 0.009 acts as a multiplier that determines how a lot a acquire or loss in Yen is value in USD.

As defined earlier, Quanto Futures contracts take it a number of steps additional. Quanto futures are a kind of monetary by-product that mixes parts of futures contracts with forex alternate charges.

Quanto Futures stands out from different futures contracts on account of its distinctive characteristic of together with forex alternate charges within the contract. Which means the contract’s efficiency just isn’t solely depending on the underlying asset, equivalent to a inventory index, but additionally on the fluctuations in an alternate price.

To Quanto or To not Quanto? Does the Excellent Hedge Exist?

The concept of the “excellent hedge” is to guard your funding from losses by managing your place measurement and defending your self towards value or forex modifications.

Nonetheless, this perfect just isn’t the truth for many portfolio managers, who are inclined to maintain the share amount mounted. As an alternative, they solely alter their hedge towards forex modifications.

This strategy, sadly, results in a “slippage,” the place the portfolio, although nominally “absolutely hedged,” nonetheless faces some threat publicity.

The method of attaining an ideal hedge may be difficult, particularly when utilizing quanto hedging.

- Sellers and market makers usually demand a “threat premium”. This additional price compensates for potential slippage and errors of their hedge.

- Furthermore, transaction prices and charges can deter frequent changes for excellent hedging.

- Market dynamics, equivalent to shifts within the underlying asset or alternate charges.

- The unpredictable correlation between asset costs and alternate charges.

Some merchants could decide to simply accept the imperfections of their hedge, equivalent to ahead hedging, as a substitute of paying the premium for a quanto hedge.

Ahead contracts don’t require a premium, which can be a bonus. Nonetheless, that is often canceled out by slippage, and the hedge gained’t carry out as anticipated. For many who care about threat, paying for a reasonably priced quanto could be a better option.

This matter may have a separate article. I’ll add extra info right here later.

Crypto Quanto Futures Contracts

Quanto futures are fascinating, and understanding the mechanics behind futures contracts, particularly these of quanto futures, is necessary for novice and seasoned merchants.

Let’s begin with understanding learn how to calculate the worth of Bitcoin (XBT) and US Greenback (USD) in a BitMEX quanto futures contract, making these advanced monetary ideas comprehensible to everybody.

A Bitcoin quanto futures contract permits merchants to take a position on the value of Bitcoin when it comes to USD, however the contract itself and the eventual settlement are in Bitcoin.

So, the payout of those quanto contracts is in a unique forex than that of the asset’s pricing forex, including a layer of hypothesis and hedging potential.

If you wish to signup to BitMEX and desire a 10% low cost. You should utilize my referral hyperlink: https://www.bitmex.com/app/register/vhT2qm

Understanding the Multiplier in BitMEX Quanto Futures contracts

When buying and selling Quanto futures, the one time period that always pops up is the “multiplier.” Though it might sound advanced, it’s really an easy idea that performs an necessary function in figuring out the worth of your wager on Bitcoin (XBT) and US {dollars}.

What’s a Bitcoin Quanto Future Multiplier?

Within the context of a BitMEX quanto futures contract, the multiplier is a selected quantity that helps convert the contract value into the precise worth that merchants work with. Consider it as a secret ingredient in a recipe that determines your closing contract worth. Within the case of BitMEX quanto futures, this multiplier is ready to 1000 Satoshis or 0.00001 BTC.

I do know what you’re pondering proper now. Why use a multiplier in any respect? The reply lies in the way in which futures contracts are structured. The multiplier permits merchants to interact with contracts with out immediately coping with the total value of Bitcoin.

It primarily “scales” the contract to manageable ranges, making it extra accessible for merchants. That is necessary when costs may be extremely unstable, and the total value of a single bitcoin could be prohibitively costly for particular person merchants.

How does the BitMEX Quanto Multiplier Have an effect on Contract Values?

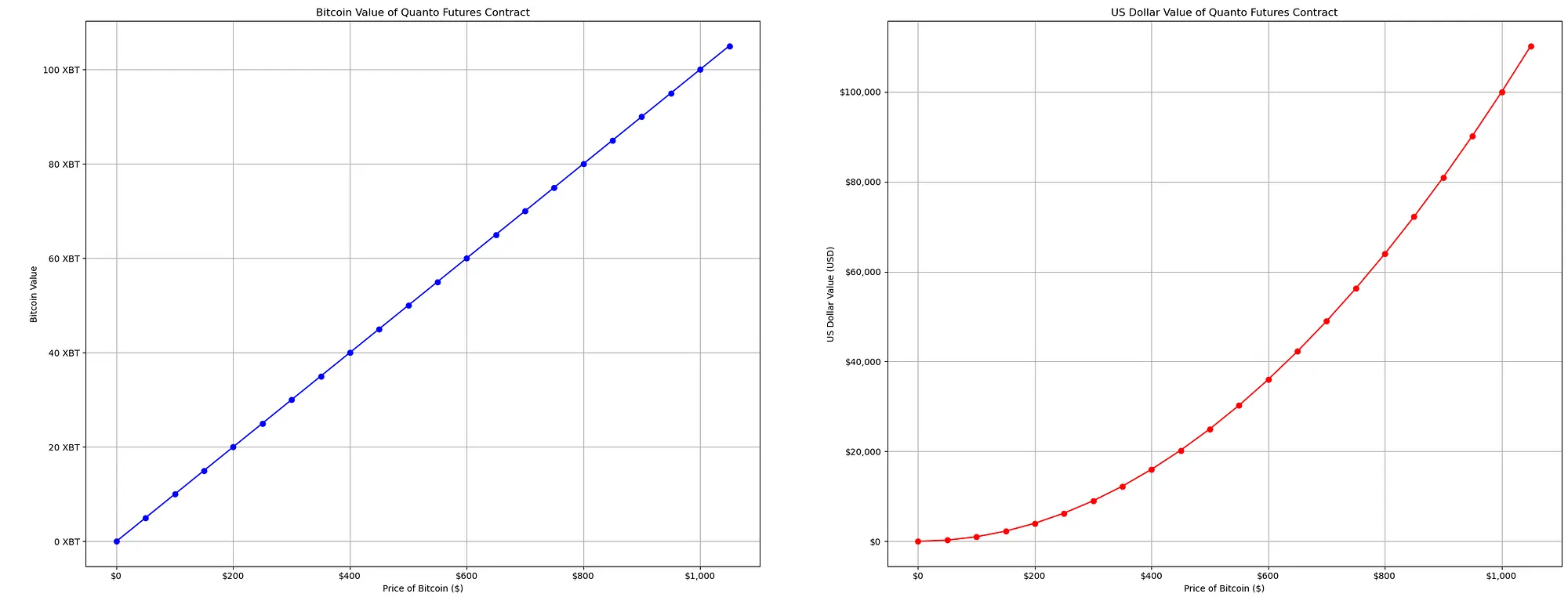

Utilizing our given multiplier of 0.00001 BTC, let’s decide the values of BitMEX quanto futures contracts. This multiplier is utilized to the contract value and the variety of contracts to calculate the contract’s worth

- For Bitcoin Worth (XBT worth), the calculation is easy: we multiply the contract value by our multiplier (0.00001 BTC) after which multiply by the variety of contracts (10,000 in our instance). This tells us how a lot the Bitcoin contract is value

- The method is barely completely different for USD worth (USD worth) however nonetheless depends on our multiplier. We sq. the contract value, then multiply by the multiplier and the variety of contracts. This calculation offers us the contract’s worth in USD.

Our formulation

Bitcoin worth = contract value * multiplier * variety of contracts

USD worth = value * multiplier * variety of contracts Let’s apply what we’ve realized with this instance for a contract priced at $100

- XBT worth = 100 * 0.00001 * 10,000 = 10 BTC

- USD worth = 100² * 0.00001 * 10,000 = $1000

We will graph our PNL for the value of Bitcoin $0

The calculations begin easy; each XBT and USD values start at 0, as there’s no contract value to multiply.

When the XBT worth is $50, it displays a direct linear relationship with the contract value and is represented by 5 BTC. Nonetheless, the USD worth jumps to $250 because of the contract value’s squaring.

When the Bitcoin worth reaches $100, it doubles to 10 BTC. Nonetheless, the USD worth quadruples to $10,000, showcasing the quadratic enhance.

Supply code for the python script to generate this graph: https://github.com/romanornr/bitmex_pnl_model/tree/main/inverse_futures

At $1000, Bitcoin’s worth reaches 100 BTC, and the USD’s worth skyrockets to $100,000, highlighting the exponential development in greenback phrases.

Right here’s the video I used from BitMEX to put in writing this text: https://www.youtube.com/live/0d1oITE3jDI?si=oMw2CfahRZQtUX9b

I didn’t use their Excel sheets; I simply created some Python scripts that may be modified for particular contracts that will differ, equivalent to Ethereum.

Disclaimer: For demo functions and to align with the right calculations of BitMEX’s Excel sheet, I’m utilizing Bitcoin for Quanto futures. Nonetheless, they don’t have them for Bitcoin anymore, however they do have them for altcoins. The specs of the contracts are barely completely different, so the Python script must be modified.

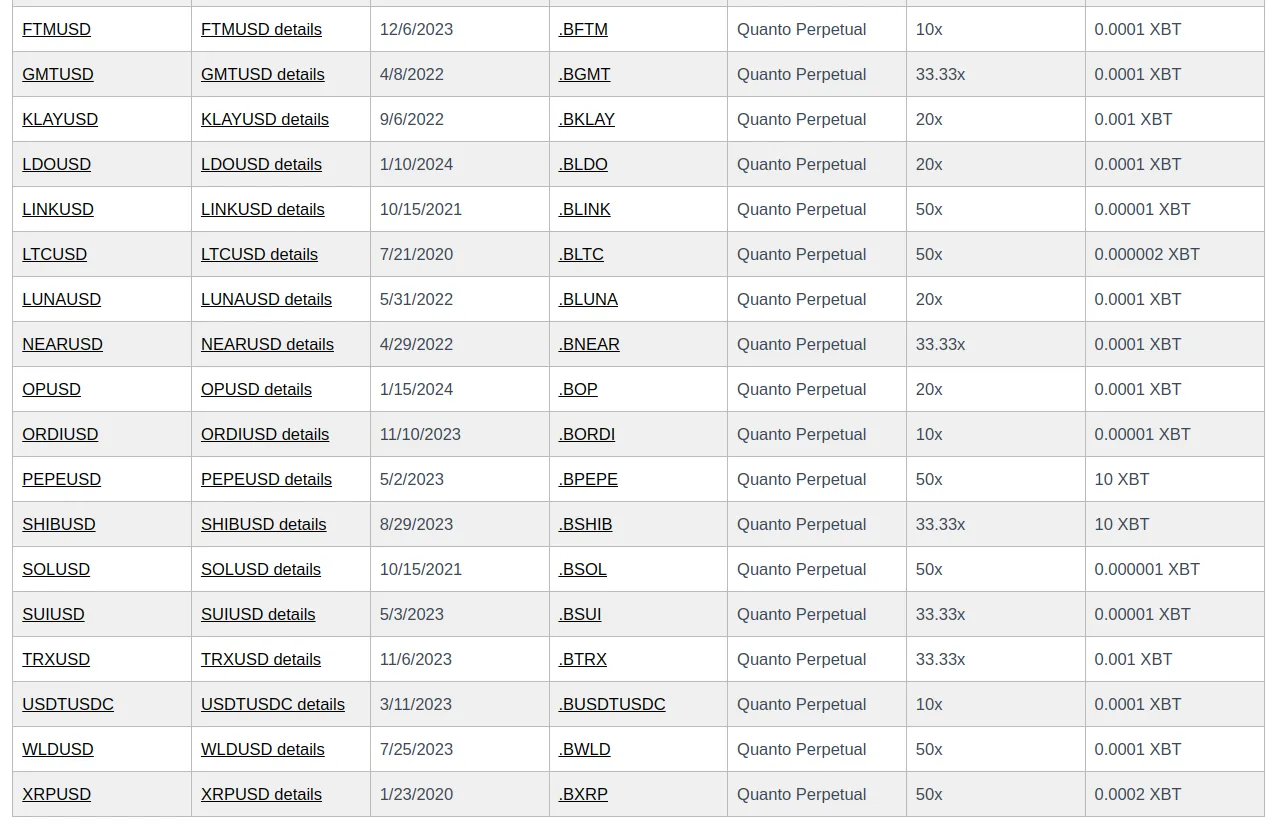

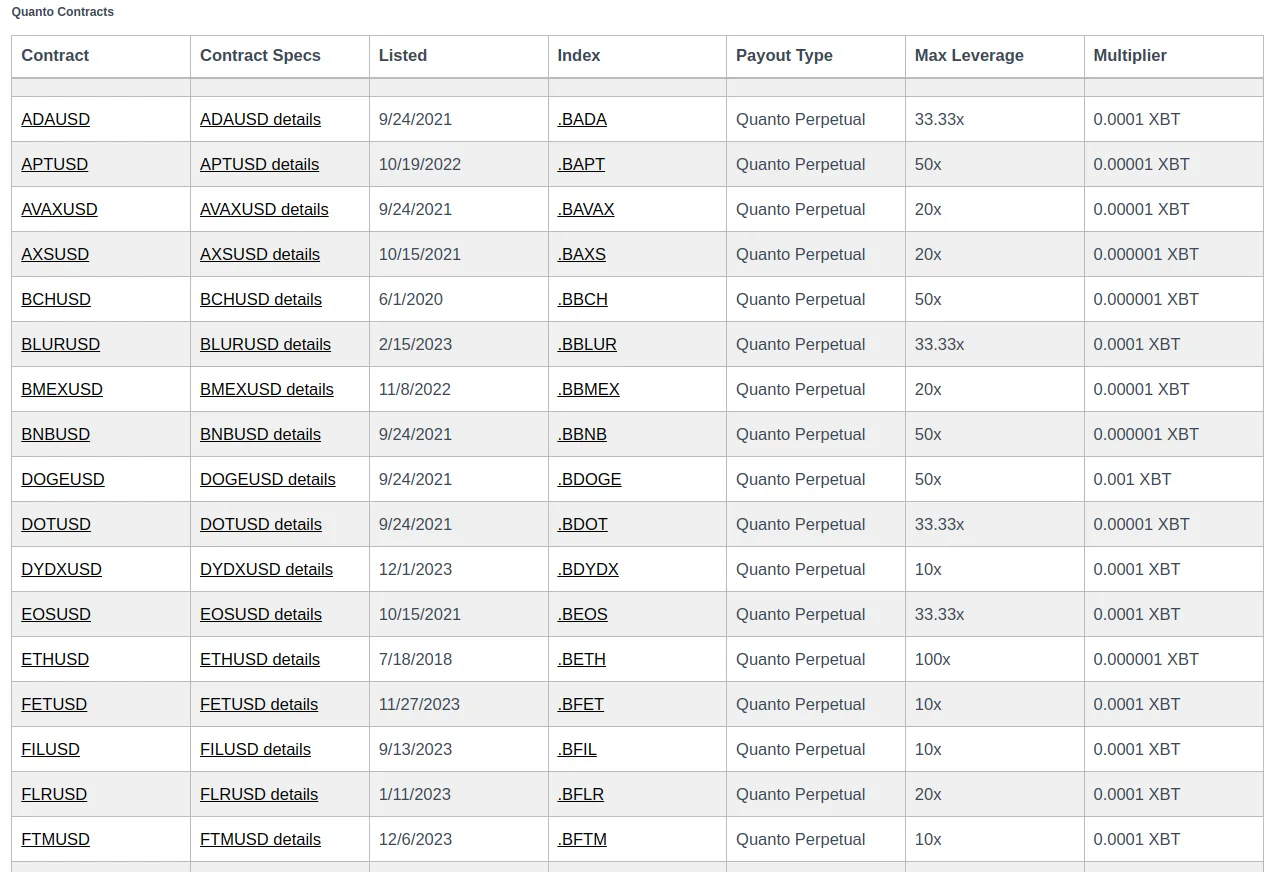

BitMEX has many Quanto futures contracts for altcoins equivalent to Ethereum, BNB, SUI and lots of others. You’ll find them right here: https://www.bitmex.com/app/contractList#Quanto-Futures

What are BitMEX Bitcoin and Altcoin Inverse Futures?

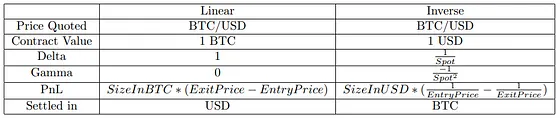

In conventional buying and selling, most contracts you come throughout are simple. If you purchase one among these contracts (let’s say BTC/USD), how a lot you could possibly acquire or lose stays the identical regardless of the Bitcoin value. In the event you enter a commerce and later exit, your revenue or loss is simply the distinction between the shopping for and promoting value.

Nonetheless, an ” inverse ” contract is a unique form of contract. Although it nonetheless offers with Bitcoin/USD, its workings are flipped. As an alternative of your contact’s worth being mounted in Bitcoin, it’s mounted in {dollars}.

BitMEX’s inverse futures contract supplies that. These contracts present a hard and fast worth in US {dollars} tied to the fluctuating value of Bitcoin. What’s nice about them is that they’re straightforward to grasp. To calculate their worth, you multiply the greenback worth of the contract by the variety of contracts you personal.

BitMEX provides a kind of by-product referred to as the XBTUSD Perpetual contract, which is an inverse futures contract. The worth of this contract is linked to the XBT/USD alternate price, which is tracked by the BXBT index. Although each the underlying asset and the swap contract are priced in USD, margins, and PNL are measured in Bitcoin.

Right here’s how this contract is structured:

- The multiplier is ready at $1

- Discover the XBT contract worth, which you do by taking the multiplier and divide by the XBTUSD value

- The USD contract worth is $1

- PnL is calculated utilizing the system: Variety of contracts * Multiplier * * (1/Entry Value – 1/Exit Value)

PNL is realized in BTC, which avoids interplay with USD.

When coping with BitMEX inverse futures contracts, your income or losses usually are not mounted in Bitcoin however in US {dollars}. The contracts are set as much as preserve a continuing greenback worth whatever the Bitcoin value. By way of potential monetary returns, these contracts present a constant quantity in US {dollars} however yield an exponential return when it comes to Bitcoin.

I do know this sounds obscure, however don’t fear. I’ll attempt to break it down.

Irrespective of the bitcoin value, every contract is value a specific amount of US {dollars}. This implies if the contract is ready to symbolize $1, the worth in US {dollars} doesn’t change with the Bitcoin value. You already know precisely what number of {dollars} every contract represents.

Now, as a result of every contract is value a hard and fast quantity of US {dollars}, the quantity of Bitcoin you acquire or lose from every contract modifications as the value of Bitcoin modifications. That is the “exponential” facet.

For instance, if the value of Bitcoin goes up, the identical contract will symbolize much less Bitcoin as a result of every Bitcoin is value extra {dollars}. Conversely, if the Bitcoin value falls, that very same contract will symbolize extra Bitcoin as a result of every Bitcoin is value fewer {dollars}.

So, in regards to the exponential half, to make clear as soon as once more. It doesn’t imply you’re getting an exponential return enhance in a strict mathematical sense. As an alternative, it refers to the truth that your Bitcoin returns might considerably enhance if the Bitcoin value falls, simply as they may lower if the Bitcoin value will increase.

So, extra returns in Bitcoin as the value falls, however much less Bitcoin returns if the value goes up? Why would somebody need that?

Merchants use these contracts to amplify their publicity to Bitcoin value actions. When the value of Bitcoin falls, if you happen to’re holding a brief place, the worth of your place when it comes to Bitcoin will increase as a result of every Bitcoin is now value fewer US {dollars}.

This implies you should purchase again the contract at a decrease Bitcoin value, which might offer you extra Bitcoin per greenback whenever you shut your place. Conversely, if the value will increase, your Bitcoin worth decreases, however if you happen to’re in a protracted place, you’ll revenue.

Instance for clarification

Inverse futures contracts have a non-linear nature. Once we go lengthy on the XBTUSD Perpetual contract inverse futures contract, we’re primarily shorting USD. It is because the contract is inverse, which signifies that as BTC will increase in worth relative to the greenback, the value of our place in BTC decreases.

Earlier than

After

Please test the values and mark costs of future contracts. You’ll discover that the value of BTC has elevated whereas the contract measurement, which is value $1, has remained fixed. Nonetheless, the worth of my lengthy place in XBT has decreased.

The income from holding BTC in your pockets give fewer beneficial properties in BTC as the worth of BTC appreciates; nonetheless, the income in USD are magnified.

Some buyers, companies, and establishments would possibly maintain Bitcoin and need to defend towards the BTC value declines. Through the use of inverse futures contracts, they will “lock in” the present greenback worth of their Bitcoin holdings.

If Bitcoin’s value drops, the rise in Bitcoin returns from these contracts can offset the loss in worth of their precise Bitcoin holdings. Whereas they won’t profit from an increase in Bitcoin’s value, they gained’t endure a decline. In sensible phrases, in case your BTC is deposited on BitMEX, you should utilize the inverse future contract and use 1x leverage brief to “lock in” the greenback worth.

There’s a purpose why BitMEX calls dubbed their inverse futures contracts BitMEX hedging XBU collection.

Here’s a record with the inverse futures contract listed on BitMEX.

If you wish to signup to BitMEX and desire a 10% low cost. You should utilize my referral hyperlink: https://www.bitmex.com/app/register/vhT2qm

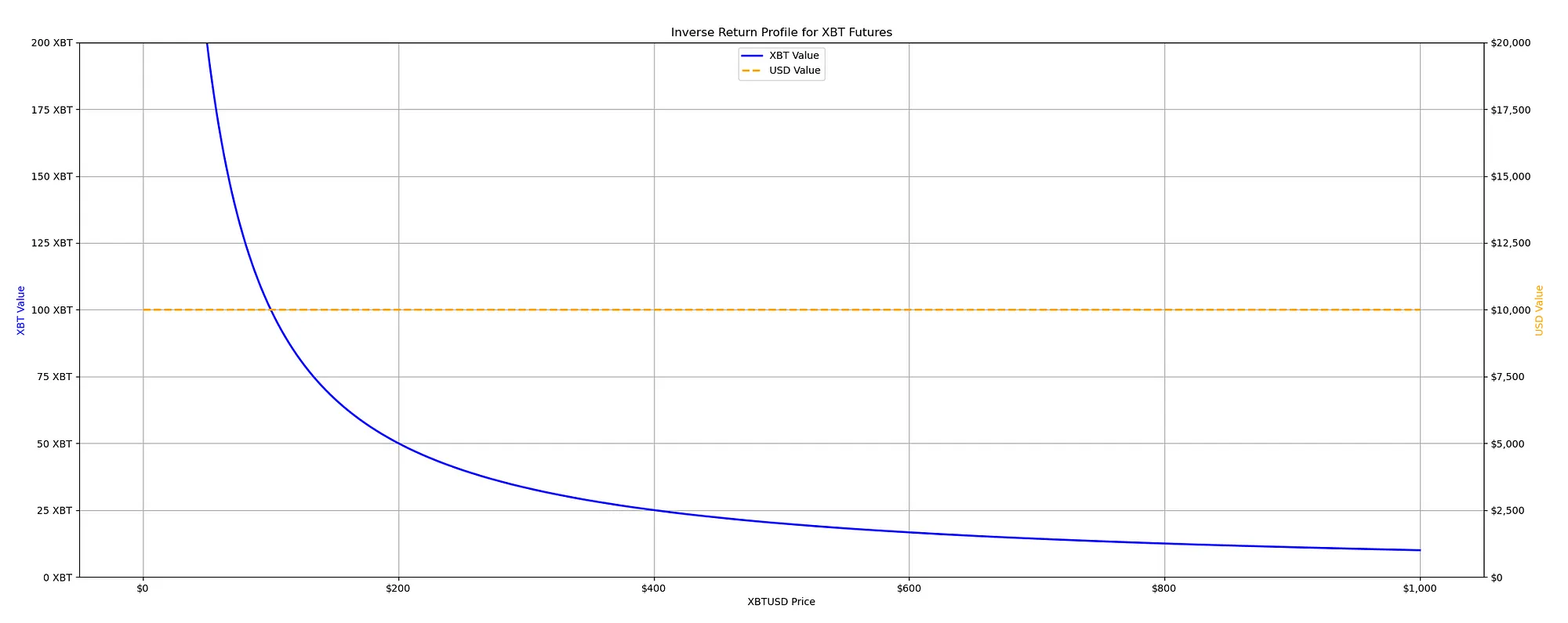

What does BitMEX XBTUSD Inverse Futures Return Profile Look Like?

As talked about earlier, an “ inverse “ contract is a unique form of contract. Although it nonetheless offers with BTC/USD, its workings are flipped. As an alternative of your contact’s worth being mounted in Bitcoin, it’s mounted in {dollars}. If the value of Bitcoin goes up, the identical contract will symbolize much less Bitcoin as a result of every Bitcoin is value extra {dollars}. Conversely, if the Bitcoin value falls, that very same contract will symbolize extra Bitcoin as a result of every Bitcoin is value fewer {dollars}.

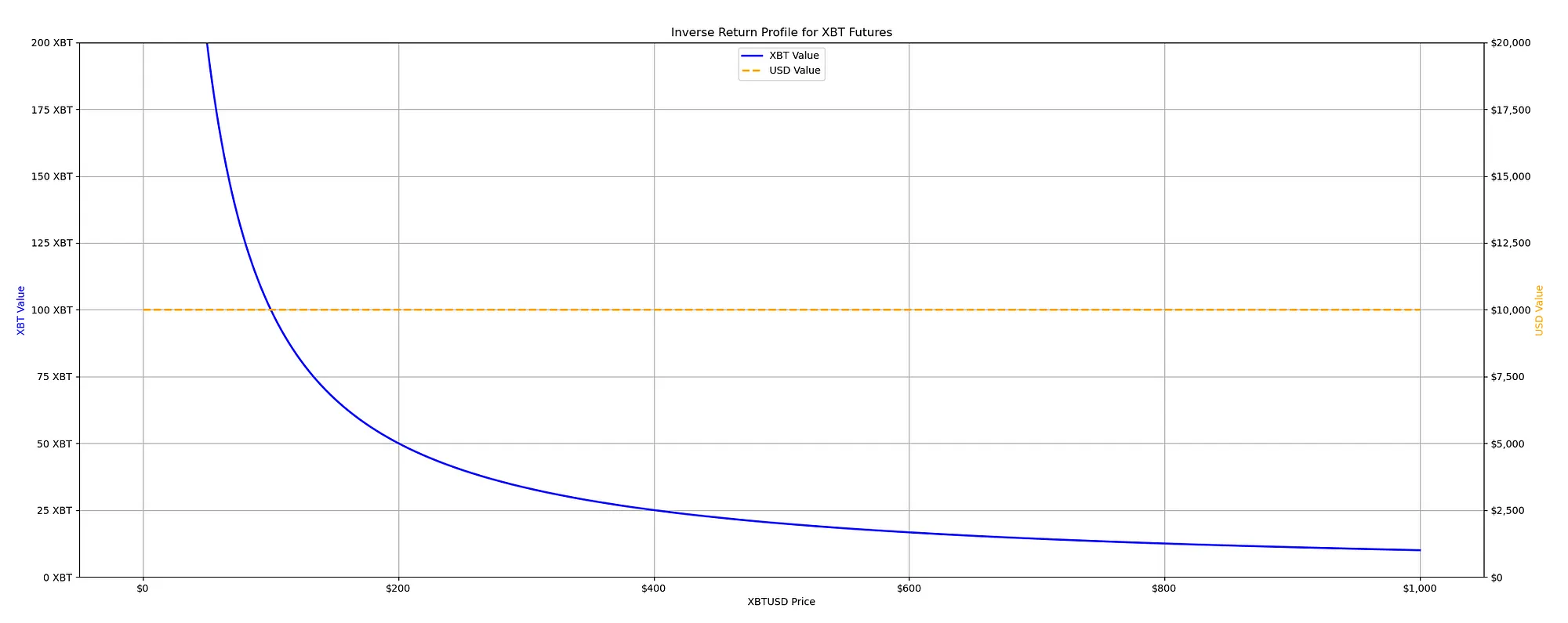

Now, you might marvel what that return profile appears to be like like. Right here is the XBTUSD perpetual contract specification. We see that the USD contract worth is 1 USD.

In comparison with different cryptocurrency inverse contracts, such ETH inverse can have various values in USD.

To offer ample illustration and guarantee an intensive understanding, let’s contemplate a hypothetical situation the place the worth of 1 contract is equal to $100.

If we’ve got 100 futures contracts, every value $100, the full worth of our contracts in {dollars} is at all times $10,000, no matter Bitcoin’s value.

As a result of they’re inverse contracts, when the value of Bitcoin goes down, the quantity of BTC that every of our contracts is value goes up. You already know, as a result of we might purchase extra BTC in {dollars} if the value of BTC is decrease. Then again, if the value of Bitcoin goes up, the quantity of BTC you get per contract goes down. That is why we are saying the Bitcoin worth is ‘exponential’ or follows a ‘1 over x’ sample, as proven by the asymptotic curve within the graph.

Supply code for the python script to generate this graph: https://github.com/romanornr/bitmex_pnl_model/tree/main/inverse_futures

As Bitcoin’s value falls, the horizontal axis will get nearer and nearer to it however by no means really touches out. Within the best-case situation, our potential revenue is which you could solely double your cash or get a 100% return on these inverse contracts if you happen to go lengthy.

Nonetheless, if the value of Bitcoin goes down, the graph reveals that the Bitcoin worth of our contracts might enhance with out a restrict. It is because, mathematically, as you divide by a smaller and smaller quantity (the value of Bitcoin, which is getting decrease), the outcomes get bigger and bigger.

BitMEX Quanto Futures vs. Inverse Futures

Let’s determine what is healthier fitted to what kind of dealer.

Quanto futures contracts on BitMEX enchantment to merchants with a bullish view or those that need to speculate in Bitcoin as a substitute of the greenback. What makes Quanto Futures distinctive is its skill to take a position on a spread of belongings equivalent to Ethereum, Hyperlink, Avax, Solana, Aptos, SUI, and Dogecoin and their value actions towards USDT with margins posted in BTC.

The settlement of those contracts is in Bitcoin (XBT), not the USDT or the underlying asset (ETH, LINK, SOL, APT, SUI). This design permits merchants to take a position on the value actions of underlying belongings in USDT whereas holding solely Bitcoin.

One other benefit of Quanto futures contracts for bullish speculators is that they sometimes commerce at a premium (contango), particularly when the market sentiment is bullish, and supply a better return.

Then again, inverse futures contracts are designed for ‘bearish merchants’ who need to hedge the worth of BTC towards the U.S. greenback. These contracts work inversely to conventional linear futures; as the value of BTC calls will increase, the contract’s worth in USD will increase, permitting merchants to revenue from downward market actions.

Reminder: When buying and selling Linear futures contracts, you should deposit USDT as collateral, and your margin and PNL will even be in USDT. To be able to commerce linear futures on BitMEX, you’re required to deposit USDT.

For buyers holding BTC however involved a few potential fall in its value, inverse futures contracts are a sexy hedging software. By getting into into an inverse futures contract, merchants can lock in a value for Bitcoin and defend themselves towards value declines. It’s a fantastic software to learn about, particularly because the market tends to be unstable.

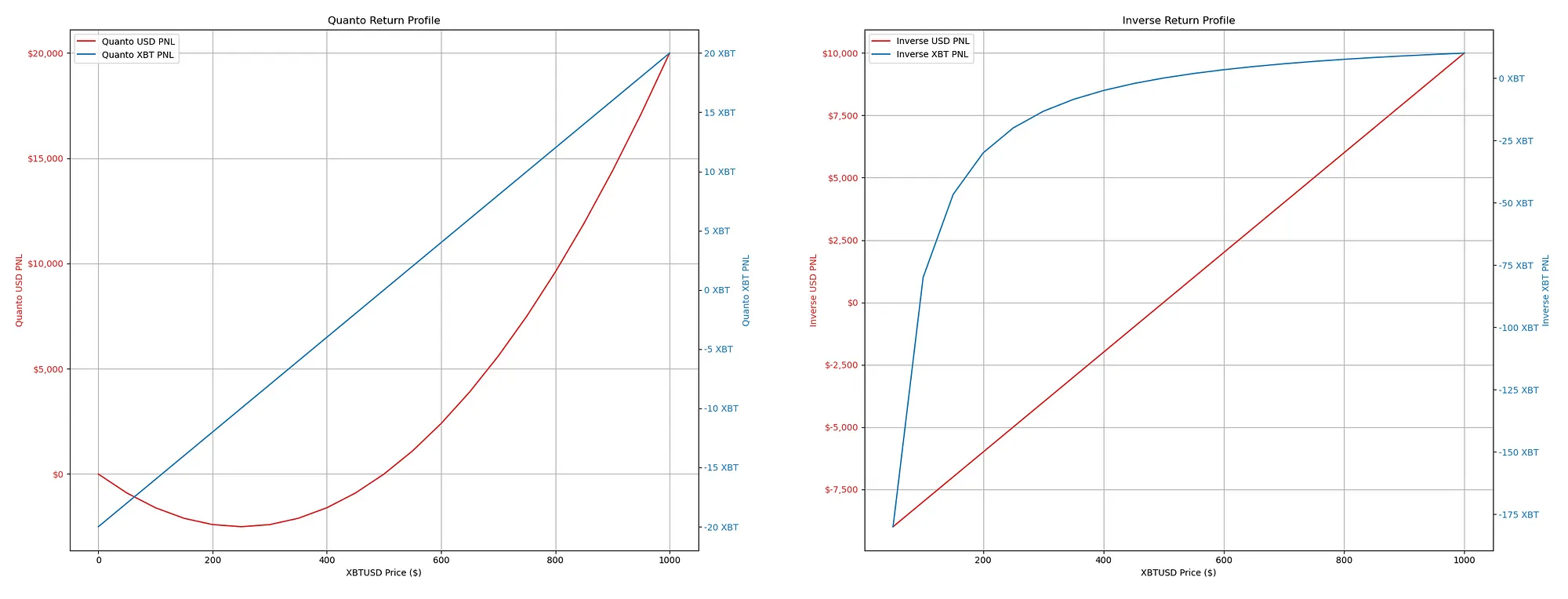

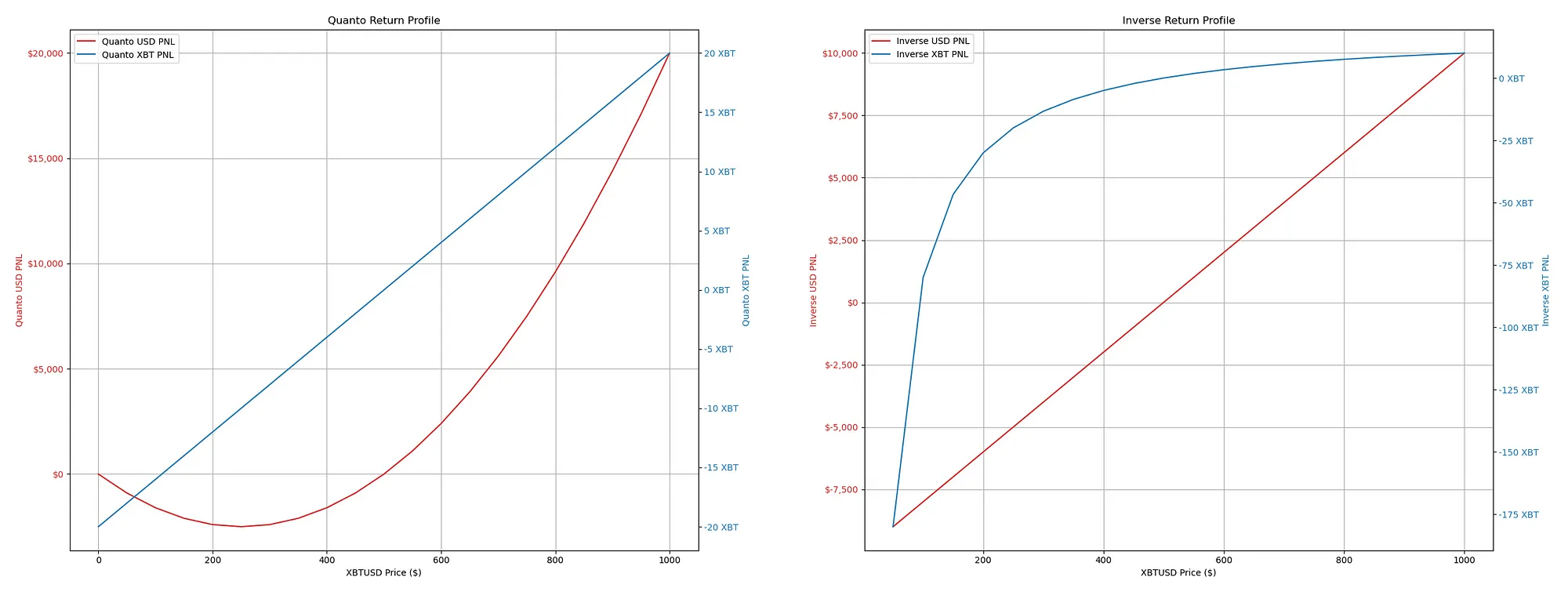

Now let’s contemplate a situation through which the value of Bitcoin in US {dollars} is ready at $500. We’re working with BitMEX quanto futures and inverse futures, which depict the return profiles of holding 4000 contracts with an preliminary entry value of $500.

For each contract sorts, we see the PNL in Bitcoin and US greenback phrases over a spread of Bitcoin costs from $0 to $1000. The Revenue and Loss (PNL) for each sorts of contracts is visually illustrated when it comes to Bitcoin and US greenback.

Supply code to generate this PNL graph: https://github.com/romanornr/bitmex_pnl_model/tree/main/quanto_vs_inverse

Quanto Futures Return Profile

- We’re on the entry level at a bitcoin value of $500, so the PNL for each USD and XBT is round zero.

- As Bitcoin’s value goes above the entry value of $500, the Quanto USD PNL (pink line) will increase, which happens at an accelerating price. Which means because the Bitcoin value retains rising, the income in USD phrases turn into more and more bigger. By holding a quanto futures place, you may make extra income in USD because the Bitcoin value will increase and the revenue development price additionally accelerates. It is because quanto futures use a payoff construction that multiplies the Bitcoin value will increase.

- When the value of Bitcoin drops under the entry value, the US greenback revenue and loss (PNL) additionally decreases. Nonetheless, the lower in PNL turns into much less steep and even flattens because the Bitcoin value approaches zero. It’s necessary to notice that losses can happen when the Bitcoin value falls under the entry value, however they might lower slower than beneficial properties when the value goes up. In different phrases, losses in USD phrases usually are not as delicate to the value of Bitcoin falling because the beneficial properties are when the Bitcoin value rises.

The convex return profile in USD PNL for the quanto futures reveals that the contract may be structured in order that the PNL, in USD phrases, advantages from a rising Bitcoin value relative to losses from a falling Bitcoin value.

The asymmetry of Bitcoin futures appeals to merchants who need to make the most of the cryptocurrency’s potential for beneficial properties whereas minimizing their publicity to USD losses. Nonetheless, it’s necessary to notice that losses usually are not solely eradicated, and Quanto futures could commerce at a premium.

Inverse Futures Return Profile

- The inverse USD PNL reveals a linear relationship with the value of Bitcoin. For each greenback change within the value of bitcoin, the revenue or loss in USD phrases modifications by a continuing quantity.

- As the value of Bitcoin will increase from an entry value of $500, the USD PNL falls linearly.

- The XBT PNL reveals a non-linear relationship with the value of Bitcoin. When the value rises above the entry value, the PNL in Bitcoin will increase; every contract represents a smaller quantity of Bitcoin because the payout is in USD, and every USD buys much less BTC as the value rises). The revenue in Bitcoin phrases grows, however every extra greenback represents a smaller fraction of Bitcoin.

- When the value of Bitcoin drops under $500, the losses are accelerated as a result of the reducing value signifies that every misplaced greenback represents a higher quantity of Bitcoin.

- The PNL in Bitcoin (blue line) has a non-linear relationship with the value of Bitcoin. It will increase with the value of Bitcoin however at a reducing price, suggesting a type of hedging by lowering publicity in Bitcoin phrases as the value of Bitcoin will increase.

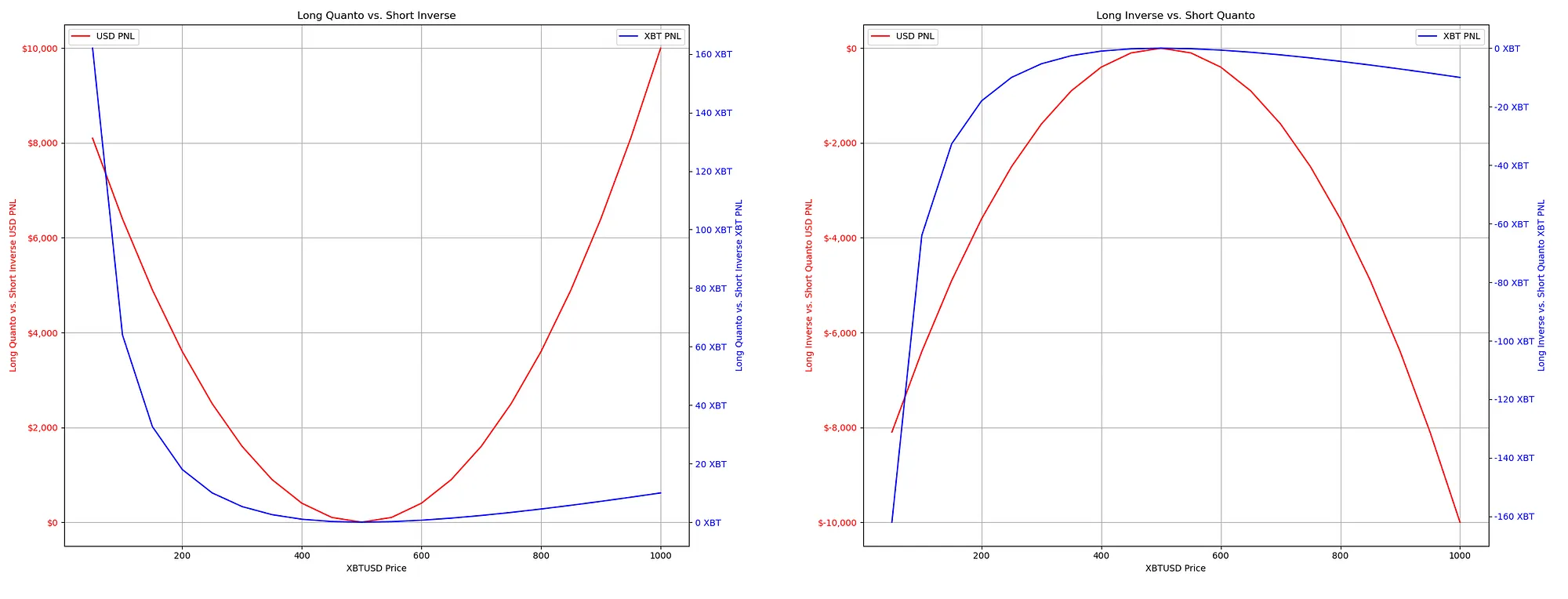

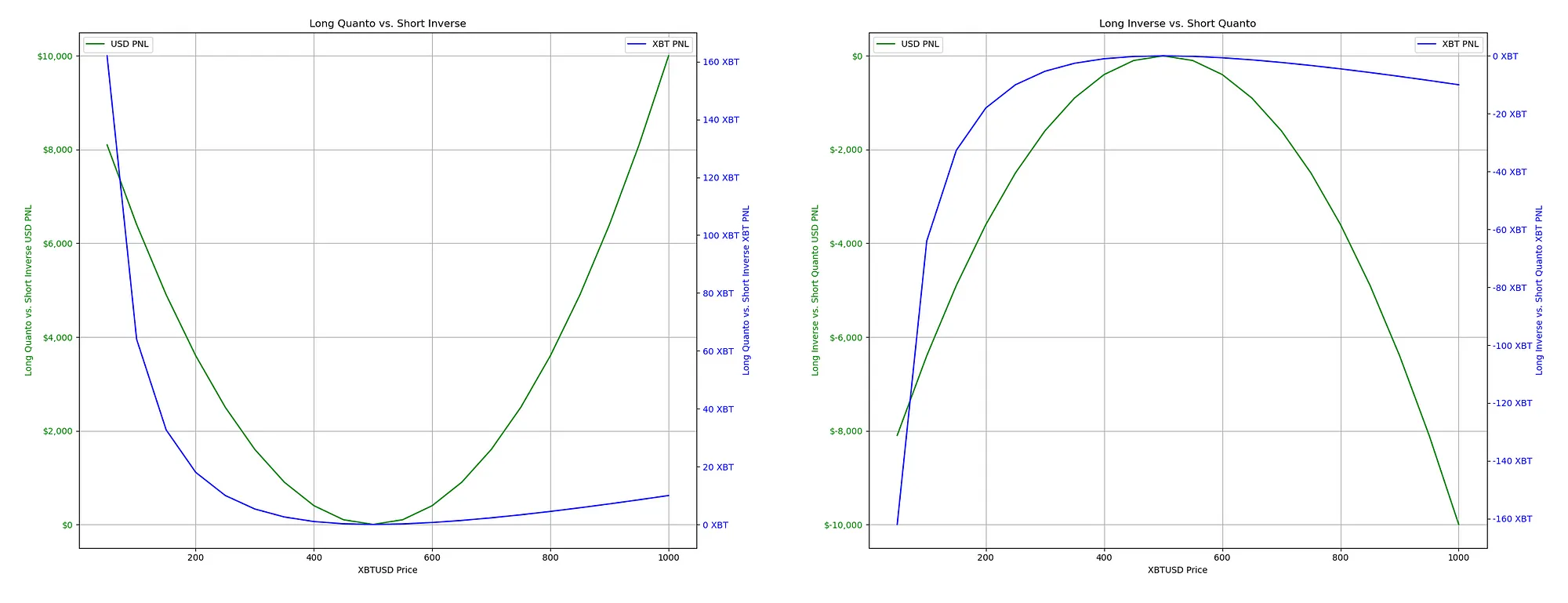

Lengthy Quanto vs. Brief Inverse Postion

Let’s make two bets on the value of Bitcoin with completely different payouts relying on the course of the value motion. Our evaluation will contemplate Bitcoin’s value vary from $0 to $1000.

We have an interest within the Quanto future, a kind of wager that permits us to earn extra U.S. {dollars} if the underlying asset’s value, bitcoin (BTC), will increase. The payout of a quanto contract is predicated on the share change within the asset’s value however calculated in one other forex, on this case, the greenback. Due to this fact, as the value of Bitcoin goes up, the potential income in USD additionally enhance at an accelerating price.

Then again, a ‘Brief inverse’ place is actually a wager towards the value. On this place, we earn a revenue if the value falls, however we use the ‘inverse future contract’ to convey that wager to life. The revenue or loss (P&L) for this technique is mirrored in Bitcoin. As the value of Bitcoin will increase, the contract loses worth quickly on account of its ‘inverse’ nature, as defined earlier. The ‘inverse futures contract’ payout construction is a perform of the reciprocal of the asset value. Nonetheless, since we’re brief, we acquire extra USD as the value of Bitcoin drops.

Supply code to generate this graph: https://github.com/romanornr/bitmex_pnl_model/tree/main/quanto-inverse-combination

When these two positions work collectively, they create a dual-benefit situation. If the value of Bitcoin will increase, our lengthy quanto place ought to yield a squared return in {dollars} because of the magnifying impact of the quanto futures contract. Then again, if the value falls, our brief inverse place must be worthwhile, as it’s designed to hedge and profit from a falling market.

This strategy takes benefit of volatility, permitting us to revenue whether or not the value skyrockets or nosedives with out precisely predicting its course however the magnitude of the course.

This will likely remind you of a protracted straddle 😉 // TODO Wants context

It is advisable know the way the Bitcoin worth of your contracts modifications with the change in value as a result of BitMEX margins their futures contracts in Bitcoin. If you’re buying and selling with a protracted Quanto and brief inverse mixture, the inverse futures are the contracts that may enhance of their Bitcoin-denominated worth when the greenback value of Bitcoin falls. The Bitcoin-denominated worth falls when the value rises.

Attributable to these fluctuations, It’s attainable that you could be have to deposit additional Bitcoin into your margin account at occasions on account of fluctuations out there. This additional margin is critical to fulfill the upkeep necessities and guarantee which you could uphold your trades regardless of important value swings. You will need to stay vigilant of market modifications to handle your margins successfully and keep away from liquidation.

Right here’s an inventory of Quanto futures buying and selling on BitMEX: https://www.bitmex.com/app/contractList#Quanto-Futures

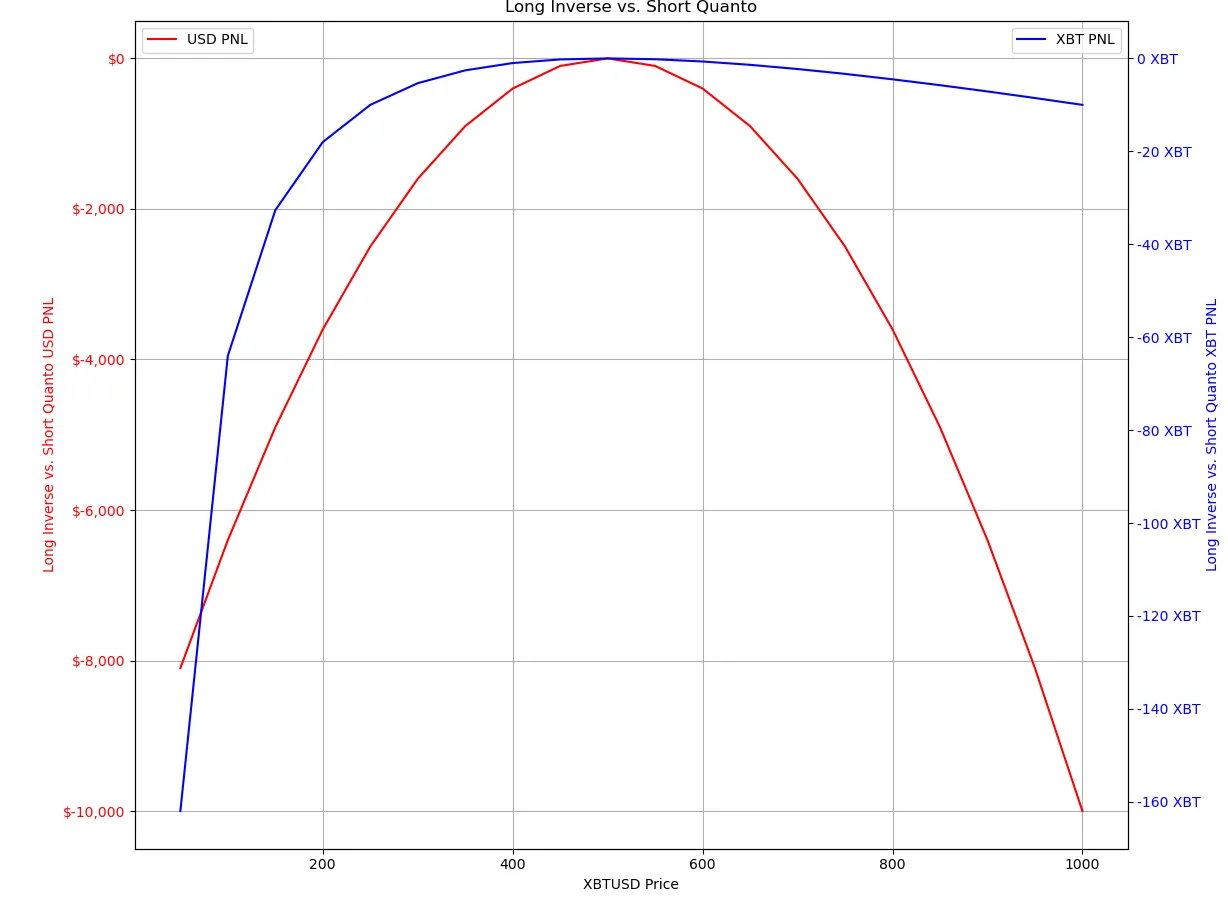

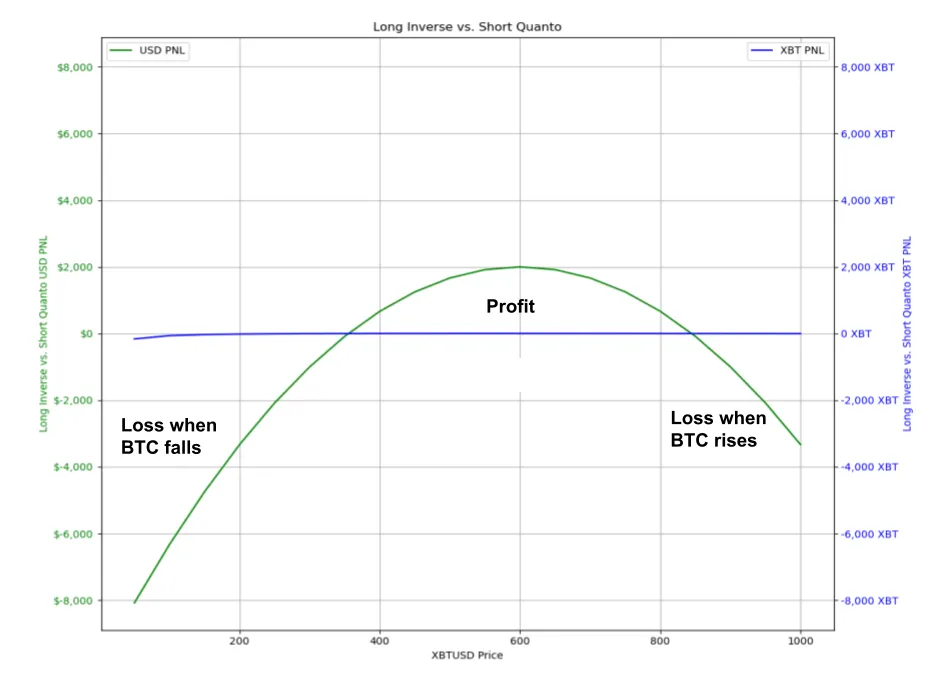

Lengthy Inverse and Brief Quanto Mixture Place

Now let’s take a look at the alternative; let’s make two bets on the value of Bitcoin. We lengthy the “inverse futures contract” and “brief quanto contract.” Our evaluation will contemplate Bitcoin’s value vary from $0 to $1000.

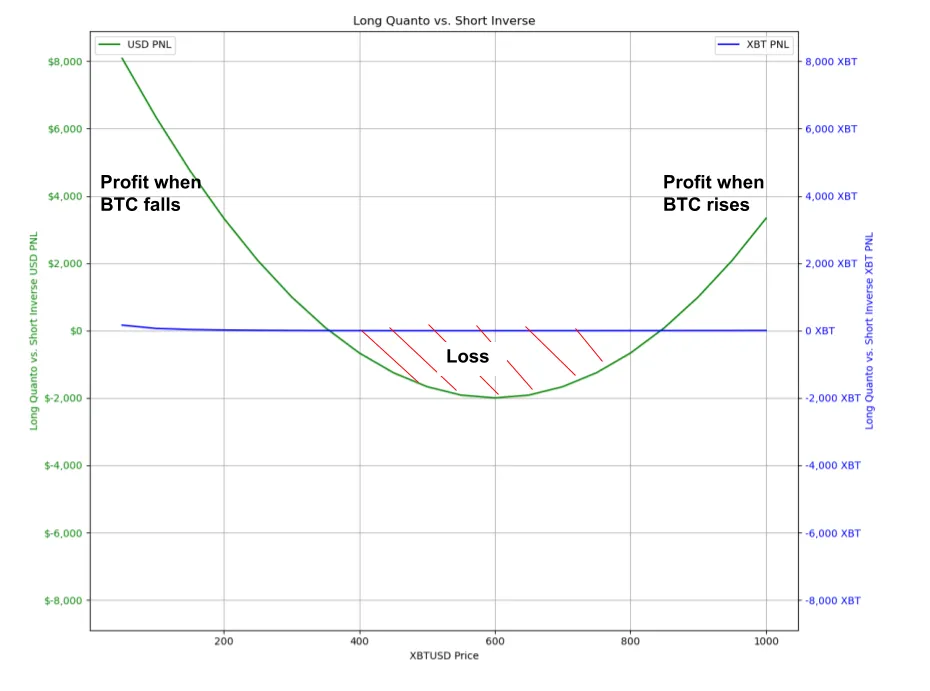

Within the “lengthy inverse and brief quanto situation,” the graph presents a mirrored parabola, indicating that our P&L final result is predominantly adverse no matter whether or not the Bitcoin value goes up or down.

Only a heads up, the parabolic impact of each “lengthy quanto & brief inverse” and “lengthy inverse & brief inverse” is corresponding to “gamma” in choices buying and selling and “convexity” in bond buying and selling. To study extra about gamma, learn this article by Romano RNR.

Gamma refers back to the price of change within the delta of an choice, whereas convexity refers back to the sensitivity of a bond’s length to modifications in rates of interest.

Each phrases describe a scenario the place the returns are non-linear, which means that the modifications in value turn into extra important as we transfer towards the extremes.

Within the case of “lengthy inverse & brief quanto,” this non-linear relationship exposes us to elevated threat. If the value strikes drastically in both course, our Revenue and Loss (P&L) can deteriorate rapidly.

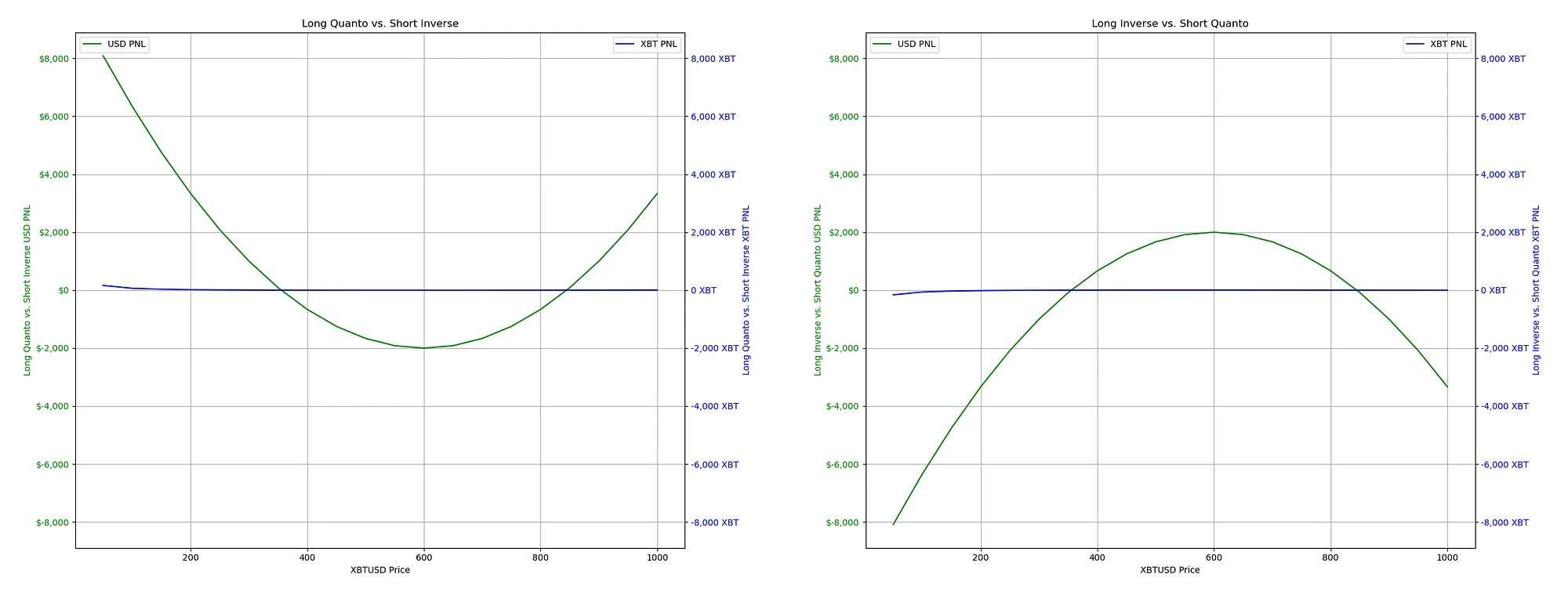

Holding a protracted place in a quanto contract whereas being brief in an inverse contract may be advantageous. Nonetheless, you will need to word that these contracts will not be priced equally or “truthful” always.

Normally, a quanto contract carries a “premium” because of the extra dangers and payoff it presents.

For the aim of our evaluation, let’s assume this premium is $100. This adjustment shifts the P&L graphs, reflecting the premium it prices to enter the lengthy quanto place.

In a “Lengthy Quanto vs. Brief Inverse” setup, we’re getting into a derivatives place delicate to Bitcoin’s value actions and the corresponding influence on the USD payout, which depends upon each the BTC value and its volatility.

Once we take a protracted place in a quanto contract, we expose ourselves to a non-linear payoff profile. Which means our revenue and loss (P&L) just isn’t an easy perform of the Bitcoin (BTC) value, like a linear contract. As an alternative, the impact of the BTC value is squared because of the quanto characteristic. In easier phrases, if the value of BTC strikes considerably in both course, our USD return will enhance exponentially.

Though the improved publicity has advantages, it comes at a value, which is mirrored as a premium over the brief inverse contract. This premium primarily represents the market’s future implied volatility expectations, and the implied volatility is priced into the contract. Once we pay this premium, we’re betting on volatility higher than what the market expects.

If the market experiences extra volatility in comparison with what it expects priced into the quanto premium, the premium we paid for the lengthy quanto place could erode our potential income. This “erosion” is named “time decay” or “theta,” an idea borrowed from choices buying and selling. The place’s worth erodes over time because it approaches the expiration date. To study extra about time decay and theta, learn this article by Romano RNR.

After incorporating the $100 premium, we see the danger zone the place our place is “underwater.” This implies the market value would wish to maneuver considerably in both course for us to interrupt even and canopy the price of the quanto premium. That is much like an “choices premium,” the place you want the market to maneuver sufficient to compensate for the premium you initially paid.

If we had been to take the alternative place, promoting volatility by going “Lengthy inverse and brief quanto,” we’d acquire a premium much like an choice vendor. We might revenue so long as the market stays throughout the vary, however the threat is that if the BTC value strikes past this vary, our losses enhance in a non-linear vogue because of the brief place within the quanto contract.

Is it Higher to At all times Be Lengthy Quanto and Brief Inverse?

It’s not at all times the only option to be lengthy quanto and brief inverse, though it might sound like the higher choice. The choice relies upon closely on the fee related to getting into the commerce, which is the anticipated volatility priced into the quanto premium and your predictions for future market volatility.

It’s mainly an evaluation of the market’s implied volatility (IV) and realized volatility (RV). If you lengthy a quanto contract, you’re shopping for implied volatility. If the market’s future realized volatility finally ends up being decrease than the implied volatility priced into the Quanto contract, then the premium was not value it. It’s like shopping for a ticket for a competition, however the occasion didn’t stay as much as the hype, and the “ticket” was overpriced.

Conversely, if the implied volatility is low relative to the potential excessive realized volatility we count on, and the realized volatility finally ends up being increased than what the market anticipated, then having a “lengthy quanto vs. brief inverse” place may very well be very worthwhile with out a lot directional publicity.

If the quanto premium is just too excessive and we don’t assume that the market will expertise sufficient volatility to justify that premium, then it’s higher to take the alternative place. This implies going “Lengthy Inverse and Brief Quanto,” which has similarities to being the “vendor” of volatility. On this place, we are able to revenue if the volatility seems to be decrease than what the market anticipated. So, if the market doesn’t transfer as a lot because the Quanto premium, we are able to nonetheless make a revenue.

Understanding market sentiment, by-product pricing, and threat administration is essential to buying and selling with historic and implied volatility evaluation.

If you wish to signup to BitMEX and desire a 10% low cost. You should utilize my referral hyperlink: https://www.bitmex.com/app/register/vhT2qm

What’s the Level of All of This?

In October/November 2020, I stumbled upon an outdated article about BitMEX. It talked about the time period “convexity,” which piqued my curiosity. That very same day, I started researching extra in regards to the matter through the use of Google to seek out extra info.

Possibly you’re not concerned about Bitcoin buying and selling, however reasonably altcoins. In that case, you’ll love buying and selling on BitMEX. Stick to me until the top for extra details about making use of every little thing you’ve realized to commerce altcoins and supercharge your P&L

Learn the article on convexity by Arthur Hayes here.

On that very same day, I realized about choices buying and selling and phrases equivalent to “convexity squeeze” and “gamma squeeze.” Earlier than the Gamestop gamma squeeze, a gamma squeeze was occurring in Tesla, which I attempted to ‘examine.’

The phrase “convexity” modified every little thing for me since. It was most likely probably the most pivotal second.

So about these contracts and their complexity. Convexity, also called “Gamma,” measures how sensitively a by-product’s worth modifications as the value of the underlying asset modifications.

It’s just like the acceleration of a automobile; it’s not nearly how briskly you’re going (just like the delta, also called the primary by-product) however how rapidly that pace is growing.

Convexity can amplify your portfolio beneficial properties. You can also make bigger income if the market swings in your favor past what you accounted for by the first-order value motion, which is the delta.

Nonetheless, if you happen to don’t perceive convexity and the way it impacts the derivatives you’re buying and selling, you gained’t be capable of account for the way quickly your place’s worth can change, and also you threat repeatedly being financially destroyed.

When not understood or mismanaged, your losses will compound non-linearly.

So, the BitMEX XBTUSD perpetual swap has at all times been an “inverse futures contract,” and lots of have traded that previously. Do you know that? It’s a shocker for some.

The identical goes for Deribit. These had been at all times “inverse futures contracts” and lots of contracts on OkEx.

What did we find out about inverse futures contracts once more?

- Inverse futures are contracts that enhance of their Bitcoin-denominated worth when the greenback value of Bitcoin falls, and the Bitcoin-denominated worth falls when the value rises.

- That is why we are saying the Bitcoin worth is ‘exponential’ or follows a ‘1 over x’ sample, as proven by the asymptotic curve within the graph.

- Inverse futures contracts are designed for ‘bearish merchants’ who need to hedge the worth of BTC towards the U.S. greenback. These contracts work inversely to conventional linear futures; as the value of BTC calls will increase, the contract’s worth in USD will increase, permitting merchants to revenue from downward market actions.

- If you lengthy an “inverse futures contract”, the losses are accelerated as a result of the reducing value signifies that every misplaced greenback represents a higher quantity of Bitcoin.

Sure, the XBTUSD perpetual swap has at all times been an “inverse futures contract,” and lots of have traded that previously to lengthy Bitcoin. Paradoxically, these contracts are meant for hedging, not speculating.

In the event you’re bullish, don’t use the “inverse futures contracts” however the “Quanto futures contracts,” and if that isn’t out there, use the “linear futures contracts.”

BitMEX Linear futures record may be discovered here.

Reminder: When buying and selling Linear futures contracts, you should deposit USDT as collateral, and your margin and PNL will even be in USDT. To be able to commerce linear futures on BitMEX, you’re required to deposit USDT.

If you’re bearish or need to hedge your publicity, use the “inverse futures contracts.”

BitMEX Inverse futures record may be discovered right here: https://www.bitmex.com/app/perpetualContractsGuide#Inverse-Contracts

Linear futures contracts weren’t out there within the early days on account of laws. Buying and selling them exposes you to Tether, which some contemplate dangerous.

As an alternative of promoting BTC, you possibly can deposit it on Bitmex and hedge by shorting XBTUSD with 1x leverage, creating an artificial USD place. By opening a 1x brief place on XBTUSD inverse, you possibly can earn some additional passive earnings because of the funding price if it’s in your favor.

What About Quanto Futures for Altcoin Buying and selling?

If you’re bullish on BTC and altcoins, you possibly can commerce BitMEX Quanto futures for altcoins and amplify your PNL non-linearly. On high of that, your PNL will likely be in BTC, including one other layer of hypothesis.

Now that you’ve got realized about quanto futures contracts, you should utilize this data in sensible situations.

As an example, if you’re holding a protracted place on an altcoin with a quanto futures contract and also you discover that BTC is underperforming whereas the altcoin is bullish, you possibly can maintain your Quanto lengthy place on the altcoin open and use the “inverse future contract XBTUSD” to brief your BTC publicity. This may assist to hedge effectively.

BitMEX Quanto futures record together with altcoins may be discovered here.

Lately, you may as well deposit Ethereum on Bitmex, they usually have an inverse futures contract for Ethereum in case you should hedge: https://www.bitmex.com/app/trade/XBTETH

You possibly can apply what you’ve realized and shorten the inverse futures contract for Ethereum whereas opening a protracted Quanto place on Ethereum. Or, if you happen to consider the Quanto premium is just too excessive and volatility turns decrease than anticipated, you possibly can brief Quanto and lengthy inverse.

You’ll find the Quanto contract for Ethereum here.

I like to recommend utilizing BitMEX Testnet to apply what you’ve realized.

If you wish to signup to BitMEX and desire a 10% low cost. You should utilize my referral hyperlink: https://www.bitmex.com/app/register/vhT2qm

{kind=link}