Carmaker Ford Motor Firm (NYSE: F) has been on a reorganization drive for fairly a while, geared toward higher aligning the enterprise with the quickly altering auto trade. The main target is on revisiting the corporate’s legacy enterprise and streamlining operations via initiatives like management change, rightsizing, and disciplined capital allocation.

Final week, Ford’s shares bounced again from their newest dip however proceed to commerce beneath the long-term common. ‘F’ is a relatively low cost inventory that has skilled vital fluctuations. It gives dividend yield that’s properly above the S&P 500 common. So, the inventory is a favourite amongst revenue traders, particularly after the latest dividend hike.

The Inventory

The weak sentiment surrounding the inventory is unlikely to alter till there’s a significant enchancment within the firm’s gross sales and margin efficiency. Going by the cautious outlook on the enterprise amid manufacturing delays and destructive opinions from a bit of analysts, 2023 would probably be a blended 12 months for the corporate. In the case of proudly owning the inventory, there are usually not many optimistic components to contemplate aside from the low valuation.

In the meantime, the corporate has delivered secure gross sales and earnings efficiency after returning to profitability from the virus-induced losses greater than two years in the past. Additionally, it ended fiscal 2022 with a free money movement of $9.1 billion, which got here as a shock to many. Nevertheless, the administration’s steering factors to a decline in free money movement this 12 months, a prediction that doesn’t bode properly for the corporate’s capital allocation plan.

Roadblock?

Of late, Ford has been dealing with issues with its electrical car enterprise, and the corporate was compelled to slash 1000’s of jobs. Not too long ago, it needed to halt manufacturing of the F-150 Lightning pickup — a mannequin well-received by clients after the launch — as a result of battery-related points. It has come as a setback to “Ford+”, a plan laid down by the corporate with the purpose of changing into a frontrunner in digital electrical autos. The administration is bullish on the Ford Blue used-vehicle program and Ford Professional, a set of enterprise productiveness instruments designed for complete fleet administration.

“Ford’s a special firm at the moment, we’re all constructing a stronger customer-focused enterprise that generates sustainable, worthwhile progress and returns above the price of capital. Whereas our 2022 outcomes fell in need of my expectations, I’ve by no means been extra enthusiastic about our future, as a result of we have now the precise plan, the precise construction to succeed, the perfect group on the sphere, and actual strategic readability. This 12 months is about execution. It’s time for us to ship and we’ll with relentless consideration to our founding rules, drift, and progress, and we’re hitting the bottom operating,” mentioned CEO James Farley on the This autumn earnings name.

Key Numbers

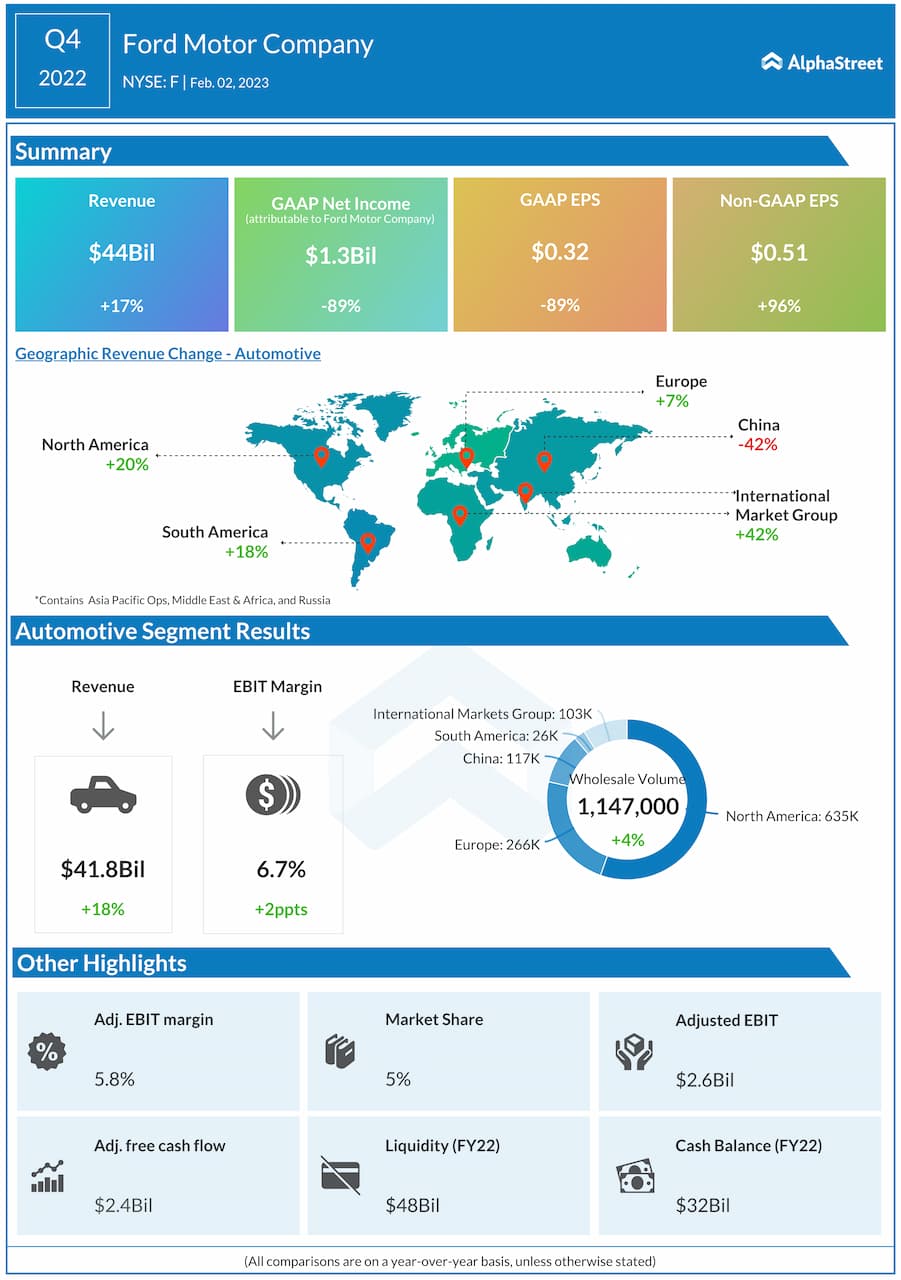

Within the last three months of fiscal 2022, gross sales elevated in all geographical segments besides China the place the financial system is experiencing a slowdown as a result of resurgence of COVID-19 instances. Whole revenues climbed 17% from final 12 months to $44 billion, which is broadly according to the market’s projection. Consequently, adjusted earnings practically doubled to $0.51 per share however fell in need of expectation, marking the second consecutive miss after beating persistently for a number of quarters. The corporate expects adjusted free money movement to be $6 billion and capital expenditures between $8 billion and $9 billion in fiscal 2023.

After a weak begin to the session, Ford’s shares picked up momentum and traded increased on Friday afternoon. It’s down 25% from twelve months in the past.

{kind=link}