6381380

A Fast Take On NCS Multistage

NCS Multistage Holdings (NASDAQ:NCSM) supplies oil & fuel effectively website fracturing and associated techniques and companies in the USA, Canada and abroad.

NCSM has grown income because the {industry} rebounds from the pandemic’s demand drop.

My outlook on NCSM is a Maintain.

NCS Overview

Houston, Texas-based NCS Multistage was based in 2006 to offer engineered merchandise for onshore hydraulic fracturing techniques extracting oil & fuel hydrocarbons from unconventional formations within the U.S. and elsewhere.

The agency is headed by Chief Govt Officer Ryan Hummer, who has been with the agency since 2014 and was beforehand a Director at Lazard and an Affiliate at Credit score Suisse.

The corporate’s main options embrace the next:

Fracturing techniques

Nicely building

Tracer Diagnostics

Enhanced restoration

Repeat precision

The agency acquires clients by its in-house direct gross sales, advertising and enterprise growth efforts and thru referrals.

NCS Multistage’s Market & Competitors

In line with a 2022 market research report by Verified Market Analysis, the worldwide marketplace for hydraulic fracturing (as a proxy for the fracturing tools market) was estimated at $33.8 billion in 2021 and is forecast to achieve $61.3 billion by 2030.

This represents a forecast CAGR of 6.6% from 2023 to 2030.

The primary drivers for this anticipated development are a shift in exploration exercise towards ‘growing unconventional property together with shale, tight fuel, tight oil, and coal mattress methane.’

Nonetheless, public issues in regards to the environmental uncomfortable side effects of fracking embrace water utilization, seismic exercise and water contamination, to call a couple of.

The agency faces a wide range of rivals in a fragmented {industry}.

NCS’s Current Monetary Tendencies

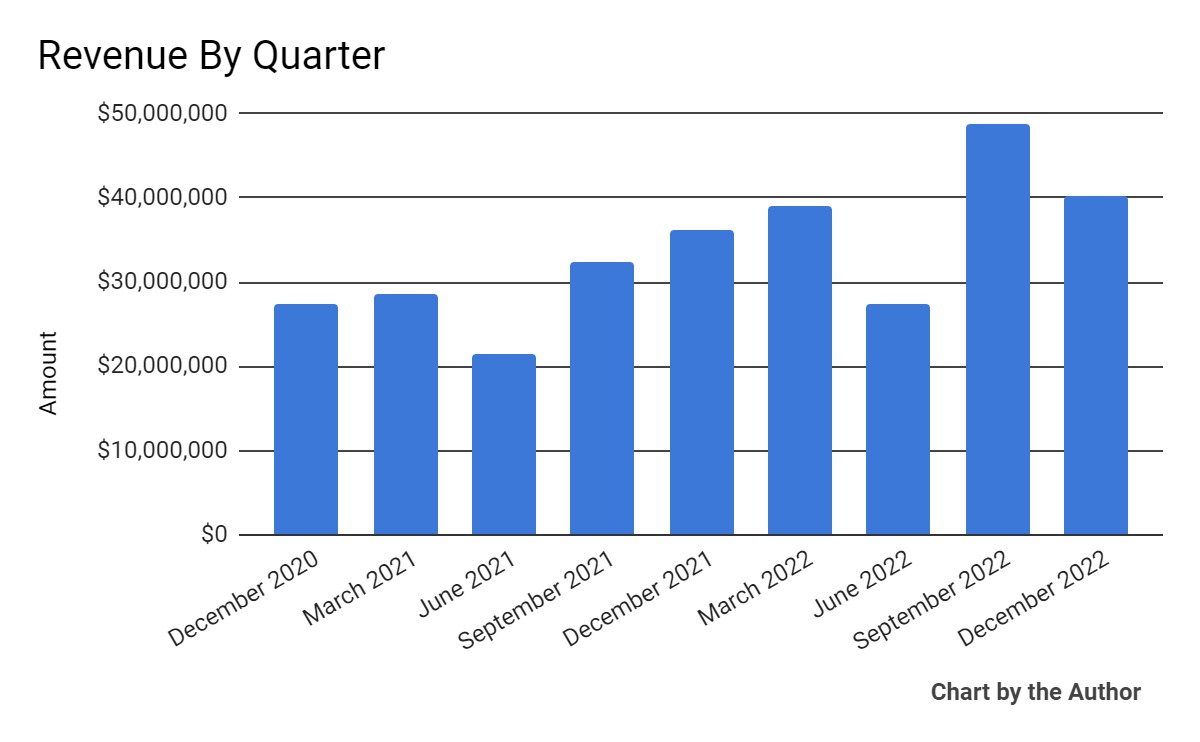

Whole income by quarter has trended larger per the next chart:

Whole Income Historical past (In search of Alpha)

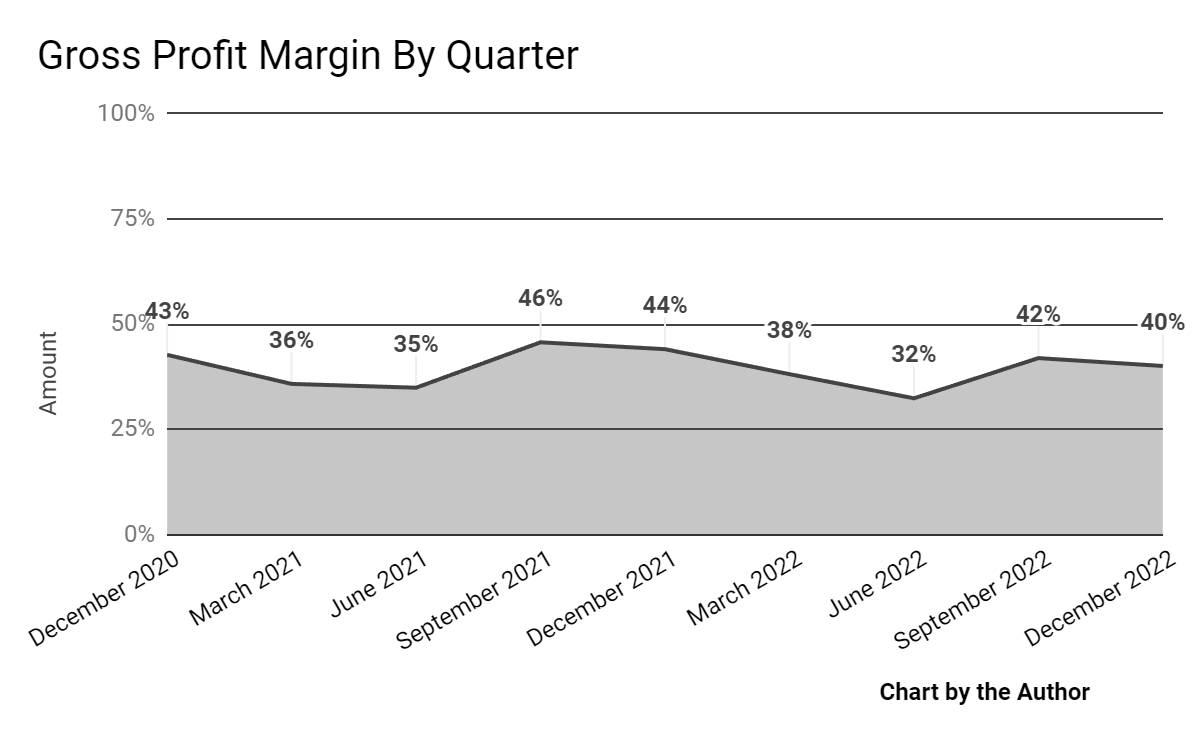

Gross revenue margin by quarter has been trending decrease in latest quarters:

Gross Revenue Margin Historical past (In search of Alpha)

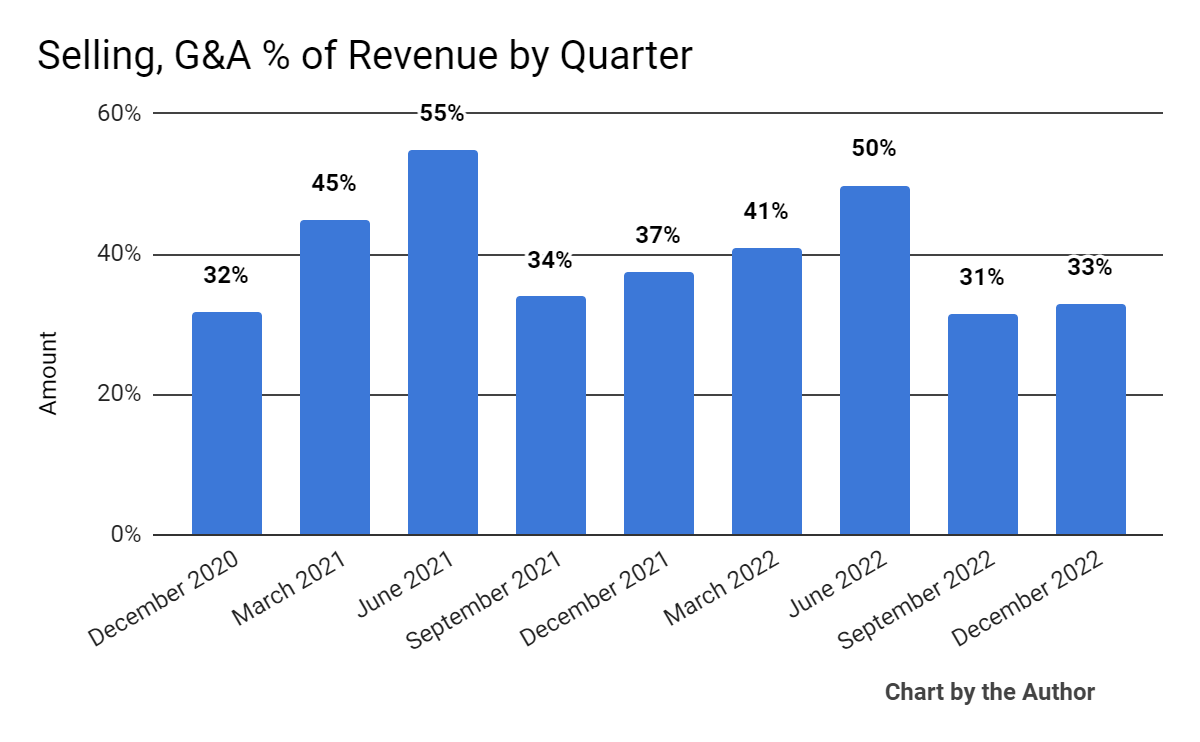

SG&A bills as a share of whole income by quarter have been transferring decrease in latest quarters, a constructive signal of accelerating effectivity:

Promoting, G&A % Of Income Historical past (In search of Alpha)

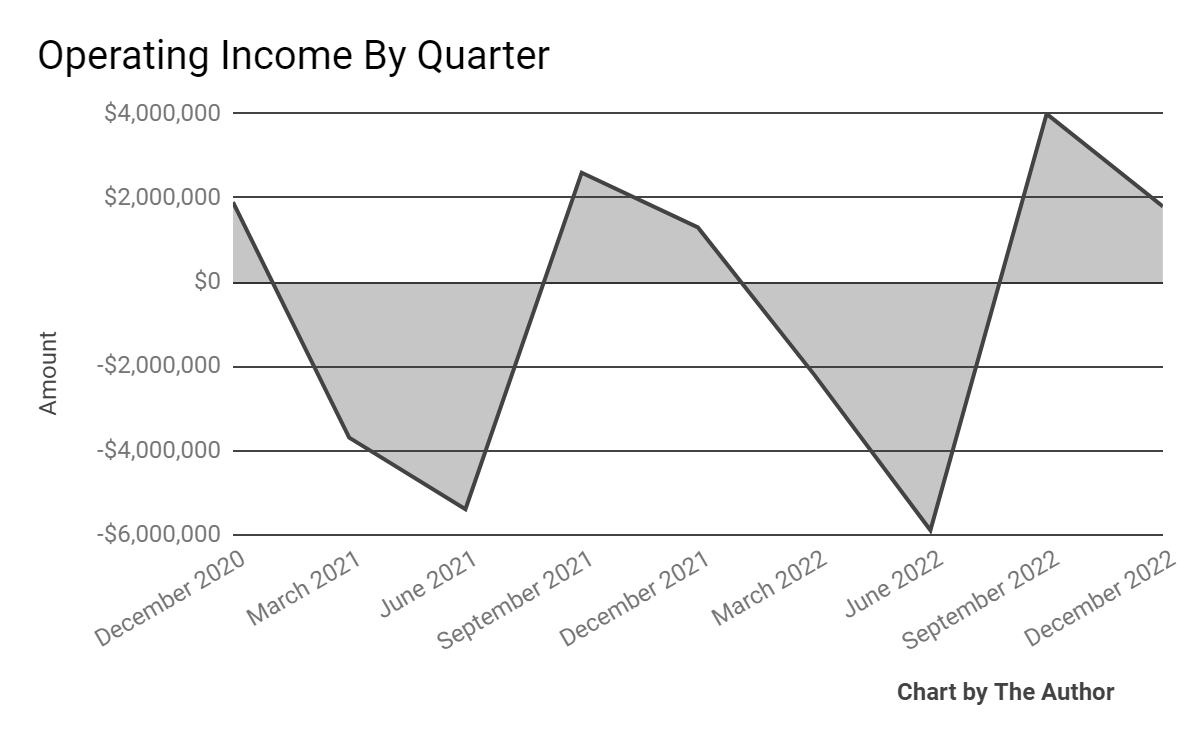

Working revenue by quarter has been trending barely larger in quarterly cycles:

Working Earnings Historical past (In search of Alpha)

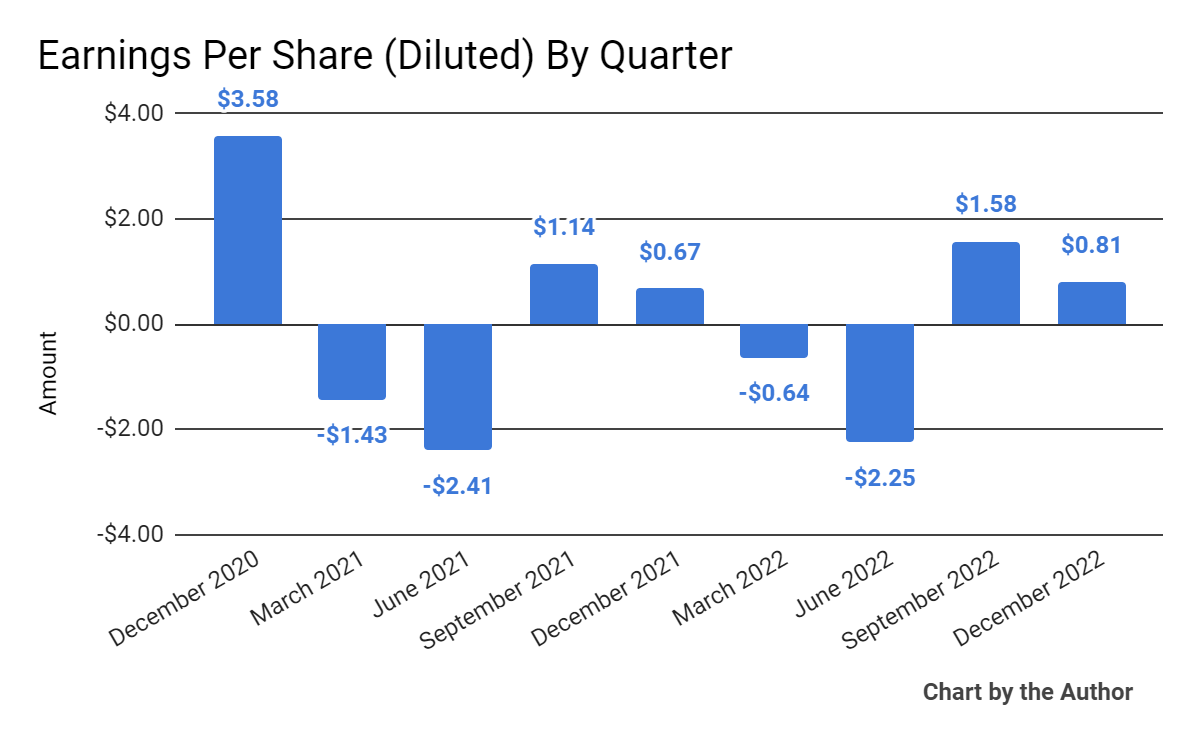

Earnings per share (Diluted) have diversified in keeping with the next chart:

Earnings Per Share Historical past (In search of Alpha)

(All knowledge within the above charts is GAAP)

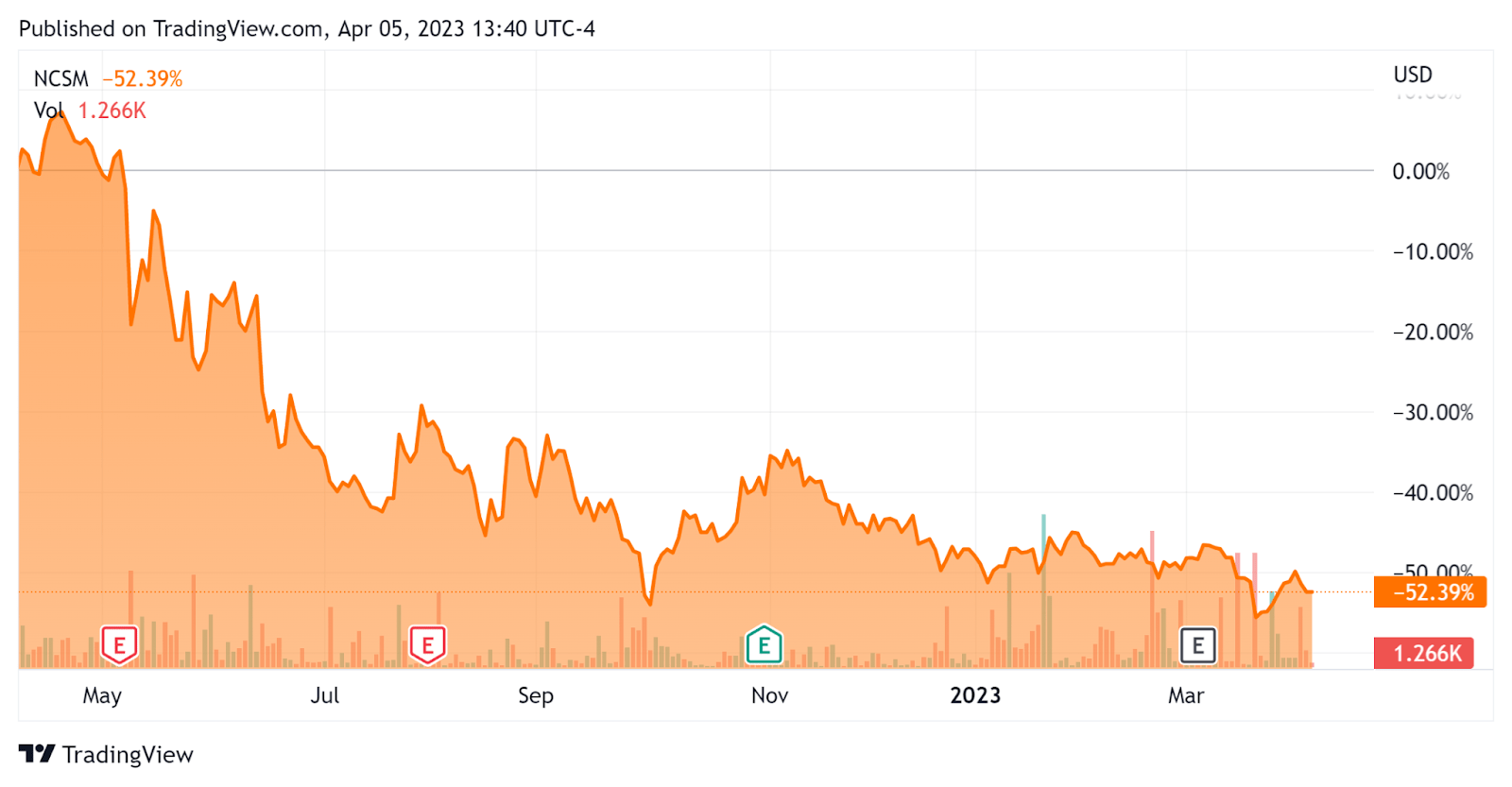

Prior to now 12 months, NCSM’s inventory value has dropped 52.4%, because the chart signifies under:

52-Week Inventory Worth Chart (In search of Alpha)

As to its This fall 2022 monetary outcomes, whole income rose 11.4% year-over-year however gross revenue margin dropped 4.4 share factors as a result of inflationary pressures on components and labor.

SG&A bills as a share of whole income have been trending decrease and working revenue has been working its means larger in successive four-quarter cycles.

For the steadiness sheet, the agency completed the quarter with money and equivalents of $16.2 million and no debt.

Over the trailing twelve months, free money used was $2.4 million, of which capital expenditures accounted for $1.0 million. The corporate paid a hefty $6.0 million in stock-based compensation within the final 4 quarters.

Valuation And Different Metrics For NCS

Beneath is a desk of related capitalization and valuation figures for the corporate:

Measure [TTM] | Quantity |

Enterprise Worth / Gross sales | 0.5 |

Enterprise Worth / EBITDA | 33.8 |

Worth / Gross sales | 0.4 |

Income Development Fee | 31.3% |

Web Earnings Margin | -0.7% |

GAAP EBITDA % | 1.3% |

Market Capitalization | $54,870,000 |

Enterprise Worth | $69,750,000 |

Working Money Stream | -$1,420,000 |

Earnings Per Share (Totally Diluted) | -$0.50 |

(Supply – In search of Alpha)

Future Prospects For NCS Multistage

In its final earnings name (Supply – In search of Alpha), protecting This fall 2022’s outcomes, administration highlighted the restoration of the {industry} and the corporate throughout 2022 as a result of continued larger demand for vitality merchandise.

Management believes the {industry} is ‘nonetheless within the early levels of this multiyear restoration, with a moderating charge of {industry} exercise development in North America…’

The corporate is within the technique of increasing its operational footprint in Canada and seeks to additional put money into its product growth for a broader array of consumers domestically and internationally.

Wanting forward, administration expects to generate free money stream in 2023, with income at $182.5 million on the midpoint of the vary and adjusted EBITDA at $22.5 million on the midpoint.

Relating to valuation, the market is valuing NCSM at an EV/Income a number of of 0.5x on strong development.

The first danger to the corporate’s outlook is the volatility in hydrocarbon E&P exercise, which can reasonable if macroeconomic situations sluggish within the interval forward.

One other danger is the continued affect of inflation on prices, which have been pressuring gross revenue margins.

If inflationary pressures stay ’embedded’, profitability development will probably be hampered, assuming administration can’t move by value will increase, which can be more and more tough with the bigger E&P corporations within the U.S.

Moreover, a moderating demand development profile in N. America will possible result in elevated competitors for present enterprise alternatives, driving down costs and dampening income development.

This has occurred earlier than in latest cycles within the hydraulic fracturing {industry} within the U.S. and Canada, as service suppliers search to totally make the most of their fleet capability and decrease costs to maintain their crews working.

Additionally, technological advances within the {industry} have been vital in recent times, resulting in ‘haves and have-nots’ as companies have differentiated themselves from their know-how growth.

For fracking service companies to acquire the perfect contracts and finest costs, administration has to put money into R&D efforts to maintain abreast of the most recent improvements in fracking applied sciences; providing clients elevated efficiencies and decrease prices is rising the requirement for getting new enterprise.

Moreover, the hydraulic fracturing {industry} in the USA has modified in composition from quite a few small and midsized companies to plenty of bigger giants and a few midsized companies, with many smaller companies being squeezed out as a result of poor historic efficiency.

So, bigger E&P companies which have come to dominate the most important U.S. shale areas have outsize bargaining energy with smaller service suppliers like NCSM.

These price and utilization pressures can result in worsening money place, elevated debt or fairness issuance and deteriorating inventory efficiency if oilfield service supplier administration groups should not disciplined of their method.

A possible upside catalyst to the inventory might embrace stronger home U.S. development and not using a slowdown as customers proceed to spend their extra financial savings.

Administration expects U.S. and Canada industry-level development to be ‘as much as 10%’ in 2023, whereas it believes worldwide {industry} development to ‘a minimum of 10%’ with the potential for larger development than North America within the close to time period.

Nonetheless, worldwide enlargement could also be extra expensive as a result of being additional afield of the corporate’s core operational footprint in North America.

Whereas I am cautiously optimistic for NCSM, that might change if financial situations deteriorate.

My present outlook on NCSM is a Maintain as we await additional North America demand situation knowledge.

Editor’s Observe: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.

{kind=link}