We Are

Government abstract:

- In personal markets, one of the best funding alternatives can come up in a time of declining fairness markets, rising rates of interest and financial uncertainty

- Evaluation of previous efficiency has proven that one of the best vintages are people who begin throughout recessions or quickly after

- Secondary personal fairness pursuits are buying and selling at steeper reductions to NAV and we imagine yields obtainable in personal credit score current buyers with a compelling entry level

Introduction

A key consideration for buyers when constructing and sustaining their desired strategic asset allocation goal to personal markets is their ongoing dedication technique. Non-public markets methods are sometimes applied through closed-end fund buildings the place capital is named down throughout a fund’s funding interval (sometimes the primary 3-6 years). Portfolio firm investments are made and capital is subsequently distributed again to buyers as firms are offered (sometimes in years 4-10) of the fund’s life. Given this dynamic the place investments are made in a single financial surroundings and offered in one other, a fund’s classic 12 months can have a significant affect on returns.

The present surroundings of financial uncertainty, rising rates of interest and declining fairness markets presents a very enticing surroundings to be committing capital to personal markets. On this article we’ll take into account a few of the key concerns as to why we imagine 2023 is seeking to be a beautiful classic 12 months throughout personal markets together with personal fairness, secondaries and personal credit score.

Key causes personal fairness valuations look promising

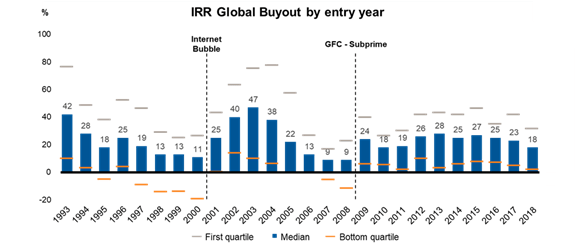

Exhibit 1 under highlights median international buyout inner price of returns (IRRs) for the 26 classic years from 1993 to 2018.1 As seen, historic efficiency has proven that one of the best vintages are these following difficult financial circumstances and unfavourable fairness markets, such because the aftermath of the web bubble within the early 2000s, or the World Monetary Disaster in 2008.

Exhibit 1: World buyout IRR by entry 12 months

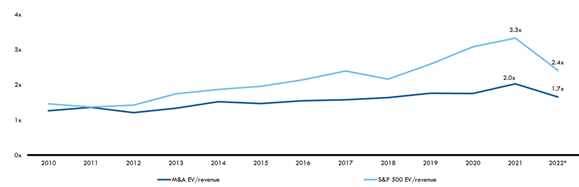

One other key consideration is that entry multiples for personal firms are at present decrease than their public market counterparts. Exhibit 2 highlights public vs. personal valuation multiples since 2010 on an enterprise worth (EV) / income foundation.2 However that since 2010 personal firms have on common traded at a 20% low cost relative to S&P 500 constituents, on the finish of 2022, personal firms traded 40% cheaper than public firms on an EV / income foundation. Given this enticing valuation surroundings, deploying capital with prime quality basic companions ought to drive robust efficiency for the 2023 classic 12 months.

Exhibit 2: Public vs. personal valuation multiples

Secondaries market ripe for alternatives in 2023

Difficult market environments present alternatives for buyers, creating circumstances that enable extra room to make acquisitions at a reduction. This development is in line with earlier recessions or distressed environments which may create nice alternatives for secondary methods.

By specializing in secondary investments and associated methods, we imagine there are quite a few alternatives to supply liquidity to the market and enticing returns for buyers. One component that affects the secondary market is the denominator impact. Fairness and bond valuations have fallen considerably, and this has affected the strategic asset allocation of institutional buyers, forcing them to create liquidity from numerous sections of their portfolios. In these cases, personal markets managers can step in as liquidity options suppliers whereas delivering to their investor’s funding alternatives that may exploit an surroundings characterised by rising rates of interest, fewer exit alternatives and liquidity strains.

alternatives on the secondary aspect, we often see that conventional personal markets funds begin exchanging homeowners three and 5 years after launch, as a result of that is the time when the portfolio has sufficiently developed and there may be sufficient portfolio visibility for sellers and consumers to achieve consolation transacting. So, if we take a look at the latest super international curiosity in personal fairness in the previous few years, we are able to anticipate that an unbelievable quantity of property will attain the secondary market. Along with a few of the restricted companions (LP) pursuits which have began to commerce at deeper reductions to internet asset worth, we’re additionally seeing continued progress typically companions (GPs) continuation options. Basically, managers searching for sources of liquidity for his or her current portfolios could also be enticing to consumers on the secondary market.

Non-public credit score yield continues to develop

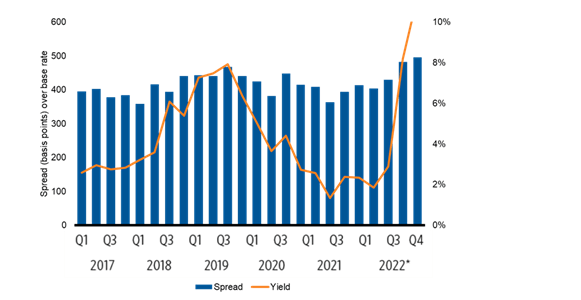

When contemplating credit score, we’d spotlight that spreads and yields have elevated considerably for the reason that starting of 2021. Exhibit 3 exhibits the unfold over base price and yield on new challenge leveraged buy-out (“LBO”) loans.3 Within the case of spreads over the bottom price, these have elevated from 387 foundation factors (bps) in 2021 to 514 bps in 2022. As well as, yields have elevated from 4.7% to 9.86% over the identical interval. On condition that loans in personal credit score are sometimes floating price, buyers are poised to profit from taking part in greater ranges of absolute returns (not like mounted price devices that may lose worth when rates of interest rise) together with safety from inflation.

Exhibit 3: Unfold over base price and yield on new challenge LBO loans

As well as, there may be $554 billion in upcoming maturities from 2024-2026 that can have to be rolled over at considerably greater charges.4 Given these present market dynamics, we imagine personal credit score supplies buyers with extremely enticing entry factors and the potential for draw back administration via the applying of stronger covenants as a part of credit score agreements.

Classic 2023 – A compelling entry level

Finally, in personal markets, one of the best funding alternatives can come up in a time of declining fairness markets, rising rates of interest and financial uncertainty. As such, we imagine 2023 may very well be an opportune time to commit capital to personal markets together with personal fairness, secondaries and personal credit score. Evaluation of previous efficiency has proven that one of the best vintages are people who begin throughout recessions or quickly after. As well as, secondary personal fairness pursuits are buying and selling at steeper reductions to NAV and yields obtainable in personal credit score current buyers with a compelling entry level. It’s exactly throughout these tough market environments that high tier personal markets managers can underwrite investments with the potential to ship enticing returns to buyers.

1 Hamilton Lane, Cobalt, 1993-2018

2 Pitchbook, January 2023

3 Pitchbook, LCD, December 2022

4 Apollo, S&P LCD, Bloomberg as of September 2022.

Disclosures

These views are topic to alter at any time primarily based upon market or different circumstances and are present as of the date on the high of the web page. The knowledge, evaluation, and opinions expressed herein are for basic data solely and aren’t supposed to supply particular recommendation or suggestions for any particular person or entity.

This materials is just not a suggestion, solicitation or advice to buy any safety.

Forecasting represents predictions of market costs and/or quantity patterns using various analytical information. It isn’t consultant of a projection of the inventory market, or of any particular funding.

Nothing contained on this materials is meant to represent authorized, tax, securities or funding recommendation, nor an opinion relating to the appropriateness of any funding. The overall data contained on this publication shouldn’t be acted upon with out acquiring particular authorized, tax and funding recommendation from a licensed skilled.

Please do not forget that all investments carry some stage of danger, together with the potential lack of principal invested. They don’t sometimes develop at a fair price of return and will expertise unfavourable progress. As with all sort of portfolio structuring, making an attempt to cut back danger and improve return might, at sure occasions, unintentionally scale back returns.

The knowledge, evaluation and opinions expressed herein are for basic data solely and aren’t supposed to supply particular recommendation or suggestions for any particular person entity.

Frank Russell Firm is the proprietor of the Russell logos contained on this materials and all trademark rights associated to the Russell logos, which the members of the Russell Investments group of firms are permitted to make use of underneath license from Frank Russell Firm. The members of the Russell Investments group of firms aren’t affiliated in any method with Frank Russell Firm or any entity working underneath the “FTSE RUSSELL” model.

The Russell emblem is a trademark and repair mark of Russell Investments.

This materials is proprietary and will not be reproduced, transferred, or distributed in any kind with out prior written permission from Russell Investments. It’s delivered on an “as is” foundation with out guarantee.

UNI-12211

Editor’s Observe: The abstract bullets for this text have been chosen by Searching for Alpha editors.

{kind=link}