Medical insurance corporations have been witnessing a decline in claims currently as non-urgent medical procedures are being deferred because of excessive inflation and stress on private funds. UnitedHealth Group (NYSE: UNH), a market chief in medical insurance, is on a mission to supply complete healthcare companies via continued diversification. Authorities-supported medical insurance plans have been a key development driver for the corporate.

UnitedHealth’s monetary efficiency within the early months of 2023 was robust, marked by optimistic information throughout the broad. However the outcomes did not impress the market, and the inventory skilled weak spot following the announcement final week. It seems to be just like the market was anticipating an even bigger increase in full-year earnings steering.

Investing in UNH

Whereas the inventory is comparatively costly, the current dip has made it extra inexpensive. It may be seen as a very good entry level, contemplating the healthcare behemoth’s regular development and specialists’ bullish outlook on its future prospects. At present buying and selling barely under its long-term common, the inventory is more likely to cross the $600 mark within the coming months. It’s a comparatively secure funding that might discover many takers if the recessionary fears persist, prompting traders to search for much less dangerous choices.

Going ahead, there will probably be a continued enhance within the adoption of Medicare Benefit plans as extra folks retire. It’s price noting that medical insurance plans like Medicare account for greater than one-third of the corporate’s insurance coverage enterprise. On the similar time, the Optum affected person care division is predicted to serve greater than 4 million sufferers in absolutely accountable value-based care preparations, which is almost double that of the 2021 quantity.

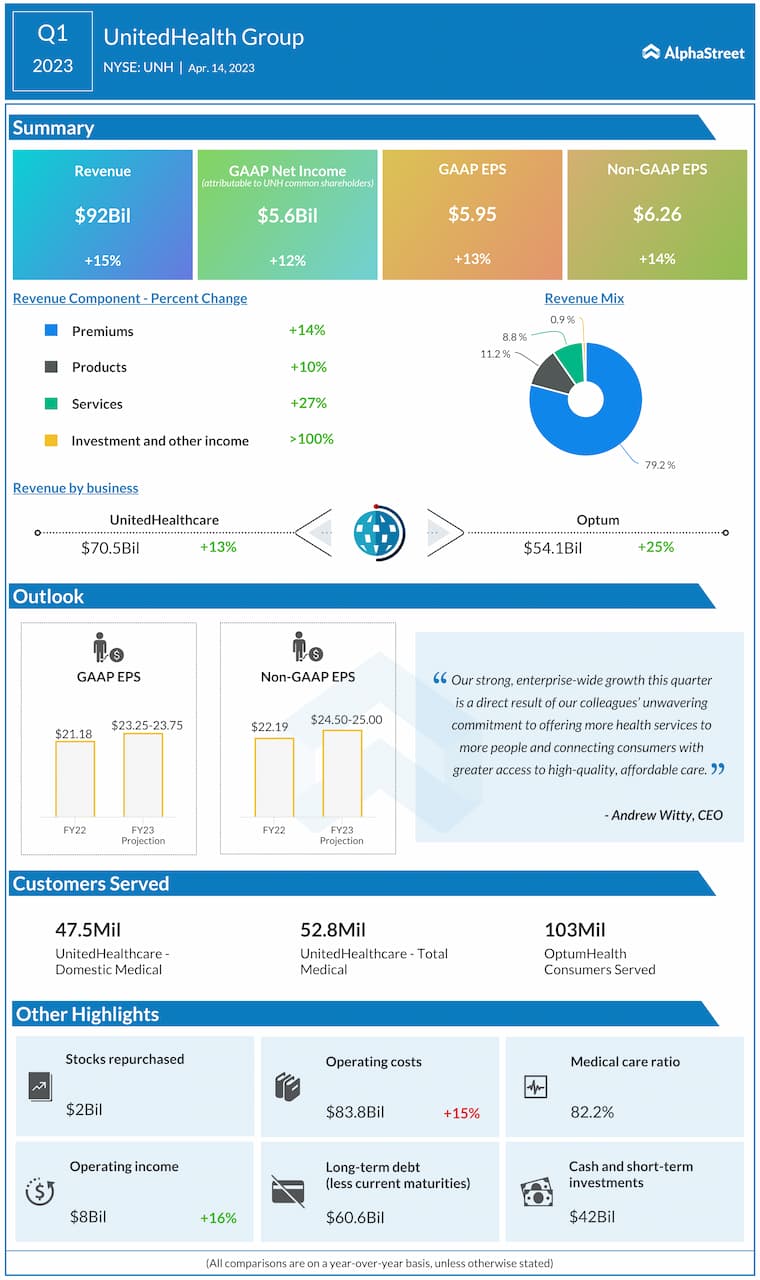

Sturdy Numbers

Within the first quarter of 2023, each the UnitedHealth division and the Optum enterprise expanded in double digits. That, mixed with continued robust development within the core Premiums phase, led to a 15% development in whole revenues to $92 billion, which additionally topped expectations. Internet revenue, adjusted for particular objects, superior 14% yearly to a document excessive of $6.26 per share. Through the years, the corporate has always impressed its stakeholders by delivering stronger-than-expected quarterly revenue, and the development continued within the first quarter.

From UnitedHealth’s Q1 2023 earnings name:

“Over the previous yr, we centered on enhancing the patron expertise throughout our firm. This shopper orientation is foundational in help of every of our development priorities, together with our strategy to value-based care. For instance, this yr we count on to serve greater than 4 million sufferers in absolutely accountable, value-based care preparations via Optum, about double the place we had been on the finish of 2021. These sufferers will probably be members of UnitedHealthcare profit plans or one of many many different plans served by Optum.”

Outlook

The corporate ended the quarter with a formidable money stream of $16.3 billion and expects to keep up a powerful money place. Taking a cue from the encouraging enterprise backdrop, the administration raised its full-year outlook for adjusted web earnings to $24.50–$25.00 per share, with an estimated development in Medicare memberships boosting the underside line. Shares of UnitedHealth largely traded sideways this yr, earlier than gaining power forward of final week’s earnings. However it modified course after the announcement and traded decrease on Monday afternoon.

{kind=link}