Galeanu Mihai

Funding Thesis

Progress and tech shares, particularly SaaS (software program) shares, have fallen out of favor for about two years now. Mixed with a slowdown in development in some notable shares within the portfolio, the portfolio has continued its mediocre efficiency, and stays having a detrimental return.

General, portfolio exercise has been muted as I’ve taken a principally wait-and-see angle.

Background

The portfolio was created in late 2019. The earlier replace might be discovered right here: Portfolio Collapse: Wealth Destruction Because the portfolio has not meaningfully modified since then, I’ll seek advice from that replace for an in depth overview of the portfolio.

This autumn/Q1 replace and ideas

Maybe for sure, however my sentiment in the direction of investing has remained fairly subpar given the evolution of the portfolio efficiency, which because the begin of inflation and so forth. has taken a deep nosedive.

Personal work

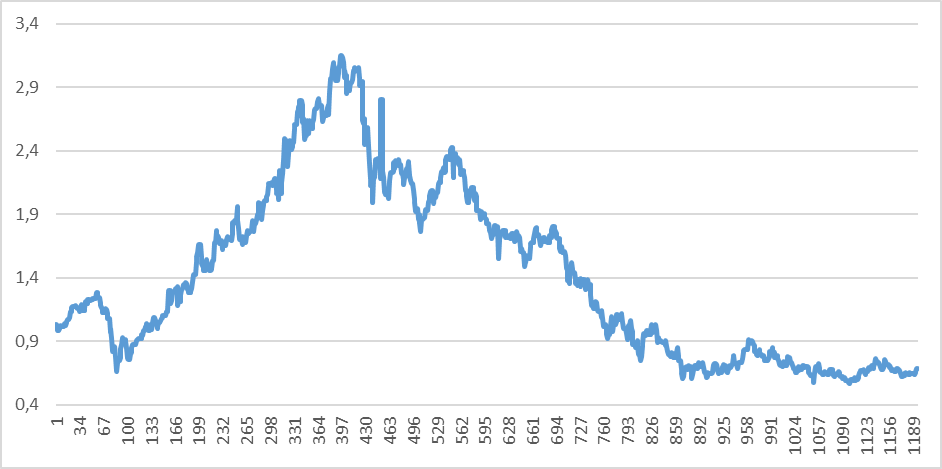

The return of the portfolio (as measured by the ratio of present worth and nest egg) is at the moment a bit over -30% (0.7x), a far cry from the 3x it as soon as was. The result’s that the portfolio worth has been flat (at finest) for the previous few years, regardless of the nest egg greater than tripling in measurement.

The portfolio reached its lowest alpha in late December with an over 40% decline in worth vs. nest egg. Be aware: since I’ve primarily offered worthwhile shares, the return as measured by its present worth in comparison with the quantity invested is even worse. In late December, this return was -50%.

Clearly, in hindsight there are various potentialities that would have delivered far better returns. For instance, my high choose for 2021 was Asana (ASAN). If I had offered the entire portfolio on the peak in early 2021 and put it in ASAN, which went on to change into a few 4-bagger by the top of the yr, a bit much like Upstart (UPST), a inventory I used to be not but conscious of on the time, if I had then offered this hypothetical single inventory portfolio once more after its rally, then I’d have made a >10x return in (my first) two years of investing. Not too dangerous. Oh effectively.

When it comes to portfolio exercise, the principle exercise has been as a result of Unity (U) acquisition of ironSource, which led my dealer to promote all ironSource shares. With this capital, I primarily purchased Unity and SentinelOne (S), in addition to Intel (INTC), Asana, SmartSheet (SMAR), monday.com (MNDY), Alteryx (AYX), Affirm (AFRM) and Upstart (UPST). Within the final half a yr, I additionally purchased a bit extra Modern Industrial Properties (IIPR) and Marqeta (MQ).

In February, I offered a significant portion of my unique Pinterest (PINS) funding for a 40% return, which was used primarily to purchase extra S. Nonetheless, since I additionally purchased some PINS on the best way down from its peak, general PINS has been a roughly flat funding.

Investor Takeaway

With the speed of inflation beginning to drop and the highest of rates of interest seen, one may argue that it’s at the moment an opportune time to put money into the form of SaaS shares as in my portfolio. After all, such calls have been made earlier than, and have turned out fallacious.

Nonetheless, within the second half of 2022 (maybe a bit coincidental with the preliminary slowdown in M/M inflation), the portfolio decline lastly began to decelerate. (The December correction was greater than made up for with the rally in January.) General, SaaS shares have now change into traditionally low-cost, inside nearly two years after that they had change into traditionally costly, which explains why it could possibly be worthwhile to take a look at this asset class once more.

Whereas some corporations have seen maybe a slowdown given the macro atmosphere, the overall thesis for development investing stays that corporations with sturdy development ought to over time have the ability to outgrow their valuation, resulting in outsized returns. For bullish development traders, an improved macro atmosphere (decrease rates of interest and inflation) may result in a re-acceleration in development and valuation a number of enlargement.

Concerning my very own portfolio, since I didn’t anticipate the extent of the decline over the past two years, for probably the most half I didn’t actively handle the portfolio. Any shares that I did promote (equivalent to IIPR), I changed these different SaaS shares anyway.

In a number of earlier updates, readers have really helpful better diversification. Whereas that is certainly a legitimate remark, on condition that my portfolio includes tech shares (admittedly of various diploma of high quality, although), which as argued are at the moment traditionally low-cost, it appears cheap to simply proceed with the portfolio in the identical spirit as the unique technique, which was the purchase and maintain for a few years. My high choose stays SentinelOne, primarily based on the instance of CrowdStrike (CRWD).

{kind=link}